Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

Swiss FrancThe Euro has fallen by 0.04% to 1.0934 |

EUR/CHF and USD/CHF, June 07(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: After falling to 1.55% after the US employment data, which, while mixing expectations, could hardly be considered weak, the US 10-year yield has come back firmer today (1.58%) This may be lending the greenback a better tone. Equity markets are quiet. Most markets in the Asia Pacific region edged higher. Australia, Taiwan, and Hong Kong were notable exceptions. Europe’s Dow Jones Stoxx 600 made a marginal new record high but is consolidating before the US session. Futures on the major US indices are a little heavier. European bond yields are slightly higher. Most seem to expect the ECB to affirm its current pace of bond buying at this week’s meeting. However, as we have noted, the euro, European interest rates, and the premia over German Bunds have risen since the ECB stepped up its purchases in mid-March. Doubts over the UK’s ability to fully open on June 21 may be favoring some profit-taking on sterling, which is the weakest of the majors, off about 0.2%. Emerging market currencies are narrowly mixed. AMLO’s party and alliance lost seats in the lower chamber as a result of yesterday’s election, and the diluted mandate has seen the peso trade higher. It is competing with the Turkish lira for the best performing emerging market currency today. Firm US rates and dollar are dragging gold lower after the yellow metal rebounded from around $1856 to $1896 on the back of the drop in US rates following the jobs report. The near-term risk extends toward $1876. July WTI tested the $70 a barrel level and paused. Other industrial commodities are trading with a modest downside bias. |

FX Performance, June 07 - Click to enlarge |

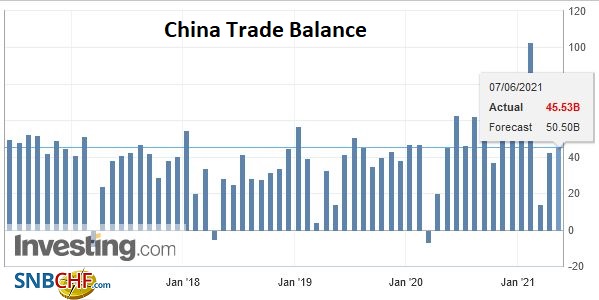

ChinaChina reported a $45.5 bln trade surplus in May. It reflected somewhat slower export growth of 27.9% in dollar terms (32.3% in April, year-over-year), while imports rose 51.1% (43.1% in April). In addition, the rise in industrial metal prices bolstered imports. Consider that iron ore and concentrate imports rose by over 85% in the first five months of the year, while only about 6% in volume terms. Similarly, copper imports are up almost 54.5% in value and 6.4% in volume. Chinese exports to the US were firm at 21% and 13% to the EU. Exports to India doubled year-over-year. There has also been a shift in China’s export mix. Textile and fabric exports, which include PPE and the like, fell by over 40%. Meanwhile, exports of household appliances and lighting rose sharply. There were some distortions in the data the make future projections difficult. There were fewer working days in May, and Guangzhou ports were disrupted by contagion. Separately, China reported that May reserves rose by $23 bln to $3.22 trillion. It was the second monthly increase after declining in Q1 (as the dollar strengthened). Reserves have risen by about $5 bln net this year and are about $120 bln above last May’s level. |

China Trade Balance, May 2021(see more posts on China Trade Balance, ) Source: Investing.com - Click to enlarge |

Asia Pacific

Japanese corporate sponsors of the Olympics called for a delay in the games until the vaccine rollout, which is accelerating, allows more spectators. A decision on local spectators is expected around June 24. However, as the inoculations increase and athletes begin arriving, fait accompli is palatable, and the opposition to holding the games may be waning. A Yomiuri survey found 50% now say the Olympics should move forward, up from 39% last month. A separate survey from TBS found 44% favoring the Olympic games, up from 35% in May. However, it does not appear to have helped Prime Minister Suga very much. In both polls, his support is at its lowest since he replaced Abe last September.

The dollar has been confined to about a 15-tick range on either side of JPY109.50, where a $1.25 bln option expires today and another for around $950 mln expires tomorrow. The greenback is holding above the 20-day moving average (~JPY109.30), the lower end of last week’s range. The intraday technicals favor the upside in the North American morning.

The Australian dollar has edged a little higher to reach $0.7755, about a tenth of a cent above the pre-weekend high. Last week’s high was set near $0.7775. Here, too, the intraday technicals favor a firmer US dollar. Initial support is around $0.7720. The greenback is steady against the Chinese yuan, trading within the previous session’s range. The PBOC set the dollar’s reference rate well above expectations: CNY6.3963 vs. CNY6.3931, suggesting officials are not content.

Europe

The poor German state, Saxony-Anhalt, held elections yesterday, and the CDU did better than expected. It garnered 37% of the vote, up from 30% in the previous election. The AfD that some polls had shown running neck-to-neck faded with 22% of the vote, down from 34%. The Left and SPD saw their support also wane. The Greens, which are running second nationally, do not typically do well in the former East German state, saw its support rise to a little over 6% from 5%. These results, coupled with recent national polls, give the CDU the advantage going to the summer, ahead of the September election.

Separately, Germany disappointed with a 0.2% decline in April factor orders. Bloomberg’s survey found a median forecast for a 0.5% gain. However, the sting may have been mitigated by the revision to the March series to 3.9% from 3.0%. Still, the drop in orders may not bode well for tomorrow’s industrial production figures, where the survey expected a 0.4% gain after a 2.5% rise in March. Recall that the April manufacturing PMI slipped to 66.2 from 66.6 in March. In May, eased further to 64.4 but remains in strong expansion territory. On the other hand, Spain’s April industrial production jumped 1.2%, more than twice the median forecast in Bloomberg’s survey. The March series was revised to 0.6% from 0.4%.

There are two developments in the UK to note. First, Health Secretary Hancock reiterated his assessment that it is too early to say whether the UK can proceed with its economy-wide re-opening on June 21 as planned. Second, a sufficient number of Tory MPs look to join the opposition in defeating the government’s push to cut foreign aid spending to 0.5% of GDP from 0.7%. It would not be a major defeat for the Johnson government–more embarrassing than substantive.

The euro rebounded from more than three-week lows (~$1.2105) on the back of the US jobs data. It stalled near $1.2185 and slipped to around $1.2145 today. It has held below the five and 20-day moving averages, which converge in the $1.2175-$1.2180 area. Today is the fourth session that the single currency is recording lower highs. The week’s big events, US CPI and the ECB meeting lie ahead, and some brief consolidation ought not to be surprising.

Sterling is also trading inside its pre-weekend range and has slipped back below the five and 20-day moving averages that converge near $1.4145. Support is seen in the $1.4080-$1.4100 area.

America

The UK hosted the G7 finance minister meeting, but the US appeared to come out the victor as the 15% minimum corporate tax rate was agreed. In some ways, the Biden administration needed the agreement to boost the chances of passing its own corporate tax bill. Moreover, US tax reforms have been unable to stop companies from booking profits in the tax havens. Similarly, the EU has not been able to persuade several of its members, including Ireland, the Netherlands, and Luxembourg, from providing those tax havens. An international agreement will help both in their domestic battles. On the other hand, having some taxes be paid to local governments where the sales are made will help the US and Europe, where the bulk of local sales are made. Several of the multinationals that would be impacted appear to have endorsed the reforms.

Tomorrow, the US Senate is likely to vote in favor of the “US Innovation and Competition Act that cobbles together several bills aimed at bolstering US research and development and competitiveness. Two important aspects of the bill stand out. First, it includes measures, like support for the semiconductor industry, that will allow the Biden Administration to compromise over some infrastructure spending that shifts to this bill. Second, the bill appears to be among the closest to being bipartisan. It is sponsored by Senators from both parties. That said, a majority of Republicans are not expected to support the measure, though there appears to be an underlying consensus.

Mexico’s legislative and local elections did not go particularly well for AMLO, his Morena party, or the governing coalition. The results mean that it will be more difficult to enact large-scale changes, including in the energy sector. The Morena party itself appears to have lost 50-65 of its 253 seats, as support eased 35%-36% of the vote, down from nearly 37.5% in 2018. Peru held a run-off election for president, and it still appears to close to call. Fujimori held a small advantage. In 2016, it took several days for the victor to emerge.

The Canadian dollar is trading quietly near unchanged levels. The focus is on the Bank of Canada meeting at mid-week. Two months of job losses are seen as shaping the official rhetoric. In April, the Bank announced it was slowing its bond purchases and anticipated that the output gap would close in H2 22. It is unlikely to back away from the assessment but could emphasize the uncertainty and unevenness of the recovery. The market has moved to discount three rate hikes over the next two years. Officials may want to temper expectations a little and take some pressure off the Canadian dollar, which has risen by around 3.4% since the April meeting, the most among the major currencies. The CAD1.20 area remains critical support, while the CAD1.2145 area is the nearby cap.

The Mexican peso is bid. The greenback has been sold through last week’s lows (~MXN19.8460). The next area of support is seen around MXN19.78-MXN19.80. The highlight for the week for Mexico is the mid-week CPI report. It could be the first time this year that the year-over-year pace eases, but it will remain sufficiently elevated for the market to continue to look for a rate hike in late Q3 or early Q4.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,China,Currency Movement,EUR/CHF,Featured,Germany,Mexico,newsletter,Taxes,U.K.,USD/CHF