Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

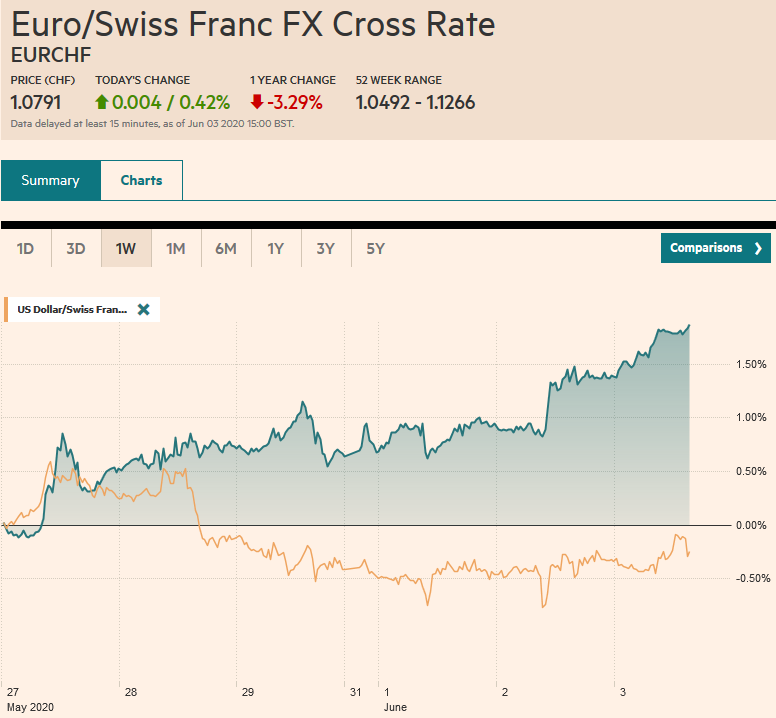

Swiss FrancThe Euro has risen by 0.42% to 1.0791 |

EUR/CHF and USD/CHF, June 3(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: Two recent trends continue. Equities are moving higher, and the dollar remains heavy. Equity markets in the Asia Pacific region rose at least one percent, and South Korea, Singapore, and Malaysia rallied 2-3%. Europe’s Dow Jones Stoxx 600 is up more than 1% for the third consecutive session. US shares are trading higher and are poised to extend their recent run. Bond yields are backing up. Australia, New Zealand, and South Korea saw 5-6 bp increases, while European bonds are 2-3 bp higher. The US 10-year benchmark is straddling the 70 bp area. The dollar is soft against most European currencies, led by the Scandi bloc, and the euro is trying to establish a foothold above $1.12. The greenback is consolidating its recent gains against the dollar-bloc currencies. The Swiss franc and yen remain on the defensive. Outside of China, Turkey, India, and most emerging market currencies also are firmer against the dollar. Gold was turned back after approaching $1750 yesterday, and July WTI is above $38, while August Brent poked above $40. |

. |

Asia PacificChina’s Caixin PMI surprised to the upside. The non-manufacturing component rose to 55. from 44.4 in April. The composite rose to 54.5 from 47.6. Nevertheless, China is expected to provide more monetary and fiscal stimulus. Meanwhile, Hong Kong forward points eased with the 3-month nearly back at pre-crisis levels, thought the 12-month points remain elevated. |

China Caixin Services Purchasing Managers Index (PMI), May 2020(see more posts on China Caixin Services PMI, ) Source: investing.com - Click to enlarge |

A pattern that is emerging with the service sector PMI reports is that the final reading is mostly above the preliminary or flash reports. This began in Japan and Australia. Japan’s service PMI rose to 26.5 from 25.3, and 21.5 in April. The composite rose to 27.8 from 27.4, and 25.8 in April. Australia’s service PMI rose to 26.9 from 25.5. It was below 20 in April. The composite PMI rose to 28.1 form 21.7 in April. The preliminary estimate was 26.4. Separately, Australia reported that Q1 GDP contracted by 0.3%, a little less than anticipated. The BOJ is considering doubling its assistance to small businesses as early as the policy meeting later this month.

The yen was sold off hard yesterday, finally capitulating to the unwind of “safe haven” strategies that had already pressured the US dollar, and was also becoming evident in the Swiss franc. The US dollar broke out of its narrow range yesterday, surging above the 200-day moving average (~JPY108.35), for the first time since mid-April to nearly JPY108.80. Follow-through buying today in Tokyo saw only a marginal new high before consolidating. As long as the JPY108.00-JPY108.20 area holds, the breakout will be confirmed. The Australian dollar’s gains accelerated to almost $0.7000 (~$0.6985) before profit-taking kicked in and sent the Aussie to about $0.6880 before buying returned. Still, a stronger recovery in North America is needed to avoid leaving a bearish shoot star candlestick in its wake. The PBOC set the dollar’s reference rate a bit stronger than the bank models suggested (CNY7.1074 vs. CNY7.1053). The dollar is ending its four-day downtrend against the yuan, and the CNY7.10, which was the upper end of the previous range, now could be the lower end of the new range. The dollar has sold off hard against the Indonesian rupiah (-2.2%) after a 1.3% slide on Monday. Strong portfolio flows into its bond market, where the 10-year local currency bond yield has fallen near 35 bp over the past week.

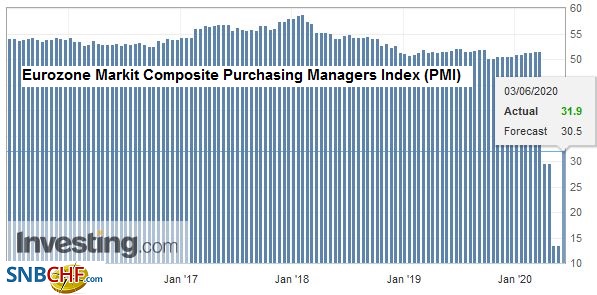

EuropeThe main macro development today is the final service and composite PMI readings. |

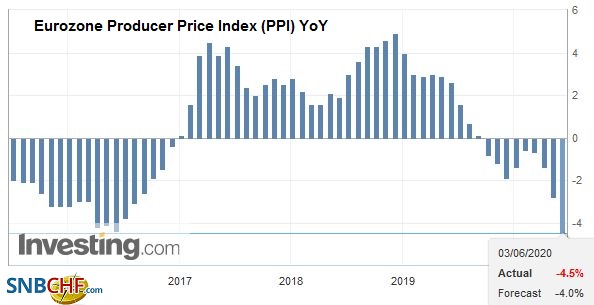

Eurozone Producer Price Index (PPI) YoY, April 2020(see more posts on Eurozone Producer Price Index, ) Source: investing.com - Click to enlarge |

| They were better than expected. Germany’s May service PMI was twice April at 32.6 (vs. 16.2) and a little higher than the preliminary reading. The composite, held back by the manufacturing PMI, rose to 32.3 form 31.4 (flash) and 17.4 in April. France’s story was the same but more. The service PMI rose to 31.1 from the initial estimate of 29.4 and 10.2 in April. |

Eurozone Markit Composite Purchasing Managers Index (PMI), May 2020(see more posts on Eurozone Markit Composite PMI, ) Source: investing.com - Click to enlarge |

| The composite stands at 32.1 after 11.1 in April. Spain and Italy, which do not see preliminary estimates, rose more than expected. In Spain, the service PMI rose to 27.9 from 7.1, and the composite is at 29.2 after 9.2 reading in April. Italy service PMI jumped to 28.9 from 10.8, and the composite surged to 33.9 from 10.9. |

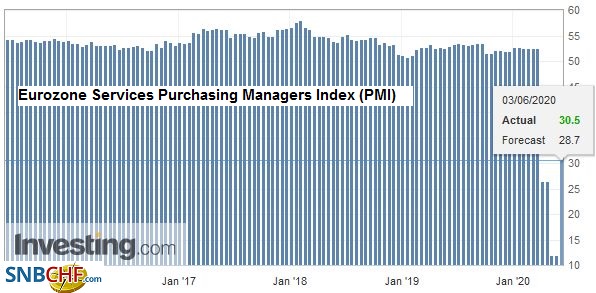

Eurozone Services Purchasing Managers Index (PMI), May 2020(see more posts on Eurozone Services PMI, ) Source: investing.com - Click to enlarge |

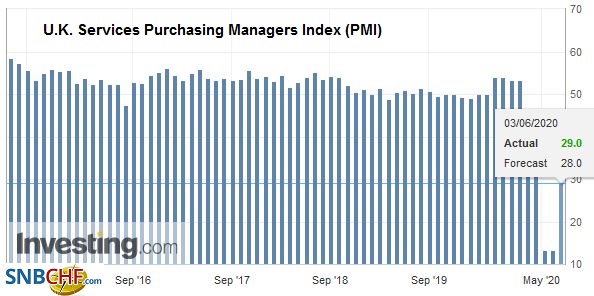

| The same general pattern was evident in the UK. Between the time of the preliminary estimate and the final reading, the situation, while remaining dire, improved. The service PMI rose to 29.0 from the 27.8 flash report and 13.4 in April. The composite rose to 30.0 from 28.9 initially and 13.8 in April. Separately, we note that Bank of England Governor Bailey encouraged banks to prepare for the UK and EU to fail to secure a trade agreement by the end of the year. |

U.K. Services Purchasing Managers Index (PMI), May 2020(see more posts on U.K. Services PMI, ) Source: investing.com - Click to enlarge |

The euro is trading higher for the seventh consecutive session and pushed above $1.12 for the first time since mid-March. There are 1.4 bln euros in options struck between $1.1210 and $1.1220 that will expire today. The high in late Asia was just shy of $1.1230. Sterling’s advancing streak has extended into the fifth consecutive session today, and it traded above $1.26 for the first time since May 1. The 200-day moving average is near $1.2675, and it has not traded above it since March 12, and the April highs were set a little lower (~$1.2640-$1.2650). Turkey’s CPI was stronger than expected (almost 11.4% in May from just below 11% in April) and mostly reflected an increase in the core rate. This takes real rates in Turkey deeper into negative territory and weakened the lira after it rose to near two-month highs.

AmericaThe Bank of Canada meets today amid little fanfare. The Bank of Canada has responded aggressively to the crisis. It slashed the overnight target rate to 25 bp from 150 bp, a record low. It launched its first quantitative easing (large-scale asset purchases) by buying federal, provincial, and corporate debt. The balance sheet has quadrupled to around C$465 bln or about 20% of GDP. Poloz was not an advocate of negative rates, and we suspect Macklem concurs. Current policies can be scaled if needed. Thursday’s economic update (to be delivered by a deputy governor) and Friday’s jobs report lay ahead. The Canadian dollar often moves alongside the other Australian and New Zealand dollar, and it has been the laggard in the advance that has accelerated since mid-May. The Canadian dollar has risen about 4.3% compared with around 7.8% for the Antipodeans. Lastly, while the Reserve Bank of Australia has targeted the 3-year yield at 25 bp, the same as its cash rate target, the Bank of Canada has not introduced yield curve control. However, its two-year yield has been stable, hovering around 30 bp since the end of April. |

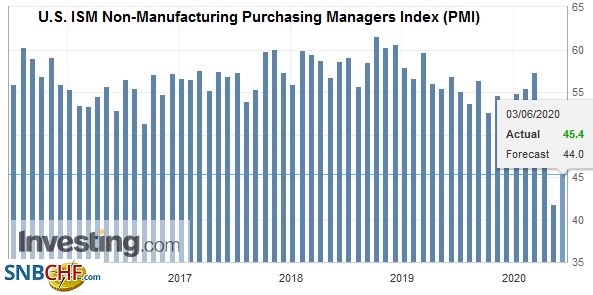

U.S. ISM Non-Manufacturing Purchasing Managers Index (PMI), May 2020(see more posts on U.S. ISM Non-Manufacturing PMI, ) Source: investing.com - Click to enlarge |

| The ADP releases its estimate of the change in last month’s private sector employment. A loss of 9 mln jobs is expected after a 20.2 mln loss in April. The median forecast in the Bloomberg survey for Friday’s non-farm payroll is for a decline of 8 mln. Markit reports its final service and composite PMI and the ISM issues its non-manufacturing index. The takeaway is that construction continues but at a slower rate, which is still seen setting the stage for a recovery beginning in Q3. The labor market, and the current end of the extended benefits next month, could set the stage for the second wave of layoffs, and this risk is beginning to be discussed. April factory and durable goods orders are too dated to have much impact. Separately, the US has begun reviewing the digital tax that several countries in Europe and India are threatening, and this could be a source of friction (tariffs?) in the coming months. |

U.S. ADP Nonfarm Employment Change, May 2020(see more posts on U.S. ADP Nonfarm Employment Change, ) Source: investing.com - Click to enlarge |

The US dollar had fallen from CAD1.40 on May 25 to about CAD1.3480 yesterday. It is holding near the today, which is a little above the 200-day moving average (~CAD1.3460). There is also an old gap from March (~CAD1.3440-CAD1.3460) that may have some technical significance. Resistance is seen in the CAD1.3585-CAD1.3615 area. The impressive recovery of the peso continues. The dollar traded toward MXN21.50, and the next technical target is near MXN21.30. Its recovery despite weak fundamentals can be attributed to its high real and nominal interest rates. We are concerned that the level of the peso needed to clear the capital markets is much stronger than the level of the peso needed to clear the market for goods and services.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,$CNY,Bank of Canada,China Caixin Services PMI,Currency Movement,EUR/CHF,Eurozone Markit Composite PMI,Eurozone Producer Price Index,Eurozone Services PMI,FX Daily,hkd,newsletter,U.K. Services PMI,U.S. ADP Nonfarm Employment Change,U.S. ISM Manufacturing PMI,U.S. ISM Non-Manufacturing PMI,USD/CHF