Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

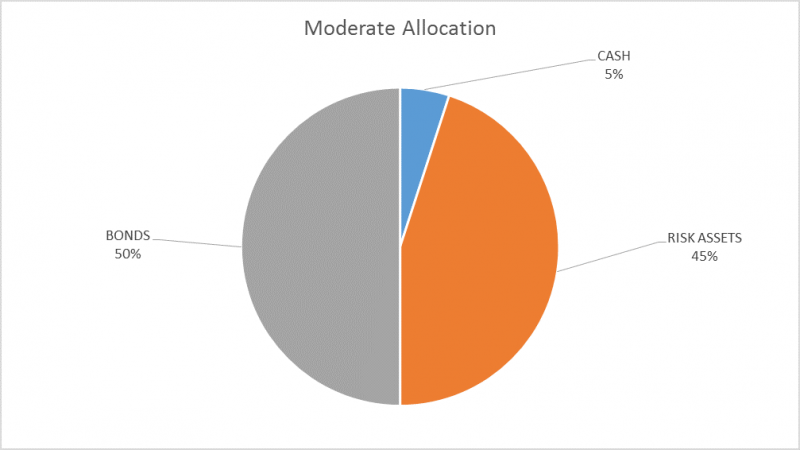

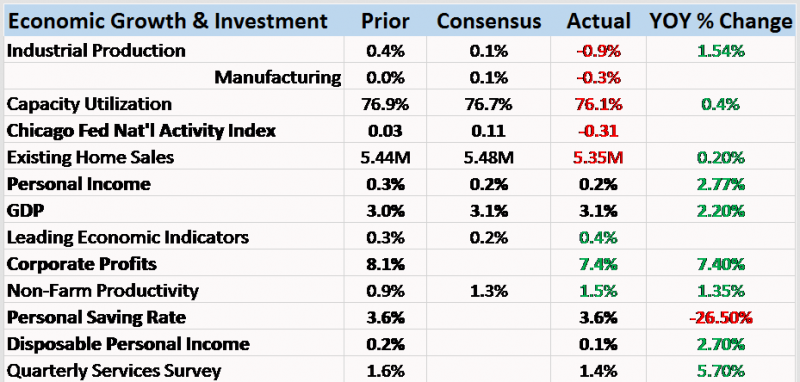

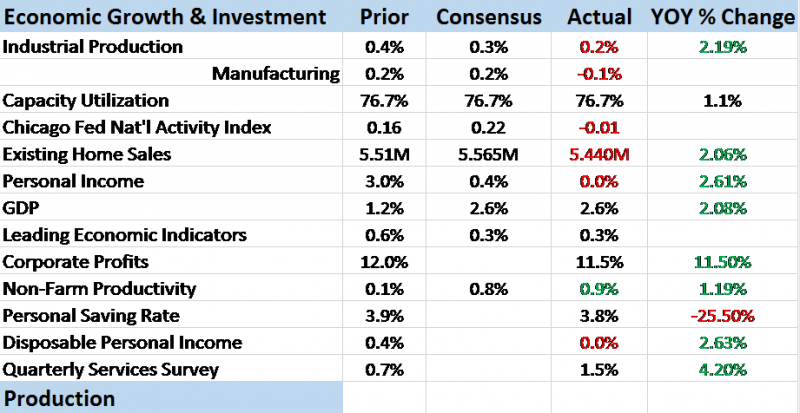

Weekly Market Pulse: The Turkey Leg

Weekly Market Pulse: The Turkey Leg23 Jun 2025

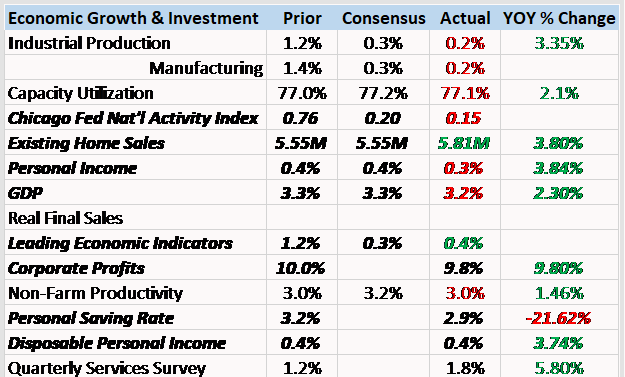

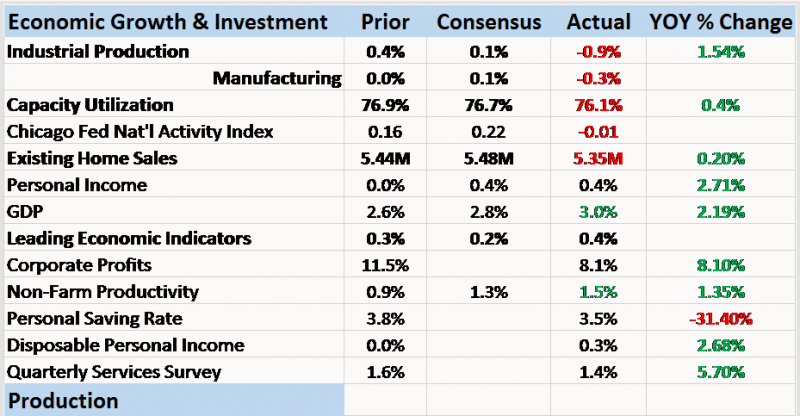

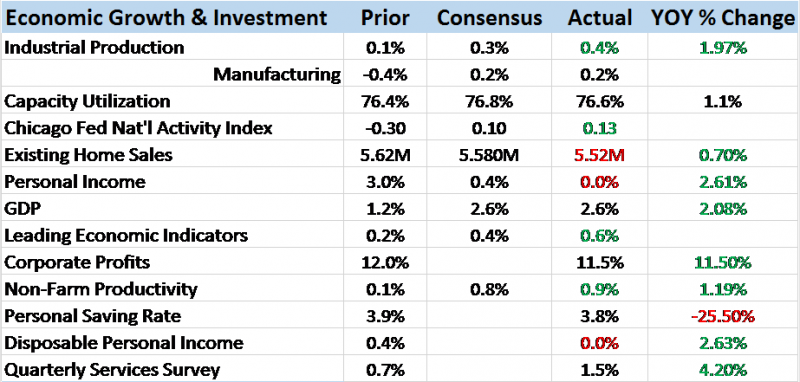

Weekly Market Pulse: No Free Lunches

Weekly Market Pulse: No Free Lunches19 May 2025

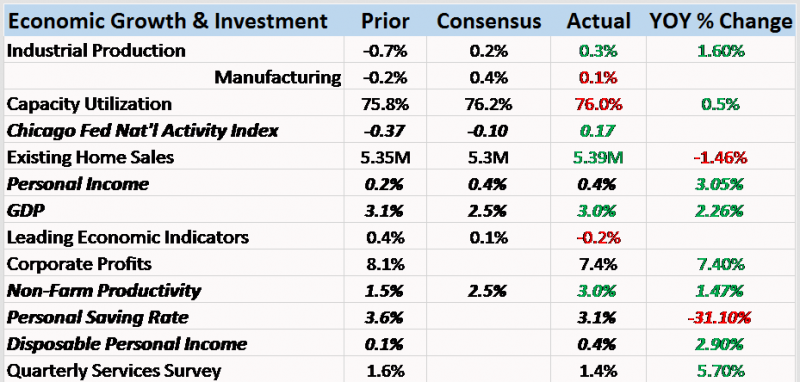

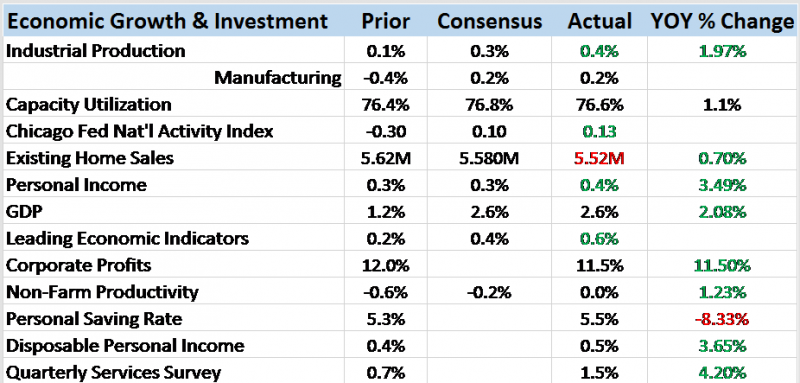

Weekly Market Pulse: Just A Little Volatility

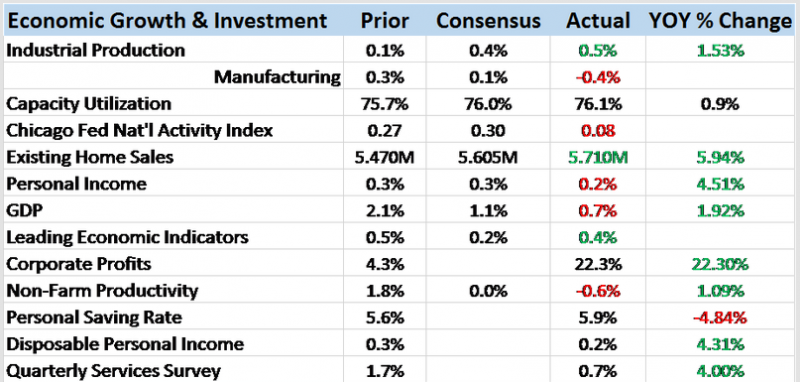

Weekly Market Pulse: Just A Little Volatility17 Oct 2022

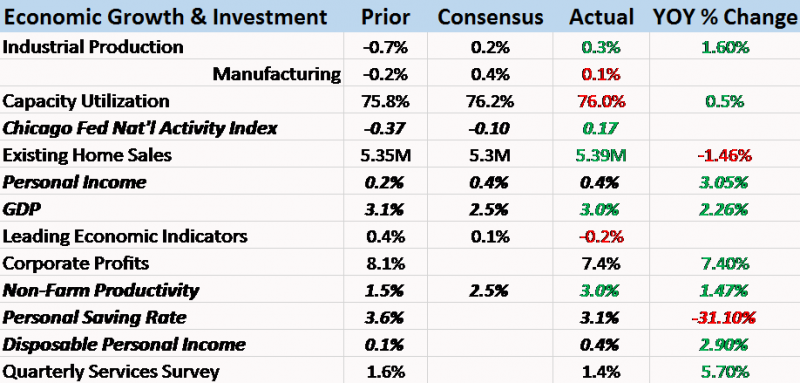

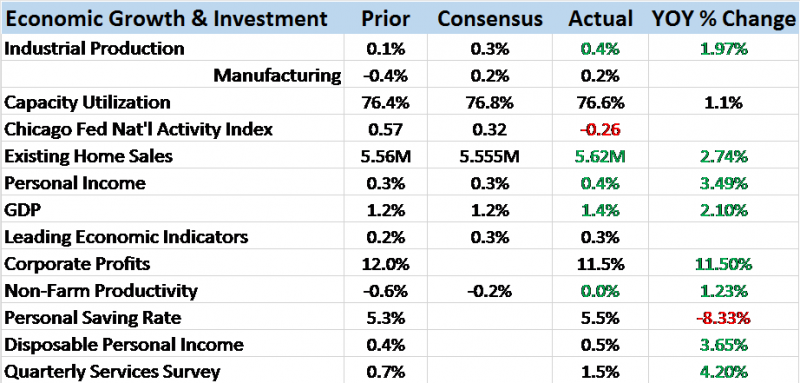

Weekly Market Pulse: Peak Pessimism?

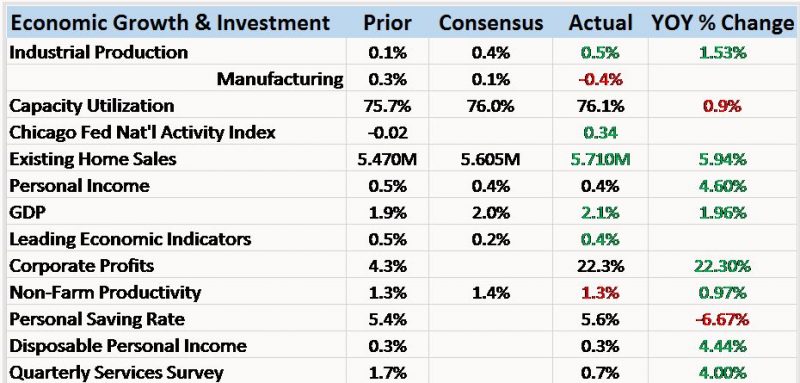

Weekly Market Pulse: Peak Pessimism?3 Oct 2022

Weekly Market Pulse: No News Is…

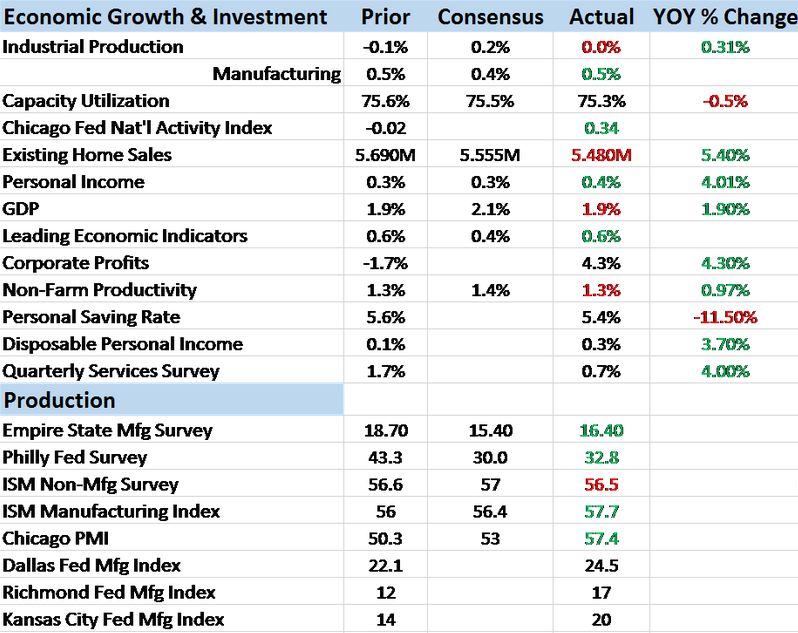

Weekly Market Pulse: No News Is…12 Sep 2022

Weekly Market Pulse: Opposite George

Weekly Market Pulse: Opposite George1 Aug 2022

Weekly Market Pulse: Expand Your Horizons

Weekly Market Pulse: Expand Your Horizons29 Jun 2022

Market Pulse: Mid-Year Update

Market Pulse: Mid-Year Update24 Jun 2022

One Shock Case For ‘Irrational Exuberance’ Reaching A Quarter-Century

One Shock Case For ‘Irrational Exuberance’ Reaching A Quarter-Century22 Dec 2021

Weekly Market Pulse: Has Inflation Peaked?

Weekly Market Pulse: Has Inflation Peaked?13 Dec 2021

Weekly Market Pulse: Discounting The Future

Weekly Market Pulse: Discounting The Future7 Dec 2021

Weekly Market Pulse: Growth Scare?

Weekly Market Pulse: Growth Scare?1 Nov 2021

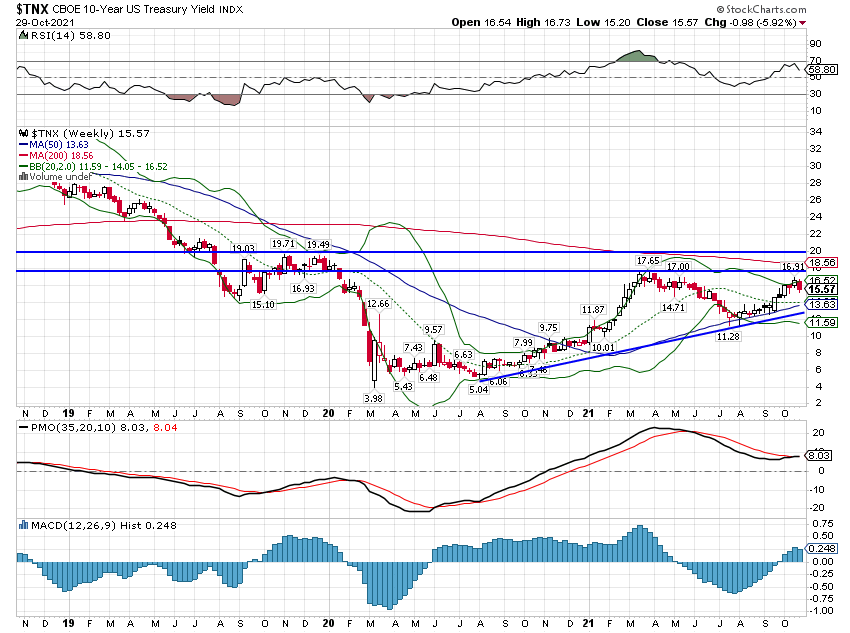

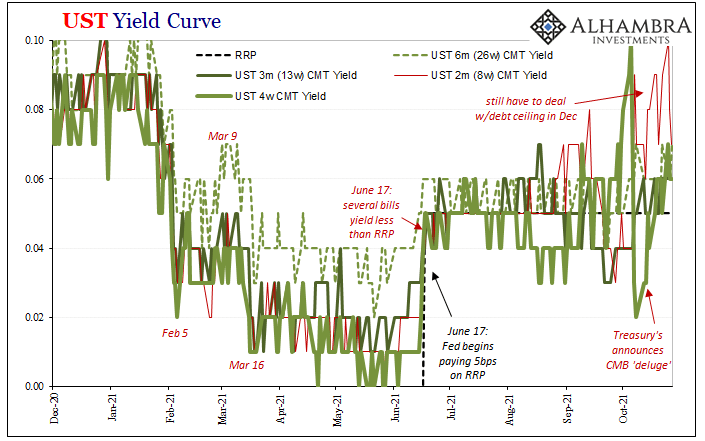

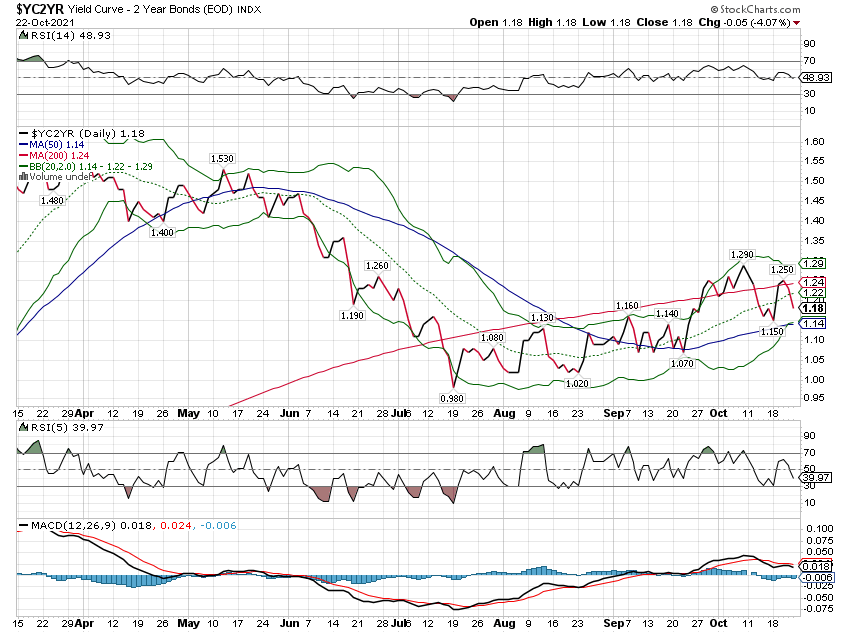

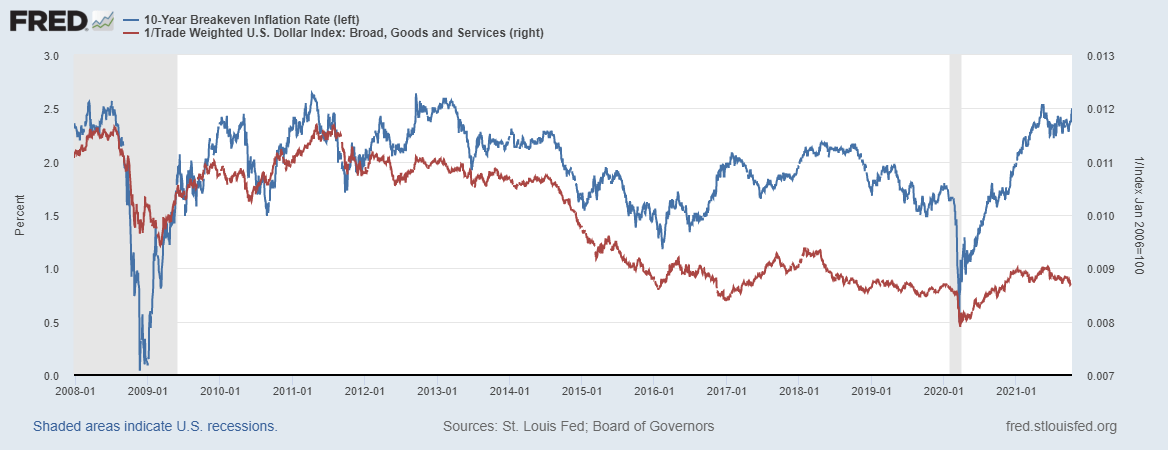

Short Run TIPS, LT Flat, Basically Awful Real(ity)

Short Run TIPS, LT Flat, Basically Awful Real(ity)28 Oct 2021

Weekly Market Pulse: Inflation Scare!

Weekly Market Pulse: Inflation Scare!25 Oct 2021

Weekly Market Pulse: Inflation Scare?

Weekly Market Pulse: Inflation Scare?11 Oct 2021

Weekly Market Pulse: Zooming Out

Weekly Market Pulse: Zooming Out3 Oct 2021

Weekly Market Pulse: What Is Today’s New Normal?

Weekly Market Pulse: What Is Today’s New Normal?9 Aug 2021

Golden Collateral Checking

Golden Collateral Checking27 Jul 2021

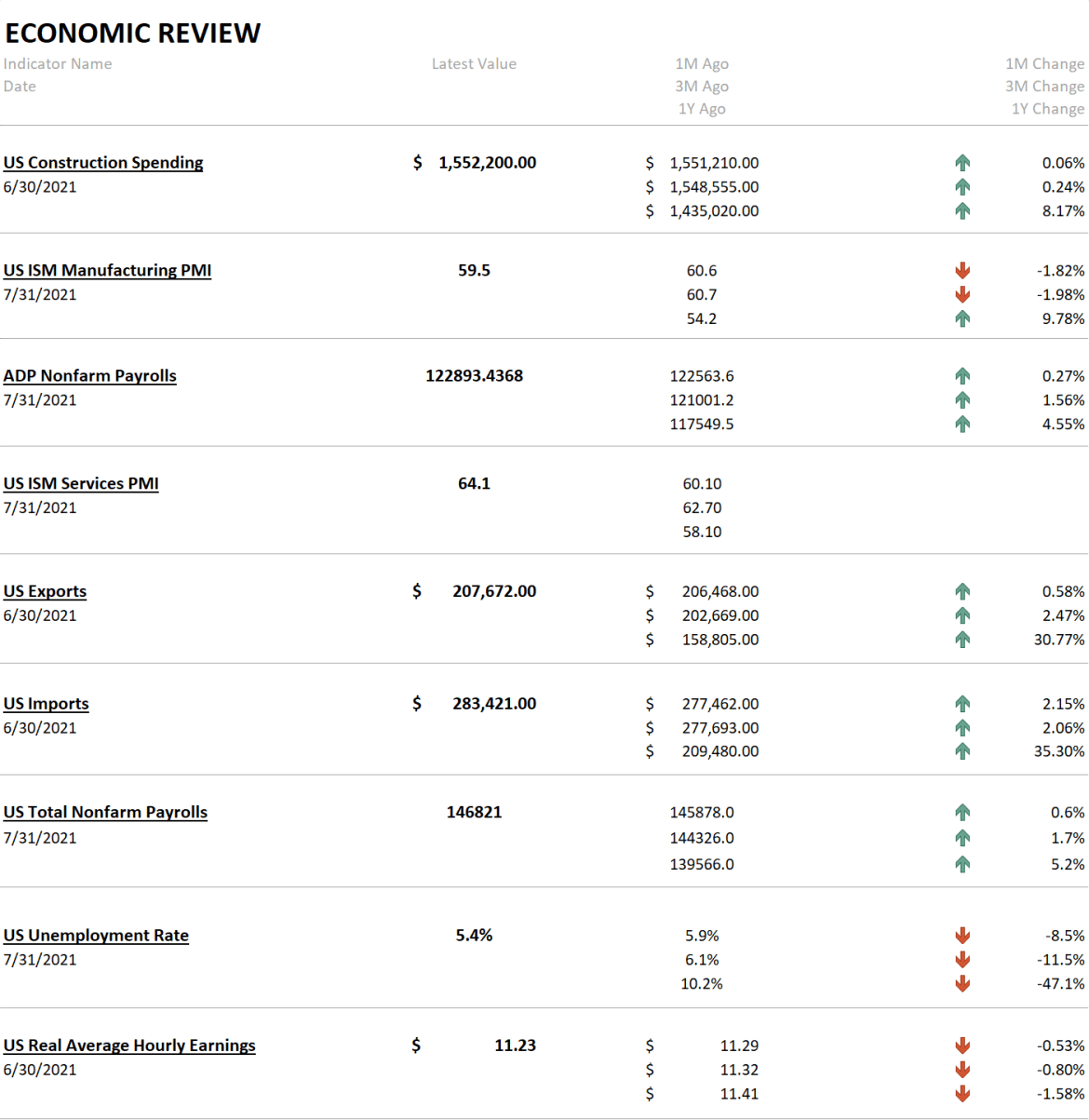

Weekly Market Pulse: As Clear As Mud

Weekly Market Pulse: As Clear As Mud19 Jul 2021

And Now Three Huge PPIs Which Still Don’t Matter One Bit In Bond Market

And Now Three Huge PPIs Which Still Don’t Matter One Bit In Bond Market15 Jul 2021