Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

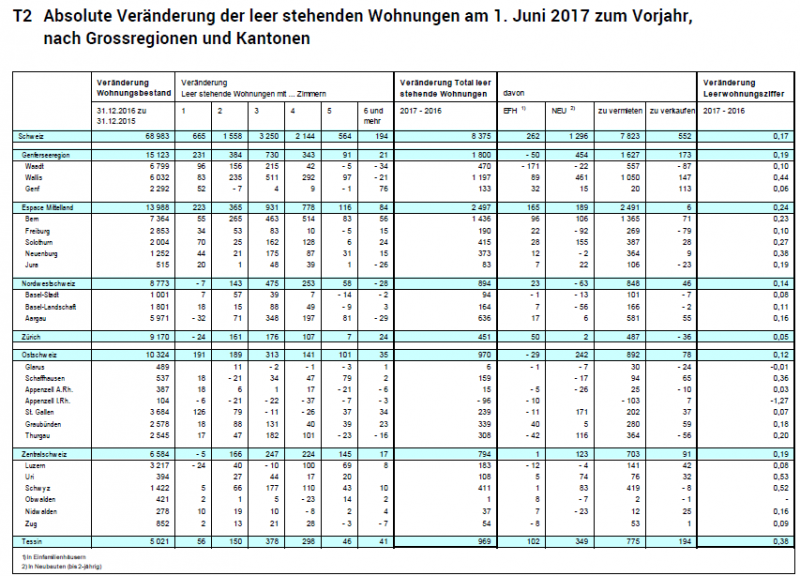

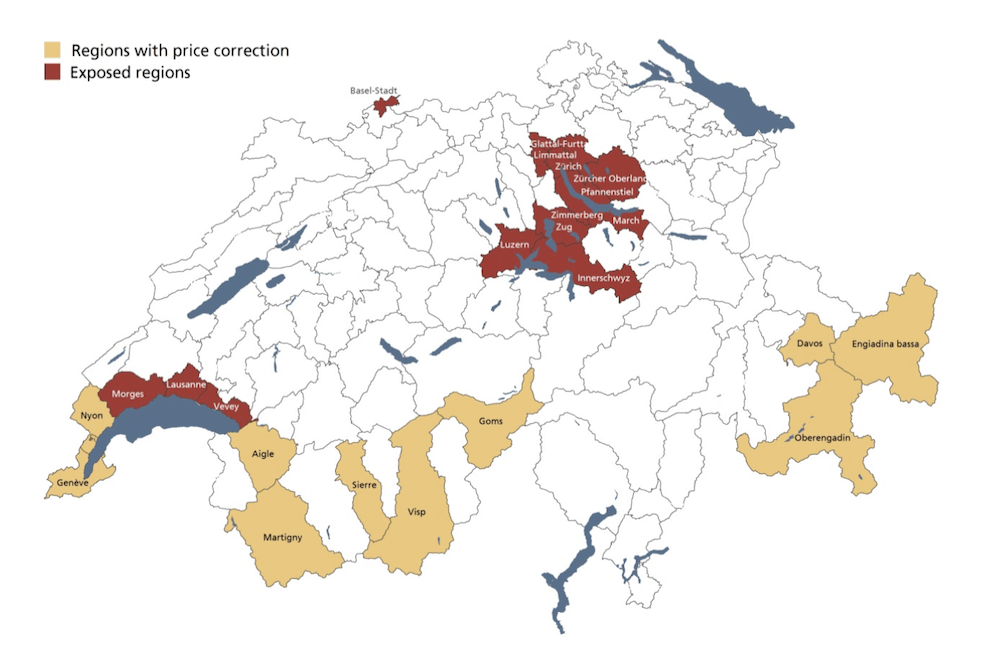

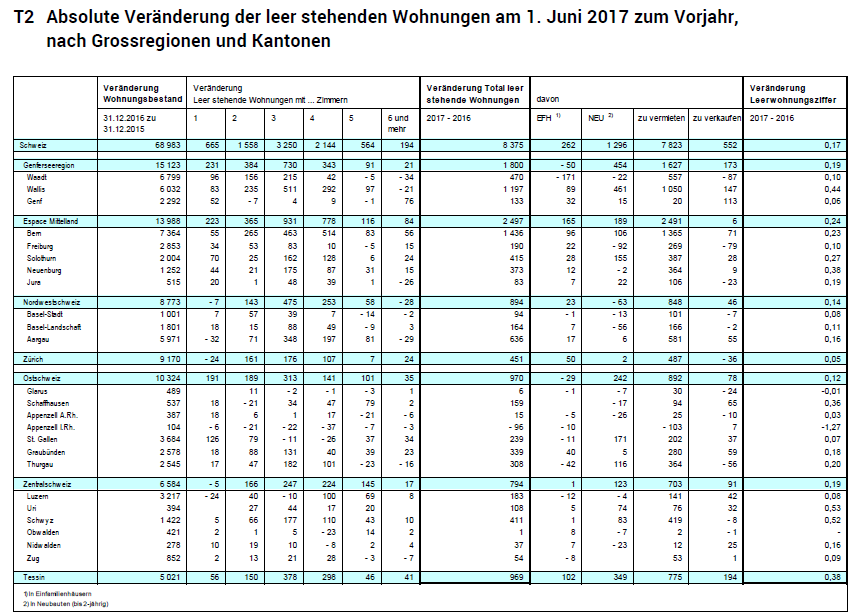

Housing vacancies rise in 20 Swiss cantons

Housing vacancies rise in 20 Swiss cantons13 Sep 2019

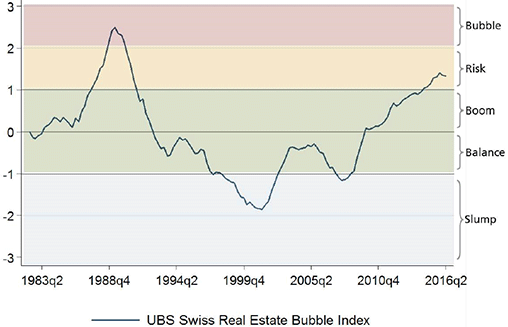

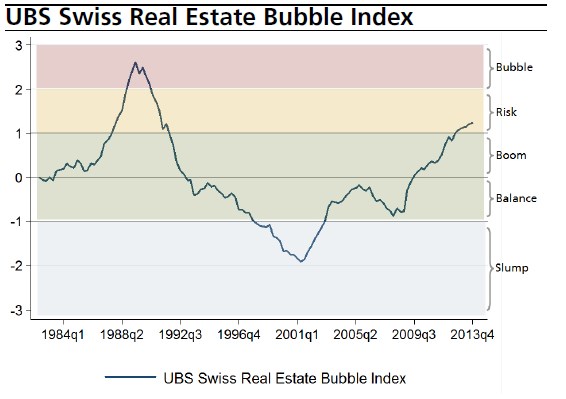

Swiss real estate risk falls two quarters in a row, says UBS

Swiss real estate risk falls two quarters in a row, says UBS9 Feb 2018

Swiss Real Estate: The Empty Dwellings Rate Continues to Increase

Swiss Real Estate: The Empty Dwellings Rate Continues to Increase11 Sep 2017

Swiss home vacancy rate climbs to 15-year high

Swiss home vacancy rate climbs to 15-year high12 Sep 2016

Swiss Real Estate Bubble Index 2Q 2016 continues falling, Still in Risk Zone10 Aug 2016

Update 2014: Swiss home price to income ratio small in historic and global comparison

Update 2014: Swiss home price to income ratio small in historic and global comparison15 Apr 2014

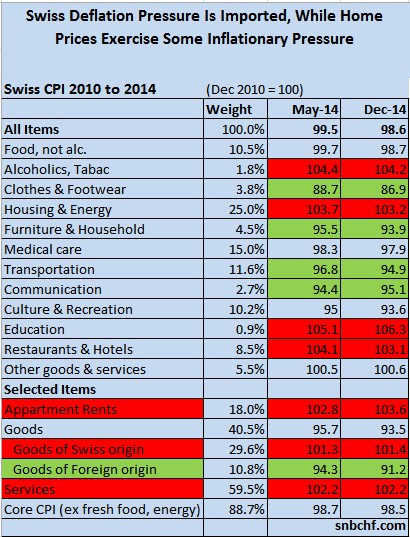

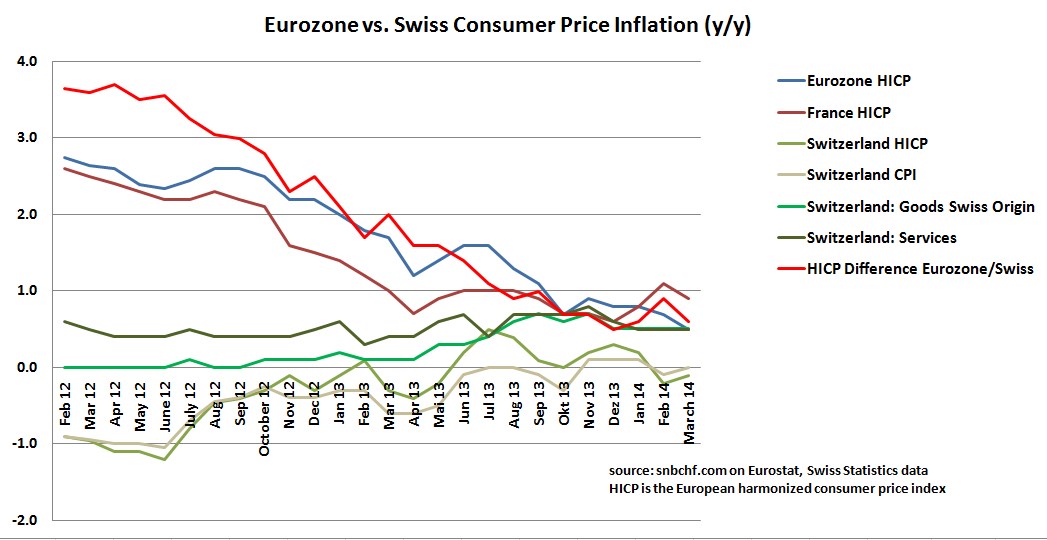

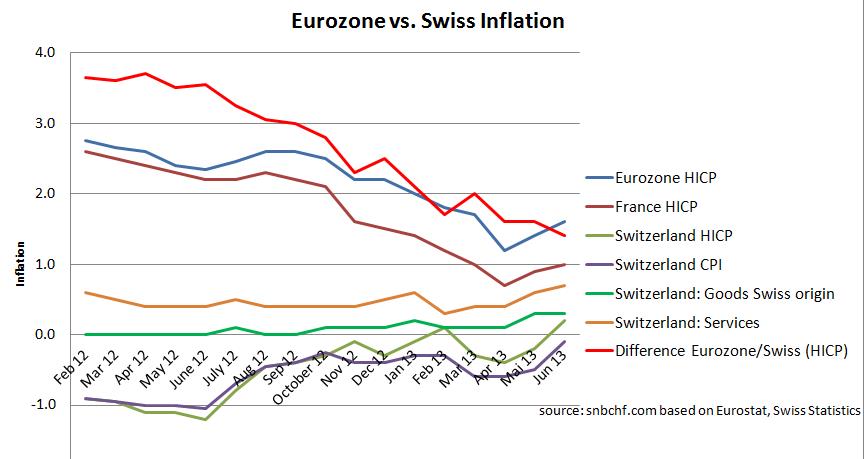

Swiss Yearly Inflation Rate Overtakes First Eurozone Countries

Swiss Yearly Inflation Rate Overtakes First Eurozone Countries11 Apr 2014

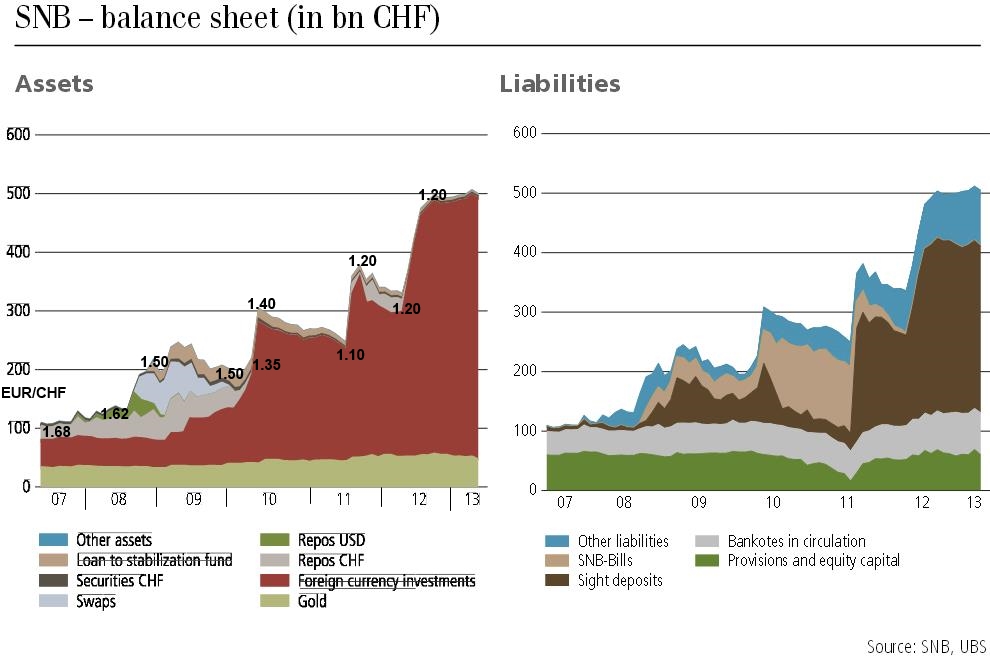

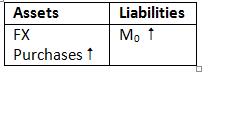

No SNB Intervention: Massive Swiss M0 Increase due to Post Finance Transformation into a Bank

No SNB Intervention: Massive Swiss M0 Increase due to Post Finance Transformation into a Bank1 Sep 2013

Our Detailed Estimate of SNB Q2 Results: 17 Billion Francs Loss, The Reality 18 Billion

Our Detailed Estimate of SNB Q2 Results: 17 Billion Francs Loss, The Reality 18 Billion30 Jul 2013

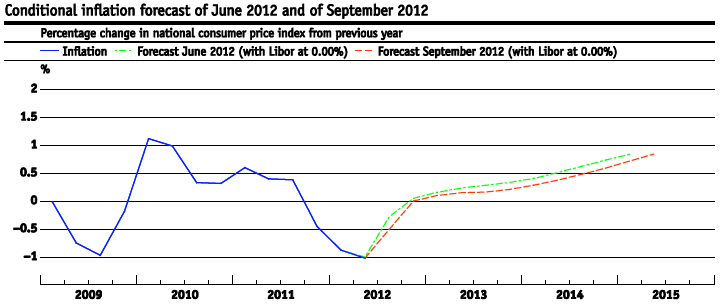

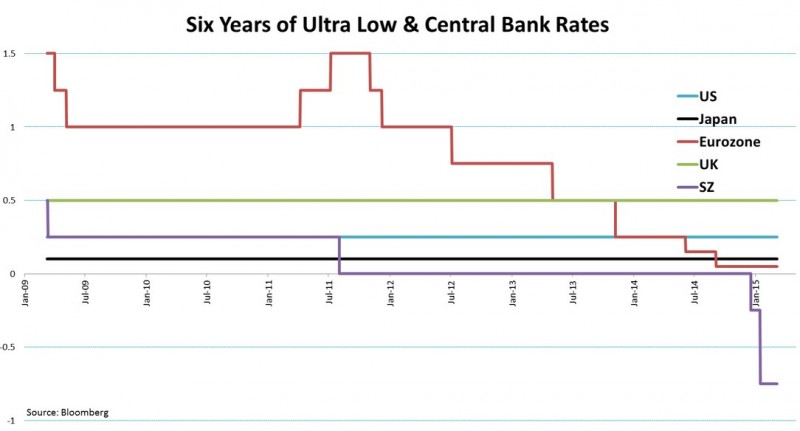

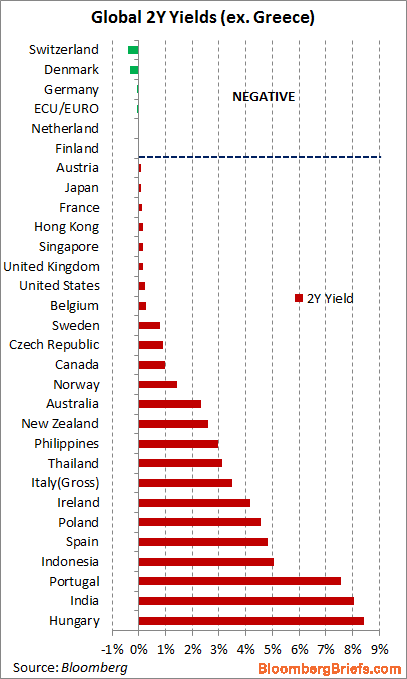

The End of Swiss Deflation

The End of Swiss Deflation5 Jul 2013

Danthine’s Latest Statements Imply that SNB Might Remove Cap in 2014

Danthine’s Latest Statements Imply that SNB Might Remove Cap in 201411 Jun 2013

SNB to Follow the Bank of Japan? Part1

SNB to Follow the Bank of Japan? Part14 Jun 2013

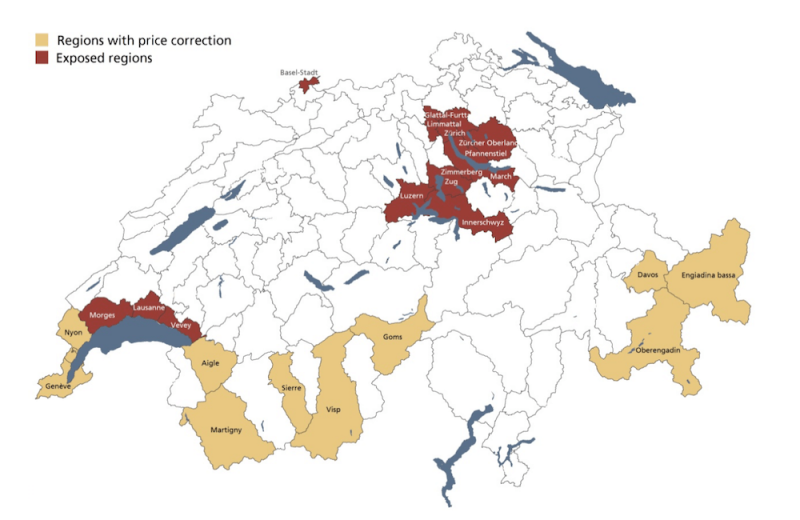

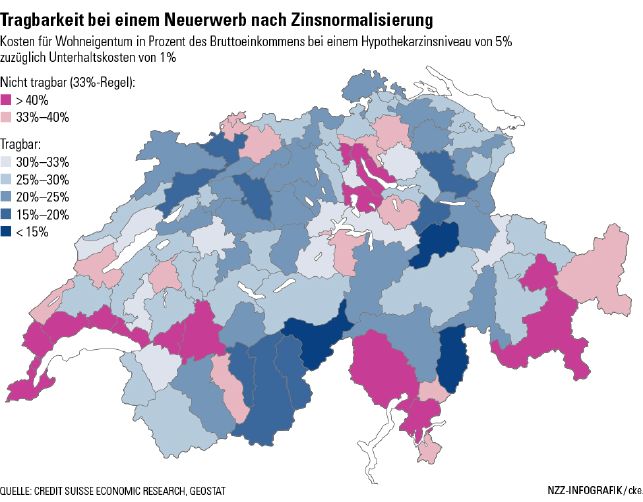

Credit Suisse Study: Swiss Real Estate Market Needs Higher Rates

Credit Suisse Study: Swiss Real Estate Market Needs Higher Rates7 Mar 2013

SNB Sight Deposits Rise by 100 Million CHF, Week January28

SNB Sight Deposits Rise by 100 Million CHF, Week January2828 Jan 2013

10 Jan 2013

17 Dec 2012

How Currency Speculators Help the SNB to Fight against Ordinary Investors

How Currency Speculators Help the SNB to Fight against Ordinary Investors5 Dec 2012

Standard and Poor’s critique of the Swiss National Bank, part 1

Standard and Poor’s critique of the Swiss National Bank, part 126 Sep 2012

Can The SNB Make Profit On Currency Reserves ?

Can The SNB Make Profit On Currency Reserves ?19 Sep 2012

The Big Swiss Faustian Bargain: Differences between SNB, ECB and Fed Money Printing Explained

The Big Swiss Faustian Bargain: Differences between SNB, ECB and Fed Money Printing Explained3 Sep 2012