Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

Weekly Market Pulse: The Turkey Leg

Weekly Market Pulse: The Turkey Leg23 Jun 2025

Weekly Market Pulse: No Free Lunches

Weekly Market Pulse: No Free Lunches19 May 2025

Weekly Market Pulse: Just A Little Volatility

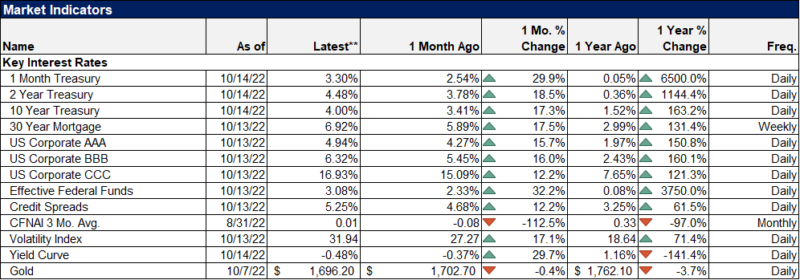

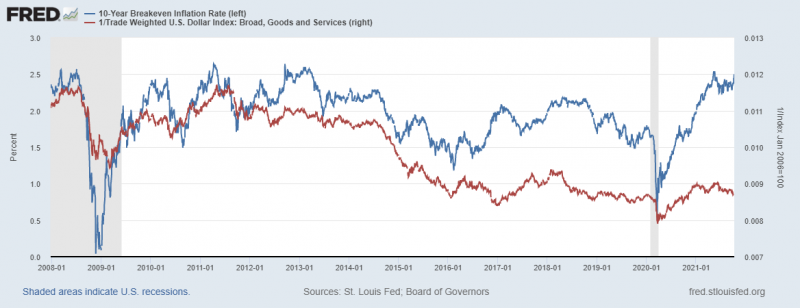

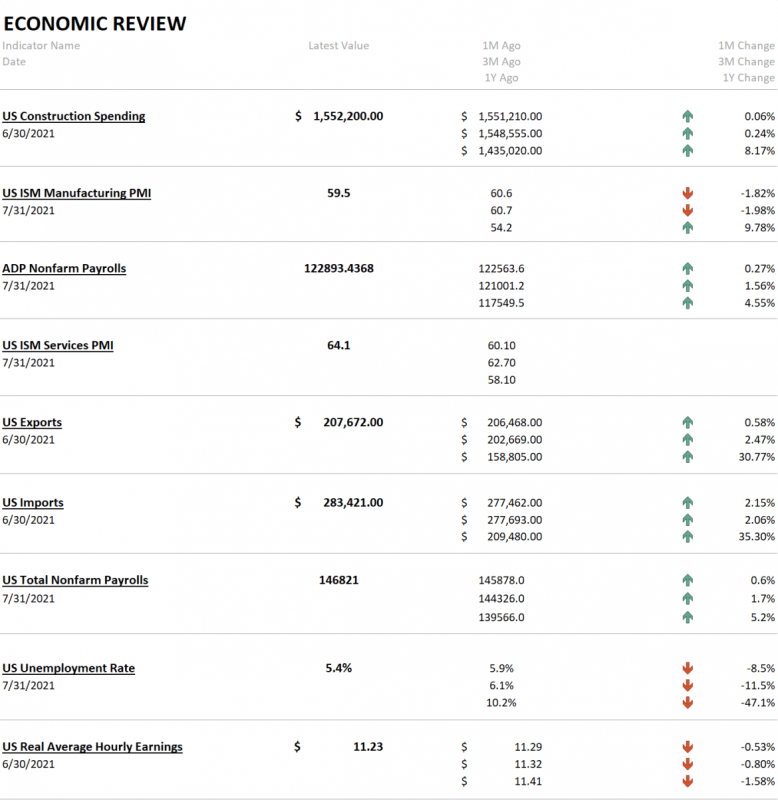

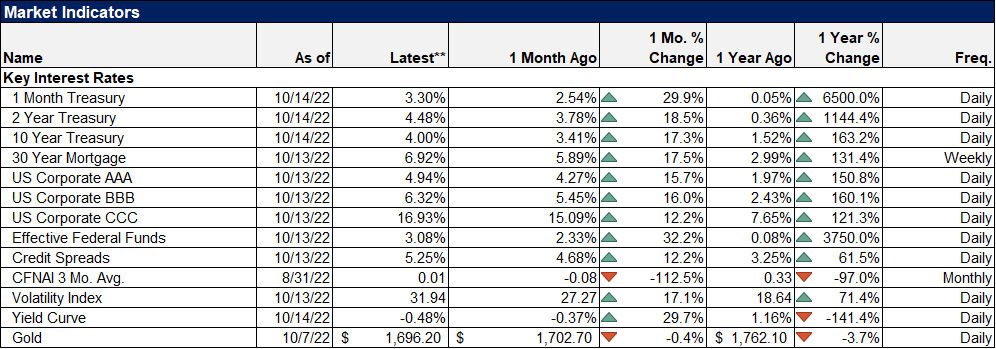

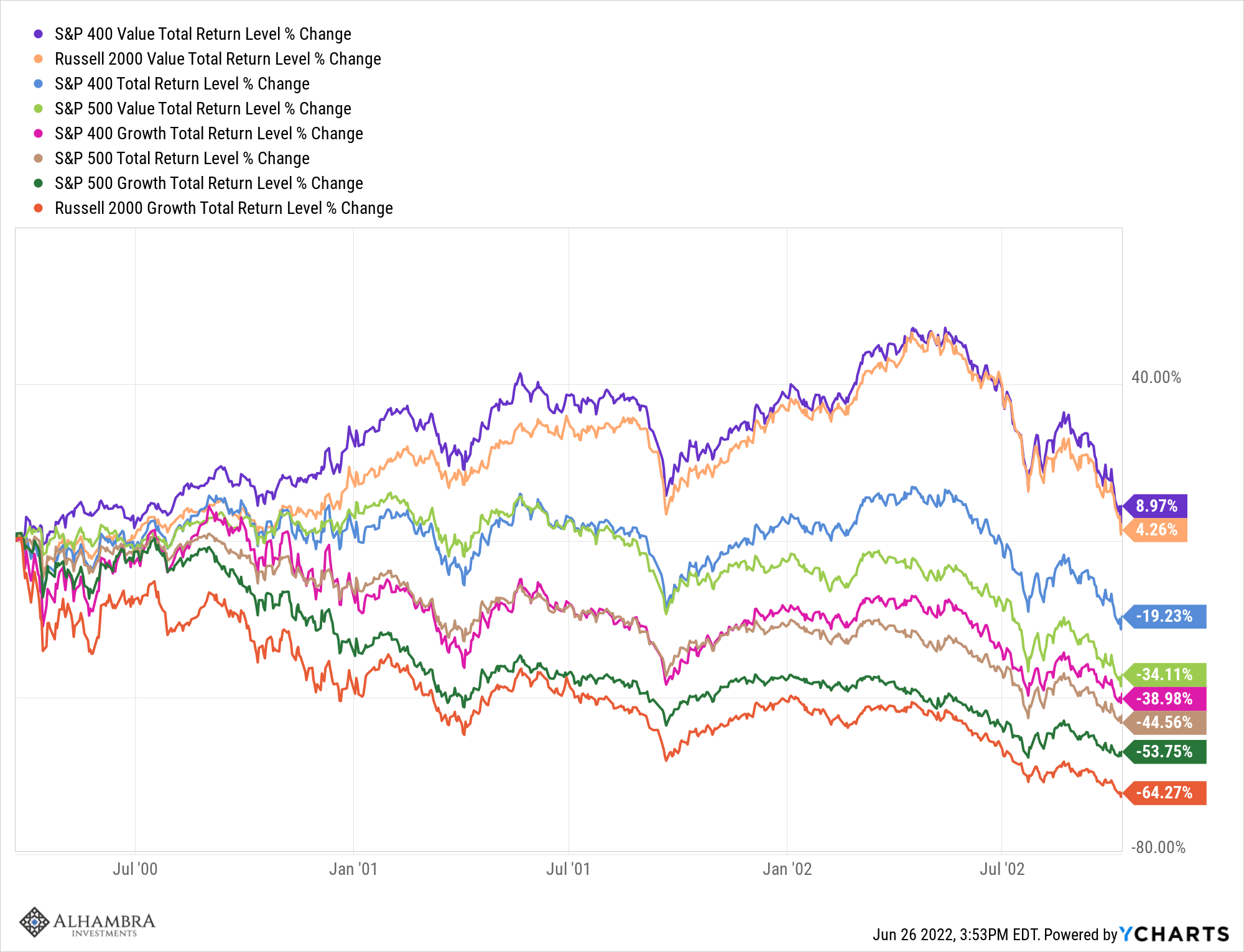

Weekly Market Pulse: Just A Little Volatility17 Oct 2022

Weekly Market Pulse: Peak Pessimism?3 Oct 2022

Weekly Market Pulse: No News Is…12 Sep 2022

Weekly Market Pulse: Opposite George

Weekly Market Pulse: Opposite George1 Aug 2022

Weekly Market Pulse: Expand Your Horizons

Weekly Market Pulse: Expand Your Horizons29 Jun 2022

Market Pulse: Mid-Year Update

Market Pulse: Mid-Year Update24 Jun 2022

One Shock Case For ‘Irrational Exuberance’ Reaching A Quarter-Century22 Dec 2021

Weekly Market Pulse: Has Inflation Peaked?

Weekly Market Pulse: Has Inflation Peaked?13 Dec 2021

Weekly Market Pulse: Discounting The Future7 Dec 2021

Weekly Market Pulse: Growth Scare?

Weekly Market Pulse: Growth Scare?1 Nov 2021

Short Run TIPS, LT Flat, Basically Awful Real(ity)28 Oct 2021

Weekly Market Pulse: Inflation Scare!

Weekly Market Pulse: Inflation Scare!25 Oct 2021

Weekly Market Pulse: Inflation Scare?

Weekly Market Pulse: Inflation Scare?11 Oct 2021

Weekly Market Pulse: Zooming Out3 Oct 2021

Weekly Market Pulse: What Is Today’s New Normal?

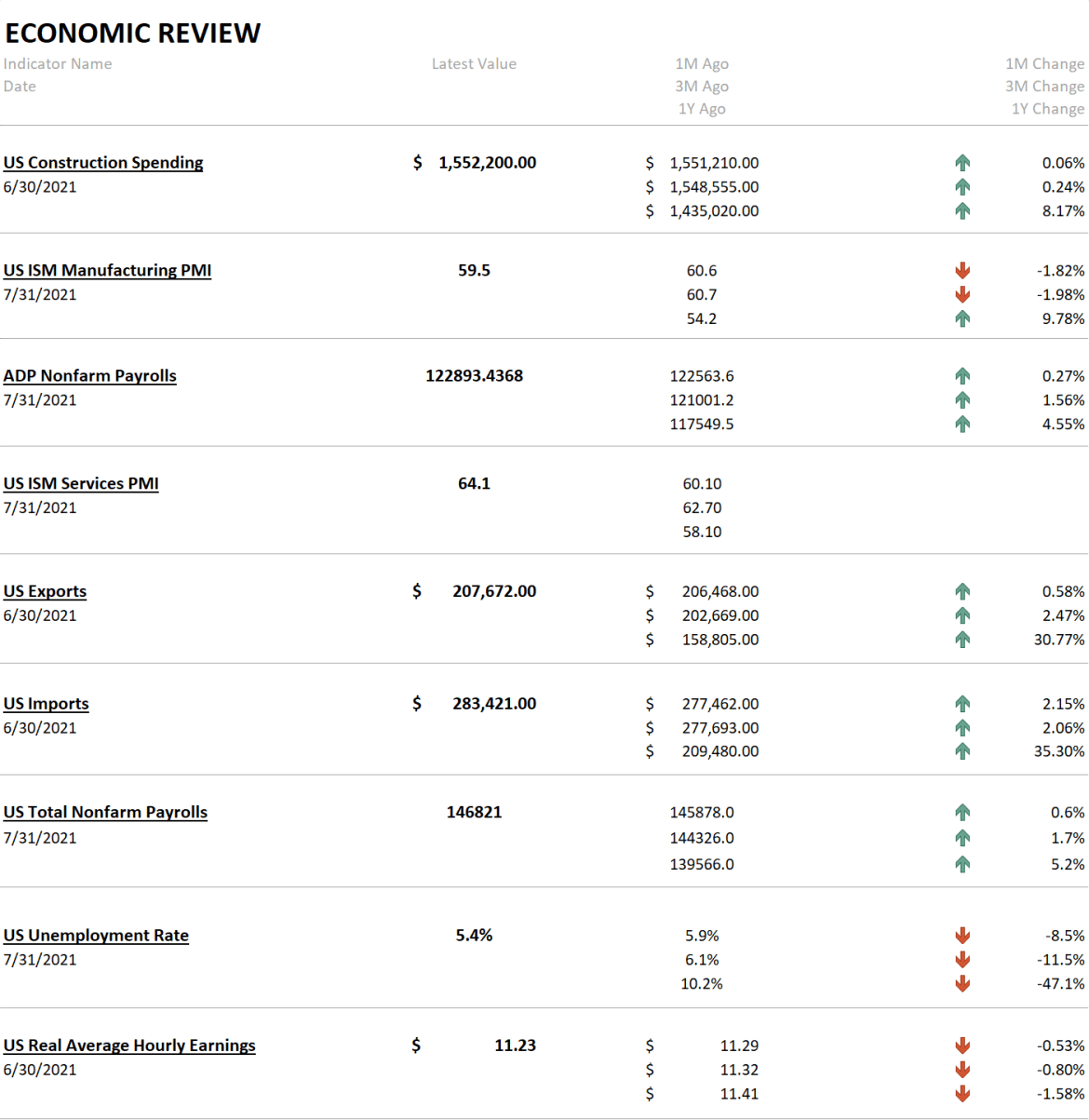

Weekly Market Pulse: What Is Today’s New Normal?9 Aug 2021

Golden Collateral Checking27 Jul 2021

Weekly Market Pulse: As Clear As Mud19 Jul 2021

And Now Three Huge PPIs Which Still Don’t Matter One Bit In Bond Market15 Jul 2021