On Tuesday, Kevin Warsh appeared before the Senate for his nomination hearing for the Fed Chair. The biggest takeaway is Warsh's desire to "reform" the Fed. Based on his appearance, reform seems to cover the following three areas:

- Public Communications: Warsh stated clearly that he doesn't believe in forward guidance. This seems to be a stark departure from prior Fed members, who presumed that the more the markets knew what the Fed was thinking, the less likely policy actions would shock the markets. Taking a step back from forward guidance could result in stock and bond market volatility, as investors are less clear about the future path of interest rates.

- Economic Models: Warsh is not comfortable with the Fed's current inflation models. He seems to advocate a trimmed-mean inflation reading. Trimmed mean models strip out the outliers with the intention of filtering out one-off price swings that can distort inflation readings. As we share in the graphic below, the trimmed mean is less volatile. At 2.33%, it is also running about half a percentage point below the headline PCE price index.

- Fed Balance Sheet: He has advocated against QE since the GFC, despite voting for it as a Fed member during the crisis.

Regarding current monetary policy, Warsh believes inflation is lower than official indicators state. We have noted this as well with the Truflation data. He acknowledges that while the inflation path is trending lower, "there's more work to do." Further, while he may be open to cutting rates slightly, he came off as hawkish as he wants to reduce the Fed's balance sheet. To wit, consider the following quote:

QE is reverse Robin Hood. It’s policy that steals from the poor, to give to the rich.

What To Watch Today

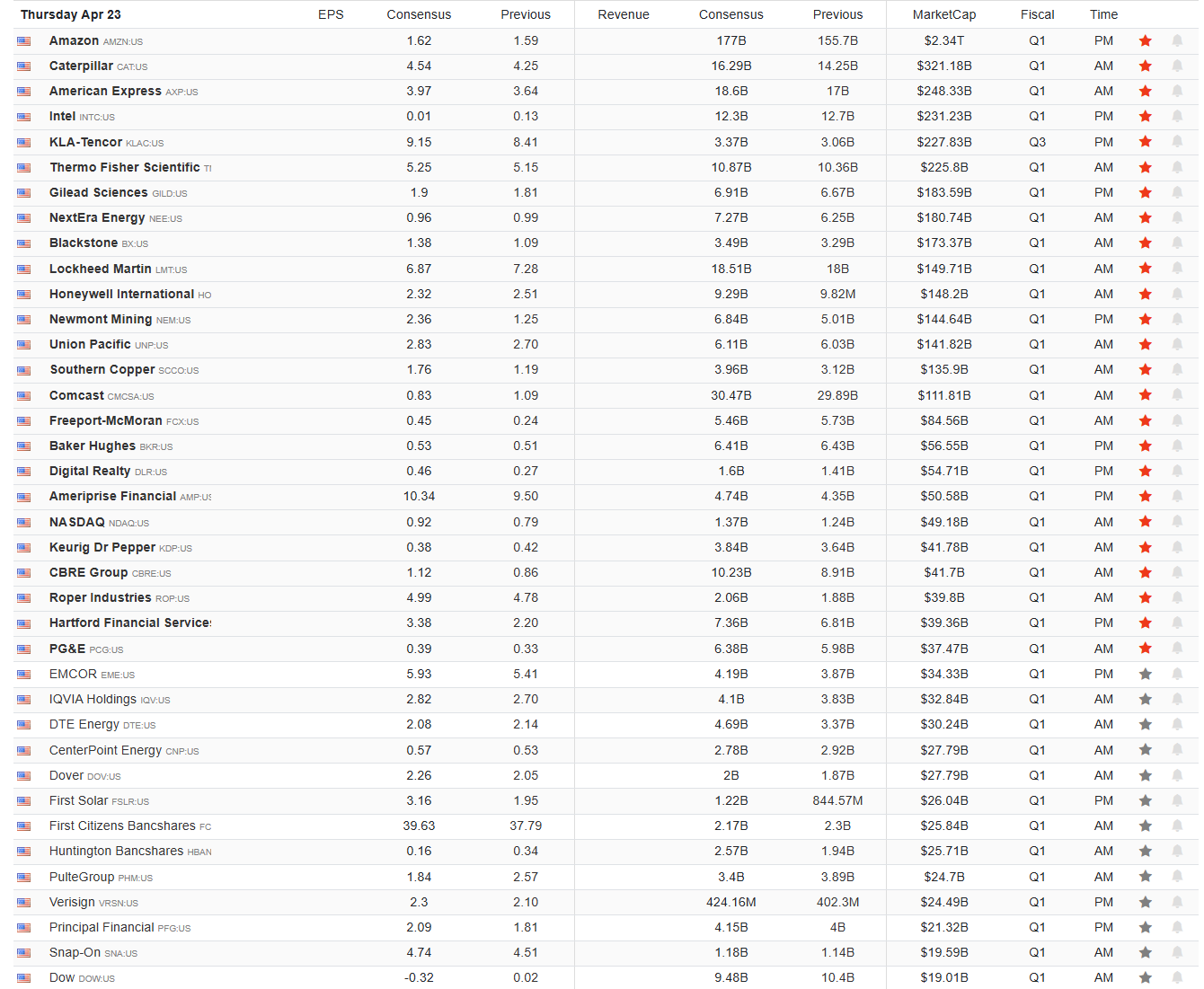

Earnings

Economy

Market Trading Update

Yesterday, we discussed the dollar and why a stronger market will likely continue to track foreign inflows into US markets. However, this raises another question I received during our live Q&A session on the RealInvestmentShow yesterday.

"Why is the market ignoring the risk arising from the shuttering of the Strait of Hormuz?"

It's a good question, and honestly one that I have repeatedly considered over the last month as the events in Iran unfolded. Here is my best guess as to why the "doomsayer" case has been wrong, at least so far.

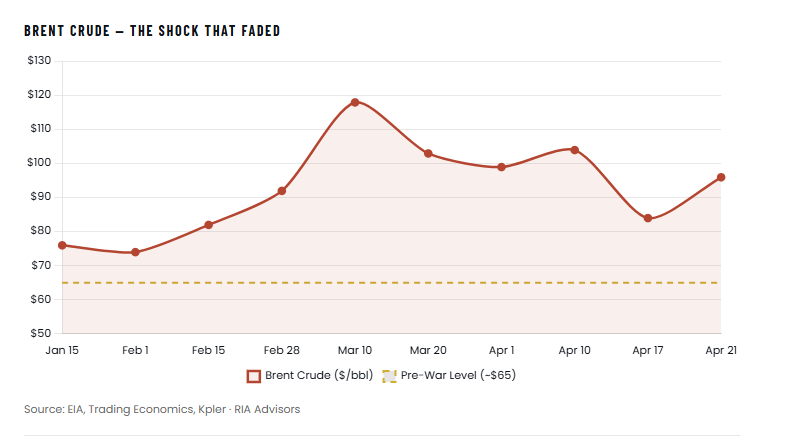

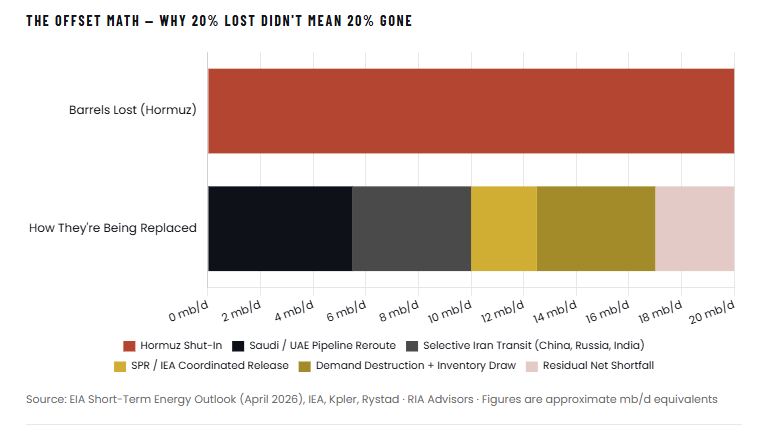

- First, "closed" was always a headline, not a fact. Saudi Arabia and the UAE rerouted 5 to 6 million barrels a day through pipelines terminating at the Red Sea and the Gulf of Oman. By late March, Iran had selectively reopened the strait to tankers flagged by China, Russia, India, Iraq, and Pakistan. The chokepoint wasn't sealed. It was rationed.

- Second, strategic reserves actually functioned for once. The IEA coordinated a 400-million-barrel release, the largest in its history, with the U.S. SPR alone putting 1.4 million barrels a day on the water. That doesn't replace lost volume, but it blunts speculative panic while physical workarounds take hold.

- Third, China was the biggest tail risk and China came in loaded. Commercial inventories sat near one billion barrels heading into the crisis, with another 360 million barrels of state reserve behind that. Iran granting Chinese tankers transit removed the rest of the downside. Beijing was never going to let this crack its economy, and it hasn't.

- Fourth, the U.S. is structurally insulated. We produce more than 13 million barrels a day, we're the world's largest LNG exporter at 18 billion cubic feet daily, and less than 10% of our crude runs through Hormuz. In a global shock, the U.S. becomes the marginal supplier, not the marginal victim.

Now to the harder question. If the U.S. supply is offsetting the crisis, does that set up an oversupply collapse when the strait reopens? Here's where I think the back end of the curve is mispriced. When Hormuz fully reopens, three things hit the market at once. Gulf producers restart roughly 9 million barrels a day of shut-in capacity. Tankers jammed up in the regional storage unload. U.S. shale, recapitalized by $95 crude, keeps pumping. That's a textbook glut setup.

The offset is SPR rebuilding. Thirty-plus IEA countries have drained strategic stockpiles, and they'll spend the back half of 2026 refilling. That creates real physical demand. Kpler already argues late-2026 Brent at $74 is undervalued. But the window between reopening and restocking acceleration could get violent. I'd expect a move back into the low $70s within 90 days of a durable ceasefire, with overshoot risk toward $60 if demand destruction lingers.

Here is the thing: I think the markets have already priced in all this.

If the supply shock really has been buffered, the market has already done the math and moved on. That's what price action is telling us. The S&P 500 has pushed through Hormuz headlines the same way it pushed through tariffs, Fed succession noise, and March's banking tremors. At some point, markets stop pricing risks they've already metabolized.

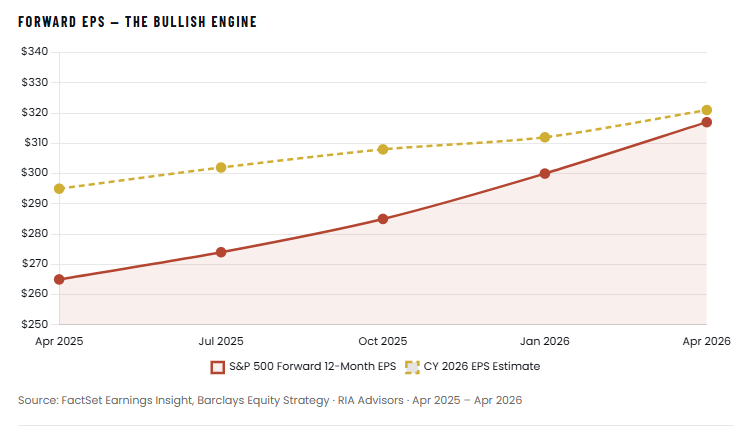

What replaces geopolitics as the driver? Earnings. And here the data is unambiguously bullish. With 10% of the S&P 500 reporting for Q1, 88% have beaten EPS estimates, well above the 10-year average of 76%. The aggregate beat sits at 10.8%, versus a historical 7.1%. Analysts have revised full-year 2026 earnings growth to 18%. Forward 12-month EPS has pushed the bottom-up index target to roughly $7,350, up 13% from the May 14 low. The estimated 2026 net margin of 13.9% would be the highest on record.

Do I buy the whole bullish read? Mostly, with a caveat. Stocks do follow earnings over time, and the earnings trajectory here is genuinely strong. But forward estimates almost always rise until they don't. That's the normal pattern, not a signal. The forward 12-month P/E is 20.9, above both the 5-year (19.9) and 10-year (18.9) averages. At those multiples, a clean beat earns a muted reaction, and any Q2 guidance that embeds the $4+ gasoline hit to the consumer gets punished hard. The market is right to pivot. It's also walking a thinner ledge than the headlines suggest.

Bottom line: The market isn't wrong to be calm about Hormuz, and it isn't wrong to be bid up on earnings. The risk isn't on the geopolitical side anymore. It's whether forward EPS estimates hold when Q2 guides land, and whether the back end of the oil curve dislocates before SPR restocking can absorb the returning Gulf supply. Both are the other side of the same trade.

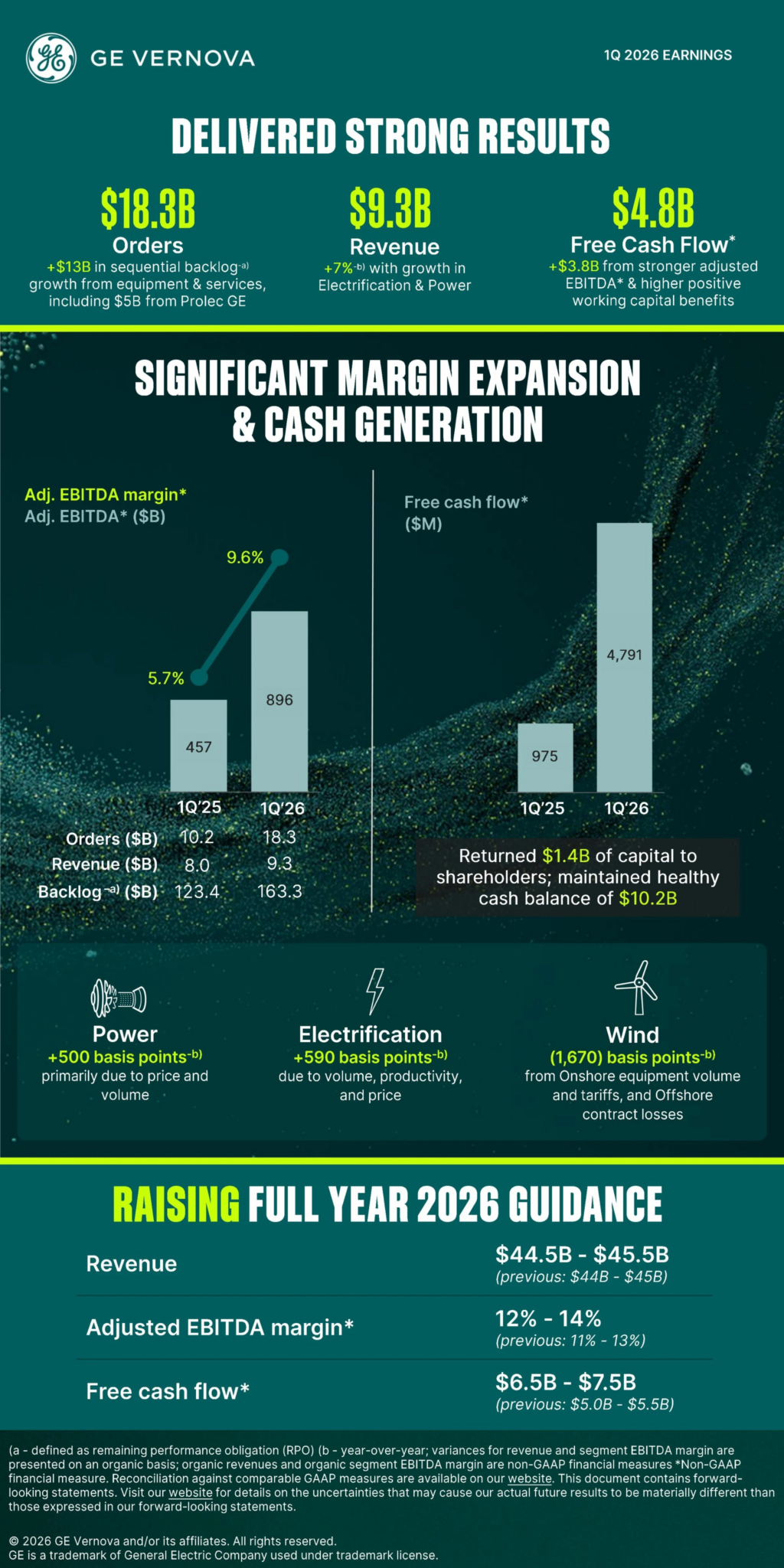

GE Vernova Continues To Beat Expectations

GE Vernova (GEV) stock opened nearly 10% higher after the company handily beat earnings expectations, posting EPS of $2.06, almost 10% above estimates. Revenues beat as well, and forward guidance was increased from already optimistic levels. Importantly, their order backlog grew to $163 billion, representing about four times their current quarterly revenue. GEV stock has risen by nearly 200% over the last year due to its growth surge.

GEV is a primary beneficiary of the AI boom, as it makes the equipment that generates, transmits, and stores electricity, such as gas and wind turbines, as well as grid infrastructure. The quest for power for the massive expansion of data centers is driving outsized demand for its products. The following quote sums up GEV's unique positioning with the AI boom nicely:

“The companies that sell the physical infrastructure for AI data centers are seeing demand faster than they can raise capacity”

GFC 2.0 Or False Alarm: Part Two

The graph below, courtesy of Preqin and the Daily Shot, shows the steady growth of private credit funds since the GFC. The “Dry Powder” category represents committed capital for investment that has not yet been deployed. For what it is worth, that amount is almost identical to the amount of subprime mortgages at their peak. The total global private credit market, including all other lenders, is estimated at around $3.4 trillion.

After the GFC, regulators forced banks to hold more capital and to retreat from riskier lending. As a result, an alternative credit ecosystem grew to replace banks. Private credit funds, business development companies (BDCs), and specialty finance vehicles have filled the gap.

Unlike the various subprime mortgage securities and derivatives, which were largely owned by institutional investors, retail investors have gotten involved in private credit funds. They were tempted with high yields and monthly or quarterly redemption windows.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

The post Can Warsh Reform The Fed appeared first on RIA.

Full story here Are you the author?You Might Also Like

The VIX Is Lying: Or Is It?

The VIX Is Lying: Or Is It?

2026-03-30

Expected and historical (realized) volatility are sending investors a puzzling signal. Because of the Iran conflict, intense oil price swings, and rising interest rates, the VIX, or implied volatility (what options markets are pricing in as future fear), is elevated. However, actual realized volatility has been much more subdued. That gap between the VIX and …

Rubino: Fiat Currencies Are In A Death Spiral

Rubino: Fiat Currencies Are In A Death Spiral

2026-03-27

The fiat currency collapse narrative is one of the most emotionally satisfying arguments in all of financial punditry. It feels intellectually rigorous, draws on genuine history, and speaks to deep and legitimate anxieties about government overreach, monetary recklessness, and the long-term consequences of unlimited debt creation. Monetary analyst John Rubino makes the case as well …

2026-03-26

Albert Edwards from Societe Generale posted a graph similar to the one on the left below. It tracks the unemployment rate and its 3-year moving average. The red arrows signify every time the unemployment rate rose above the moving average. As we circle, the unemployment rate is now above the moving average. Albert’s comment alongside …

Financial Nihilism & The Trap Young Investors Are Walking Into

Financial Nihilism & The Trap Young Investors Are Walking Into

2026-02-13

The article from the Wall Street Journal titled “Why My Generation Is Turning to Financial Nihilism” by Kyla Scanlon argues that Gen Z is embracing high-risk financial behavior out of despair and detachment. Of course, it is essential to recognize that Kyla, although well-intentioned, is a young twenty-something influencer with limited real-life experience, and sees …

Speculative Narrative Unwinds

Speculative Narrative Unwinds

2026-02-09

For nearly two years, markets were driven by the same speculative narrative that “this time is different.” Bitcoin, precious metals, and AI-linked equities rose not only because of robust fundamentals, but also because investors clung to powerful narratives about inflation, disruption, and monetary collapse. Those speculative narratives are not only seductive but also contribute to …

Fannie And Freddie Add Billions To The Bond Market

Fannie And Freddie Add Billions To The Bond Market

2025-12-18

According to Bloomberg, Fannie Mae and Freddie Mac have been increasing the mortgages and mortgage-backed securities they hold on their own balance sheets. At their peak, before the financial crisis, Fannie and Freddie held a combined total of $1.6 trillion in mortgages. As we share below, courtesy of Bloomberg, their portfolio sizes are well below …

Bull Market Genius Is A Dangerous Thing

Bull Market Genius Is A Dangerous Thing

2025-12-15

During extended upward-trending markets that reward risk-takers and punish caution, everyone is a “bull market genius.” That dynamic flips investor psychology and, over time, creates a false sense of control. As the market continues to climb, risk appears to vanish, and investors believe that nothing can go wrong, leading them to take on increasing levels …

Tags: Featured,newsletter