Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

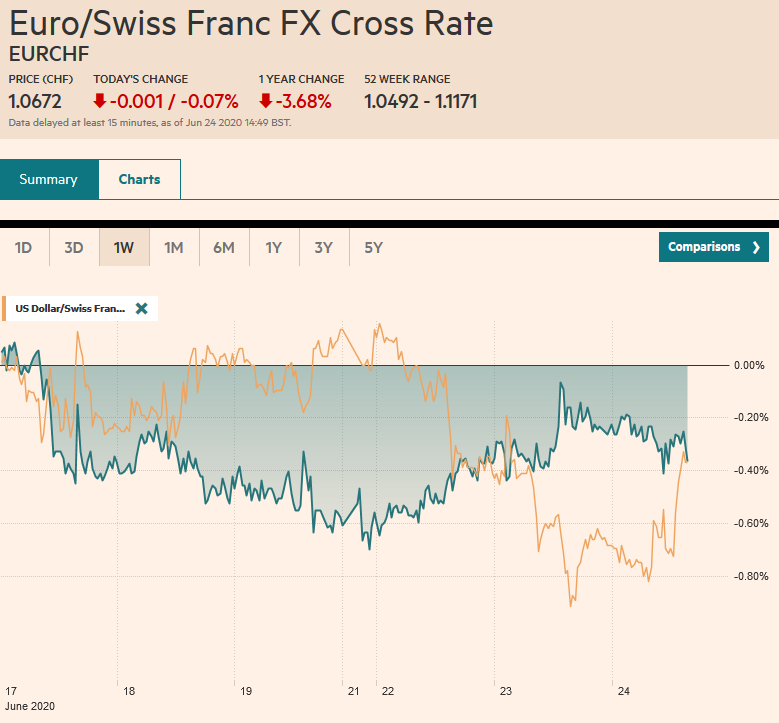

Swiss FrancThe Euro has fallen by 0.07% to 1.0672 |

EUR/CHF and USD/CHF, June 24(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The rally in risk assets in North America yesterday is failing to carry over into today’s activity. Asia Pacific equities were mixed. Korea and Indonesia led the advances with more than 1% gain. China and Taiwan also gained. Japan and Hong Kong. Europe’s Dow Jone’s Stoxx 600 is giving back yesterday’s gains (~1.3%) plus some and US stocks are heavy. The early call is for the S&P 500 to open around 1% lower, which would unwind most of the gains seen in the past two sessions. The NASDAQ rallied to new record highs yesterday and has only fallen in three sessions since May 21, including an eight-day streak that may be challenged today. Bond markets are quiet, and yields mostly lower, though Italy’s small increase is consistent with the risk-off mood. The US 10-year yield is soft around 70 bp. The dollar, which appeared to be breaking lower yesterday, is coming back firmer today against nearly all the major currencies. The Antipodeans and Scandis are bearing the brunt, while the Swiss franc and yen are faring best with small gains. Outside of a handful of emerging market currencies from Asia, emerging market currencies are trading lower. Gold is extending its recent gains and is at new multiyear highs and drawing closer to the $1800 target. August light sweet crude oil is being pushed back below the $40-a-barrel mark and may find support in the $38.50-$39.00 area. |

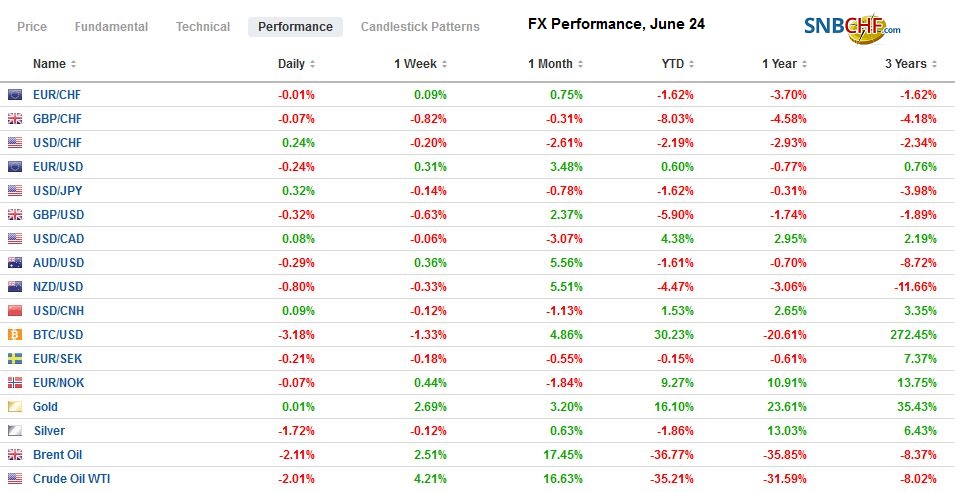

FX Performance, June 24 - Click to enlarge |

Asia Pacific

The Reserve Bank of New Zealand left rates and asset purchases steady at the conclusion of its policy meeting. It did keep open the possibility of both lower rates (25 bp cash rate target) and more purchases, if necessary.

China is requiring international shippers of meat and soy sign documents attesting to the safety of its cargo. There has been an effort to link the recent virus outbreak to imported food. Although Tyson, which has seen some of its poultry banned, after containment in a processing plant, signed-off, many US firms are reportedly reluctant, several Brazilian companies have agreed.

India has slapped anti-dumping duties on flat-rolled steel from China, South Korea, and Vietnam. The duties could remain for five years. Separately, India is poised to levy new tariffs on solar energy equipment. It appears, according to reports, to be focused on solar cells, modules, and inverters. This seems to impact China the most, which provides an estimated 80% of the modules, for example. Although there is no official confirmation of the size of the duty, some suggest it could be around 20%.

Japan, like many other countries, including the US, are struggling with the logistics of distributing funds to millions of households. A report out estimates that some 40% of the cash payments to households have yet to be distributed. Separately, some reports are linking the yen’s surge yesterday to more flows related to the Softbank-T-Mobile unwind. This was cited as a factor last week as well. Volume in the euro-yen options spiked to roughly twice the five-day average.

The dollar fell to almost JPY106 yesterday, its lowest level since May 7. The big outside down day is seen as bearish price action. Although there has been no follow-through selling today, the greenback has been unable to surface above JPY106.65. It is trading in about a quarter of a yen range above JPY106.40. The JPY106.80-JPY107.00 may offer nearby resistance. There is a $655 mln option at JPY107.00 that expires today. The Australian dollar looked like it was breaking higher yesterday, reaching $0.6975, a five-day high. However, it is pulling back today and is below $0.6900 in the European morning. A close today below $0.6880 would seem to negate yesterday’s favorable price action and setting up another test on $0.6800. The dollar is snapping a three-day drop against the Chinese yuan. For the better part of three weeks, the greenback has been largely confined to a CNY7.05-CNY7.10 range. The PBOC set the dollar’s reference rate a little weaker than the bank models suggest. The Hong Kong Monetary Authority continues to be active defending the HKD7.75 level.

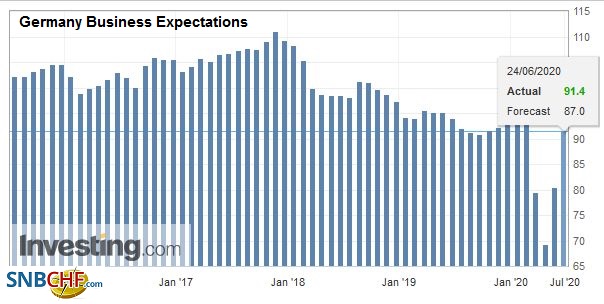

EuropeGermany’s IFO survey confirms what recent surveys have shown, and that is Europe’s largest economy is on the mend. The current assessment in June edged higher to 81.3 from 78.9. Recall that it May it had fallen for the fourth month. The forward-looking expectations component rose to 91.4 from 80.5 in May. |

Germany Business Expectations, June 2020(see more posts on Germany Business Expectations, ) Source: investing.com - Click to enlarge |

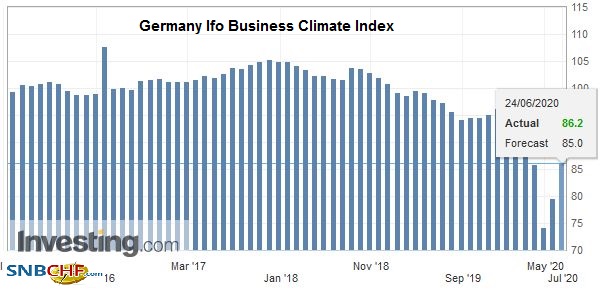

| It bottomed in April at 69.5. It averaged 93.4 last year. The overall assessment of the business climate rose to 86.2 from 79.7, which is the highest since February. |

Germany Ifo Business Climate Index, June 2020(see more posts on Germany IFO Business Climate Index, ) Source: investing.com - Click to enlarge |

The EU is planning on re-opening its borders on July 1 but is considering barring American travelers because the virus is not under control. Travelers from Brazil and Russia would also be blocked, according to press accounts. Note that the US still has not opened up travel for Europeans, though they appear to be doing a better job of containment. The German state of North Rhine-Westphalia has imposed a new lockdown on the city of Gutersloh to contain the flare-up. Meanwhile, California has reported its biggest jump in cases, and Florida’s infection rate exceeded 10% (as are another seven states). Some estimates put the Ro for 60% of US states above 1.0 (meaning each person with the virus is infecting one other person). The seven-day average number of new cases has been rising in the US since June 9. According to data from Johns Hopkins, on June 21, the US seven-day moving average was 28.3k, while Europe, with more testing, had a seven-day average 88% lower (3.4k). Dr. Fauci admitted to being troubled by the spike in cases in some areas, which he attributed to more infections, not more tests.

The US is going forward with plans to impose tariffs on a range of imports from Europe as part of its response to the WTO ruling about unfair subsidies to Airbus. Imports from Germany, France, Spain, and the UK are targeted. Consumer goods, like olives, beer, and gin, along with trucks, could face new tariffs, while current tariffs on cheese, yogurt, and aircraft may be increased. The public comment period is for a month. Meanwhile, the case against Boeing is also making its way through the WTO process, and a decision could be delivered in Q3.

The euro rose to almost $1.1350 yesterday, but the upside momentum has faltered, and the euro fell to about $1.1270 in the European morning. There is an option for 665 bln euros at $1.13 that expires today. Stronger support is seen closer to $1.1250. A close above $1.1325 would signal a move back to the high set earlier this month near $1.1425. Sterling marginally extended yesterday’s rise and reached almost $1.2545 before profit-taking set in. The trendline drawn from the June 10 high (~$1.2815) and last week’s high (~$1.2690) caught yesterday’s high (~$1.2530). It was violated intraday today, but the close is important. Support is cited in the $1.2430-$1.2450 band.

America

For the first time since February, the US composite PMI slipped below the eurozone’s (46.8 vs. 47.5). The preliminary estimate for the US missed forecasts, but the groundwork for the recovery is being laid, and expectations for a better Q3 have not been dented by the data. The June Richmond Fed manufacturing survey, like the others, was better than expected, and new sales in May exceeded not only economists forecast but the level from last May and the 2019 average.

The North American economic calendar is light today. No major reports are due. The Fed’s Bullard and Evans speak after the European markets close. Mexico reports its bi-weekly CPI. Tomorrow it reports April retail sales (a month-over-month decline of 18% is the median forecast in the Bloomberg survey) ahead of Banxico’s decision on rates. Mexico was hit by a 7.4-magnitude earthquake yesterday, while the Covid virus infections continue to rise. A 50 bp rate cut is widely expected. The IMF updates its economic forecasts today. World growth is expected to be revised lower from its April estimates.

Over the past week or so, the US dollar has been confined to a CAD1.3500-CAD1.3630 range. Yesterday, it broke down to about CAD1.3485, an eight-day low. However, the intraday breakout was not confirmed by the close, where the greenback settled near CAD1.3550, near session highs. The risk-off mood and softer commodity prices could help lift the dollar toward CAD1.3600, where a $640 mln expiring option has been struck. Above there is the June 15 high around CAD1.3685. The dollar has been making lower highs against the Mexican peso for the past three sessions, and yesterday’s high a little below MXN22.68 may be challenged today. Support this week has been seen near MXN22.30. Note that the dollar has not traded above MXN23.00 since May 22.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,China,Currency Movement,EUR/CHF,FX Daily,Germany Business Expectations,Germany IFO Business Climate Index,India,Mexico,newsletter,USD/CHF