Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

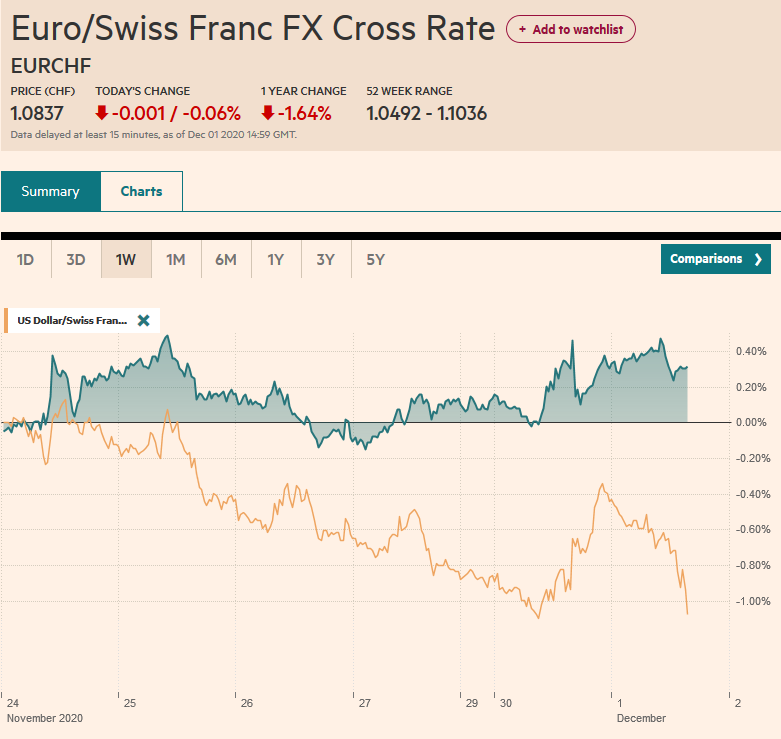

Swiss FrancThe Euro has fallen by 0.06% to 1.0837 |

EUR/CHF and USD/CHF, December 1(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The near-record rallies seen in the major equity markets in November may have contributed to the month-end drama yesterday. There has been no follow-through activity. Stocks bounced back, and the US dollar is heavy, with few exceptions. In the Asia Pacific region, all the markets are higher, and most rose by more than 1%. The European Dow Jones Stoxx 600 is recouping most of yesterday’s 1% loss, and the S&P 500 is nearly 1% higher too. Benchmark yields are most 1-2 basis points firmer in Europe and the US, leaving the 10-year Treasury yield around 0.86%. The dollar is lows against all the major currencies, led by the Scandis. The euro remains within striking distance of the $1.20-level and sterling flirted with $1.34. Emerging market currencies broadly are recovering, and the South African rand and Hungarian forint are leading today’s advance. The Turkish lira is a notable exception, falling for the first time in five sessions. Gold is nearly 1.8% higher and has resurfaced above $1800 an ounce. Oil is little changed with the January WTI contract hovering around $45 a barrel, as OPEC+ has delayed their meetings day amid discord. |

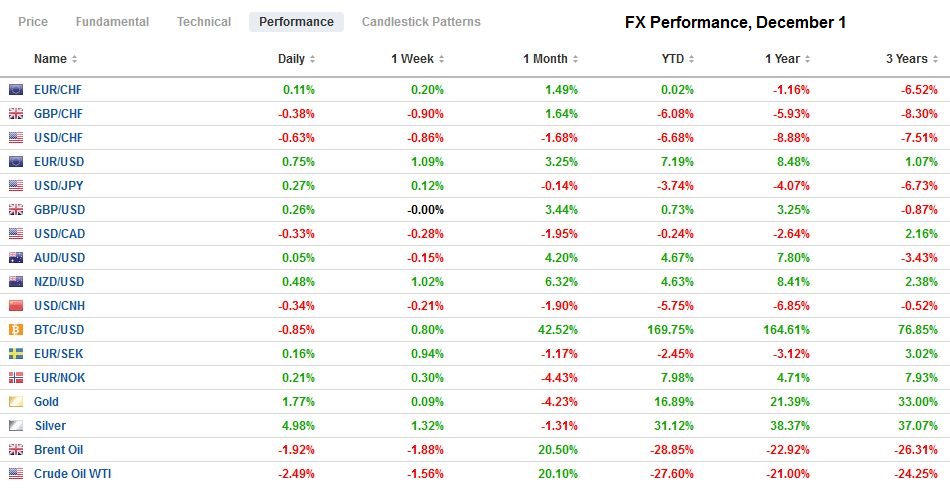

FX Performance, December 1 - Click to enlarge |

Asia Pacific

The Caixin manufacturing survey was considerably stronger than expected at 54.9 from 53.6 in October. This is the highest in a decade and is consistent with the recovery seen in other data. South Korea exports, which are also seen to be driven by Chinese demand, were also strong, rising 4% year-over-year in November after a revised 3.8% decline in October (initially -3.6%). When adjusted for the number of working days, the value of average daily exports rose 6.3%, the most in two years.

The final look at Japan’s November manufacturing PMI revised away the initial decline to 48.3 from 48.7 and instead rose to 49.0, the highest since August 2019. However, the employment situation deteriorated slightly, and the October unemployment rate ticked up to 3.1% from 3.0%. This is a new cyclical high and matches the highest level since 2017. The job-to-applicant ratio rose to 1.04 from 1.03. It stood at 1.58 a year ago.

As widely expected after easing policy last month, the Reserve Bank of Australia stood pat. The RBA says it is ready to do more if needed. Separately, the Markit manufacturing PMI slipped to 55.8 from 56.1 preliminary reading, but still better than October’s 54.2. It was just below 50 a year ago. First thing tomorrow, Australia reports Q3 GDP. It is expected to have expanded by 2.5% in the quarter after a 7.0% contraction in Q2.

The dollar posted an outside up day against the yen yesterday, trading on both sides of the pre-weekend range and closing above the high. Follow-through buying saw the dollar trade around JPY104.45 after peaking yesterday a touch lower (~JPY104.40). Today, it is confined to about a quarter of a yen above JPY104.20. A move above the JPY104.85-JPY105.00 area, which holds about $960 mln in expiring options, would lift the tone. In contrast, the Australian dollar posted an outside down day yesterday. It briefly poked above $0.7400 for the first time since September 1 before selling off to about $0.7340. Today, it has held the low but was capped near $0.7375. The intraday technicals suggest a retest of the session highs could be seen in North American activity. The PBOC set the dollar’s reference rate at CNY6.5921, in line with expectations. The dollar has been consolidating its losses against the yuan since the middle of November. Yesterday it reached a two-week high near CNY6.5945. The low today (~CNY6.5605) was the lowest since November 18.

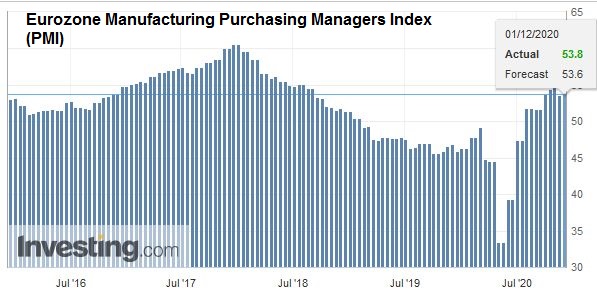

EuropeThe eurozone manufacturing PMI rose to 53.8 from the preliminary estimate of 53.6 but remained below October 54.8 reading. The new social restrictions appear responsible for the decline, but it is holding in better the earlier lock-down. |

Eurozone Manufacturing Purchasing Managers Index (PMI), November 2020(see more posts on Eurozone Manufacturing PMI, ) Source: investing.com - Click to enlarge |

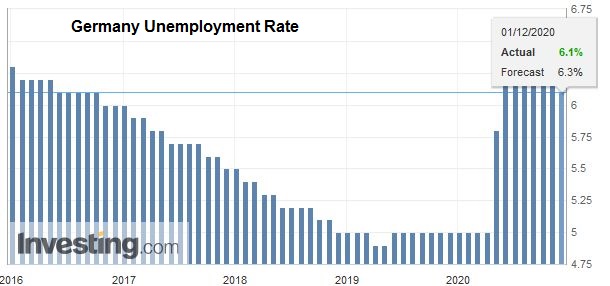

| Germany’s flash reading was revised slightly lower (57.8 vs. 57.9, and 58.2 in October. In contrast, France’s flash report was revised up (49.6 from 49.1, and 51.3 in October). |

Germany Unemployment Rate, November 2020(see more posts on Germany Unemployment Rate, ) Source: investing.com - Click to enlarge |

| Italy’s November report slipped to 51.5 from 53.8 in October, and Spain eased below the 50 boom/bust level to 49.8. Most saw employment soften, slower gains in output and new orders fell. |

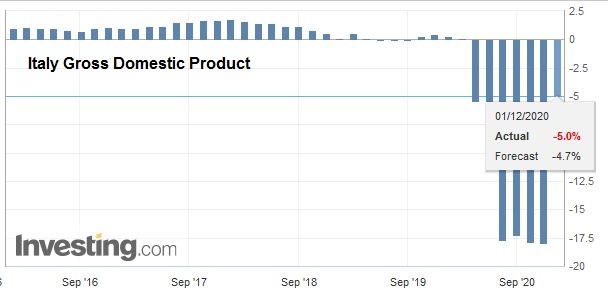

Italy Gross Domestic Product (GDP) YoY, Q3 2020(see more posts on Italy Gross Domestic Product, ) . |

| Separately, the preliminary November CPI was unchanged from October, showing a 0.3% year-over-year decline in the headline and a 0.2% gain at the core level. There is little doubt that the ECB will ease policy next week. An expansion and extension of its emergency bond-buying program and new low (negative) rate loans are its primary levers. |

Eurozone Consumer Price Index (CPI) YoY, November 2020(see more posts on Eurozone Consumer Price Index, ) Source: investing.com - Click to enlarge |

The UK’s manufacturing PMI was revised higher to 55.6 from the 55.2 preliminary estimate and 53.7 in October. This is a new cyclical and the highest in three years. It underscores the idea that the second-round restrictions have not hit the manufacturing sector as hard as the first. Parliament will vote today on the Prime Minister’s tiering system to replace the nationwide restrictions. Opposition Labour says it may abstain, allowing Tory rebels to embarrass the government.

The EC has been reluctant to present the emergency measures that will be enacted to minimize the chaos if a new trade agreement with the EU cannot be struck. The UK’s Foreign Secretary Rabb dismissed the recent EU compromise on fish as not serious. However, a combination of calendar considerations and the lack of progress is forcing its hand. Reuters reports that either Wednesday or Thursday, the EU will present its contingency plans. Nevertheless, sterling was largely unaffected. It retested the area that capped it last week (~$1.3385) but held above $1.33 during the greenback’s bounce. The euro pushed briefly above GBP0.9000 for the first time in a couple of weeks but fell back to the GBP0.8945 area. Recall that at the beginning of last week, the euro had retested the two-month low set earlier this month near GBP0.8860.

There was much hoopla earlier this year when the EU adopted the Recovery Fund (750 bln euros) that was going to be capitalized. But by trying to turn it into a lever to punish Hungary and Poland while needing their approval to raise debt in the capital markets, the EC overplayed its hand. Of course, despite the stalled efforts, peripheral European bond yields have tumbled to new lows, and premiums over Germany have narrowed considerably. It is the ECB purchases, and persuading other investors of no redenomination risk is the major driver. Although it does not capture the imaginations the way the “Hamiltonian moment” did, there was an important development yesterday that will help take the next step to complete the monetary union. Specifically, the work that went into striking an agreement that the European Stabilization Mechanism (IMF-like) would be introduced early as a backstop for the Single Resolution Fund will allow, even if it takes further debates, to launch an EMU-wide deposit insurance program.

The bearish price action on the euro yesterday saw it sell-off from a little above $1.20 to about $1.1925 seems to be exaggerated month-end related. It held the low today and recovered to around $1.1985 before sellers re-emerged in the European morning. Initial support is seen near $1.1950, which also houses an option for about 640 mln euros that expires today. There is also optionality at $1.19 (~510 mln euros) and $1.20 (~615 mln euros). Sterling traded briefly above $1.34 for the first time in three months today but immediately ran into a wall of sellers that pushed it back to about $1.3340 before finding support. The market has tried for the past week and a half to get above $1.34. A break now of the $1.33-area may suggest the market has given up and may retreat toward $1.3200. The euro tested GBP0.9000 before the weekend and again yesterday before slipping to GBP0.8945. It fell further to GBP0.8930 today before recovering. It looks poised to test the GBP0.9000 level again.

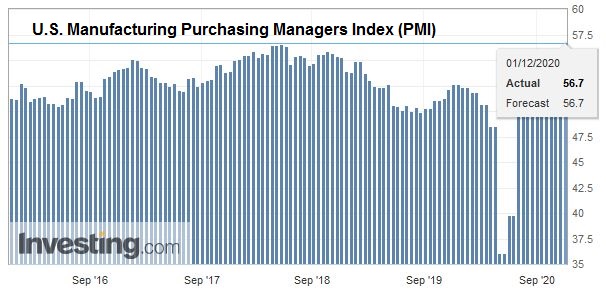

AmericaThe revision to Markit’s manufacturing PMI, where the preliminary reading of 56.7 was unexpectedly strong and a new cyclical high (it stood at 52.6 a year ago), may not draw the attention of the November ISM. The ISM is forecast to ease to 58.0 from 59.3, which would be the second-highest reading since November 2018. New orders will likely remain elevated (67.9 in October). The employment reading should be consistent with manufacturing adding jobs. Construction spending is expected to have accelerated after a 0.3% gain in September. Lastly, US November auto sales will be released over the course of the session. After recovering from May through September, auto sales slipped to 16.21 mln from 16.34 mln in September. They are expected to have softened to around 16.10 mln in November. Through October, the monthly average was 14.11 mln vehicles (seasonally adjusted annual rate) compared with an average in the first ten months last year of 16.92 mln. |

U.S. Manufacturing Purchasing Managers Index (PMI), November 2020(see more posts on U.S. Manufacturing PMI, ) . |

In his prepared remarks ahead of today’s testimony, Fed Chair Powell warned that the US economy was damaged and the outlook uncertain. Market participants will look for clues into what the FOMC may do at its meeting later this month. Most of the focus is on shifting buying to longer-dated maturities, while some still hold out the possibility of increasing its purchases. Treasury Secretary Mnuchin will testify alongside Powell and will likely be questioned on the decision not to renew several Fed lending facilities. The argument is that 1) that was Congress’ intent and 2) the funds could be better allocated to where they are needed and will be used.

Canada opened up its purse strings further yesterday as Finance Minister Freeland announced new spending of nearly C$52 bln over the next two years. The fact that its fiscal house was in order before the crisis gives the Trudeau government more room to maneuver. Moreover, the government appears not to be just supporting the economy during the crisis but has a vision for the aftermath that emphasizes childcare, pharmacare, and climate-friendly measures. IAlso, the need of the minority government for support from the New Democrat Party may have helped shape the package. Today Canada reports Q3 GDP. The Bloomberg survey’s median forecast calls for a nearly 48% jump at an annualized clip after a 38.7% contraction in Q2. Still, the economy lost some momentum as the quarter progressed, and the September monthly GDP may have slowed to 0.9% from August’s 1.2%. The Markit PMI, which stood at 55.5 in October, maybe overshadowed by the GDP report.

For its part, Mexico reports the weekly reserve figures (which have been steadily rising), worker remittances (which have been stronger than anticipated, running about 10% above year-ago levels), and the Markit PMI (43.6 in October). The manufacturing PMI bottomed in April at 35.0 and last November soot at 48.0.

The US dollar fell to a marginal new low for the year against the Canadian dollar yesterday, near CAD1.2925. It then recovered to trade above CAD1.30 and left what appeared to be a bullish hammer candlestick in its wake. However, there was no follow-through greenback buying, and an inside day is being recorded. After falling to almost CAD1.2940 in late Asian turnover, the greenback bounced to the CAD1.2980 area in early European activity, where sellers emerged. The greenback’s drop against the Mexican peso lost momentum last week around MXN19.95, and yesterday it rose to around MXN20.2165. It is consolidating within yesterday’s range but softer.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,Brexit,Canada,China,Currency Movement,EMU,Featured,newsletter,OPEC,RBA