Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

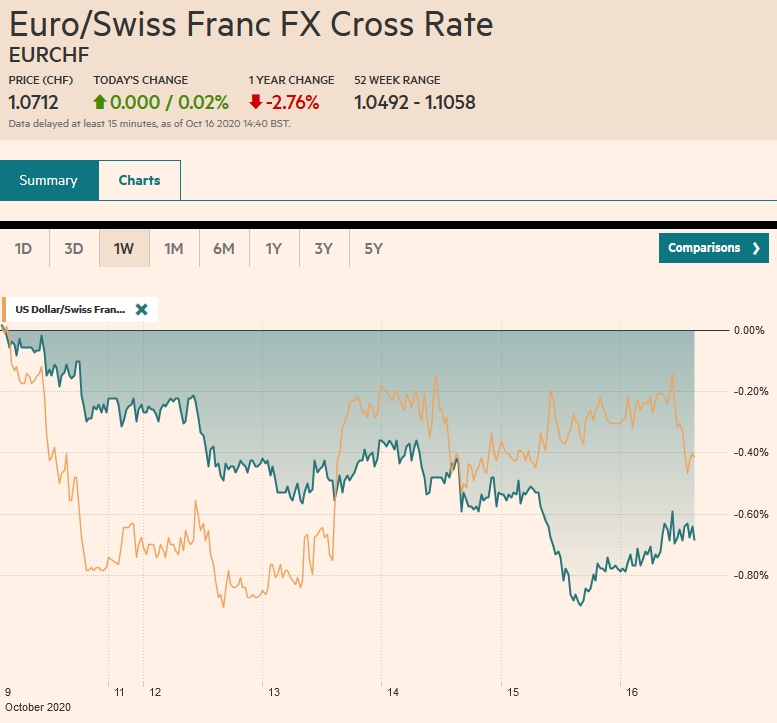

Swiss FrancThe Euro has risen by 0.02% to 1.0712 |

EUR/CHF and USD/CHF, October 16(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: It was like deja vu all over again. First, the market reacted immodestly to headlines indicating there was little chance of pre-election fiscal stimulus in the US. It was hardly new news. Then the market seemed to react with surprise that there was no last-minute breakthrough in the UK-EU trade negotiations. Prime Minister Johnson could abandon the talks, but his chief negotiator had already judged that a deal was still possible, and this seems to allow negotiations to continue. The firm close in US equities failed to carry over much to Asia Pacific trading earlier today. Only Hong Kong and Indian equities gained. In Europe, the Dow Jones Stoxx 600 is recouping around a third of yesterday’s 2% drop and is snapping the three-day slide. US shares are steady to a little higher. The US 10-year note yield is around 0.72%, slightly softer on the day and around four basis points lower on the week. European bond yields are a little softer. Peripheral yields are consolidating near record lows, while the German Bund yield, near minus 63 bp is off eight basis points this week to a new seven-month low. The dollar is mostly softer today, though the Australian dollar and Norwegian krone are exceptions. Emerging market currencies are mixed. The Korean won leads the decliners, paring this week’s gains, following an unexpected rise in unemployment (3.9% from 3.2%). The South African rand and Chinese yuan help the JP Morgan Emerging Market Currency Index snap a four-day decline. Gold is edging higher for the third day as it rebuilds a hold above $1900. November WTI is little changed on the day and week around $40.70 a barrel. |

FX Performance, October 16 - Click to enlarge |

Asia Pacific

Japan will tap the nearly JPY8 trillion reserve fund to renew its furlough program. It will draw down the fund by about JPY550 bln (~$5.2 bln), of which JPY440 bln is for the job support effort. The remainder will be used for domestic supply chain investments and funds to support agriculture and fisheries.

In other regional developments, we note that in addition to the unexpected jump in South Korea’s unemployment, Singapore’s reported a surprise 11.3% drop in non-oil exports in September after a 10.5% gain in August. As a regional hub, Singapore is often seen reflected regional trends. A bright spot in the disappointing trade figures was the shipment of electronic goods. These rose 21.4% year-over-year, surging from the 5.7% rise in August. The state of emergency in Thailand weighed on local equities, which fell 3.5% this past week. Foreign investors have sold $9 bln of Thai stocks this year before the week and about $1.4 bln of Thai bonds.

Last weekend, the PBOC reduced to zero the reserve requirement on banks for currency forwards. Recalling this policy tool’s past use, many said that China was capping the yuan’s gains. We saw it as a milder move and one consistent with the encouragement of foreign portfolio capital inflows and the use of the onshore yuan for hedging instead of the offshore yuan. Although many are focused on goods trade and see why the PBOC would lean against yuan strength, we have focused on the integration of China into the global capital markets and see how a yuan that better reflects the investment drivers (possibly the only G20 economy that will grow this year and relatively high yields, and a market that has become more accessible for foreign investors). Separately, but related, note that China reports Q3 GDP at the start of next week. The Bloomberg survey found a median forecast of 3.3% quarter-over-quarter growth after an 11.5% expansion in Q2. The IMF sees the world’s largest economy expanding 1.1% year-over-year here in 2020 and 8.2% next year.

The dollar is in a JPY105.00-JPY105.50 range in recent days. The dollar has alternated between gains and losses this week. It finished last week near JPY105.60. Indications that the Reserve Bank of Australia is considering new measures, including buying longer-dated bonds, weighed on the Aussie this week. It slid around 2.25% this week, giving back the bulk of the gains registered in the previous two weeks. The inability to recover the $0.7100-handle today warns of the risk of a test on the two-month low set in late-September near $0.7000. The PBOC set the dollar’s reference rate at CNY6.7332, which was in line with expectations. China’s 10-year bond yield edged higher to nearly 3.24%, the highest this year, a five-basis point increase this week.

EuropeThere are two focus points in Europe: the second-coronavirus wave, that by some measures is eclipsing the US, and the UK-EU trade talks. The tragic resurgence of the virus is likely to resolve the apparent debate at the ECB. No one was really expected a move when it meets later this month, but the downside risks are materializing that ECB President Lagarde will recognize this, and it will help set the stage for a move in December, armed with new staff forecasts. This is spurring a swing in market sentiment. When the Fed adopted the average inflation target, many thought this was an aggressive move than the ECB could not match. On the contrary, the ECB is seen acting before the Fed, and the net result has been a widening of interest rate differential (the US vs. Germany), which could be a factor that has weighed on the euro’s exchange rate. |

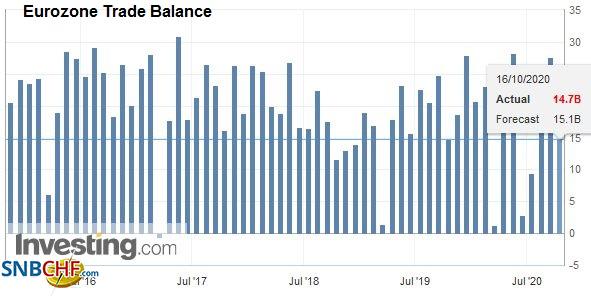

Eurozone Trade Balance, August 2020(see more posts on Eurozone Trade Balance, ) Source: investing.com - Click to enlarge |

| The EU wants the UK to compromise on state aid before it compromises on fishing. The UK’s Johnson and chief negotiator Frost, in effect, have renewed their threat to leave the talks. A decision is expected over the weekend, but this seems like theater aimed at a domestic constituency. Talks are scheduled for next week. |

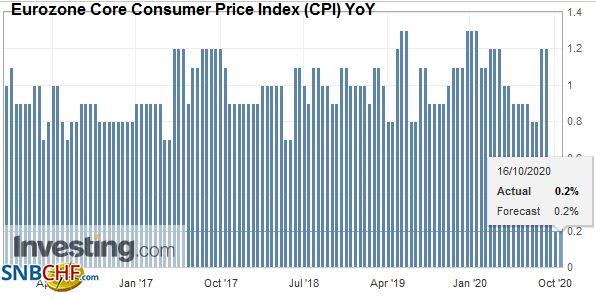

Eurozone Consumer Price Index (CPI) YoY, September 2020(see more posts on Eurozone Consumer Price Index, ) . |

| Meanwhile, it is only prudent that both sides step up preparation for no agreement. Size does matter and the EU’s economy is six times larger than the UK economy. This gives it leverage. German Chancellor Merkel, the consummate strategist, sees room for a compromise, but the extent of her influence now, as she begins her last year in office, is now an open question. |

Eurozone Core Consumer Price Index (CPI) YoY, September 2020(see more posts on Eurozone Core Consumer Price Index, ) - Click to enlarge |

The euro is in about a quarter of a cent range through the European morning below $1.1720. The inability to distance itself from the $1.1700 level warns of further downside risks. The is little doubt that the expiring option for 680 mln euros at $1.1700 has been neutralized. The next set of expiring options are half a cent away from that one. Recall that the euro finished last month near $1.1715. Sterling held above the week’s low set on Wednesday a little below $1.2865. Today may be the first session since October 8 that sterling does not trade above $1.30. There are about GBP450 mln in options set at $1.2945-$1.2950 that expire today and have also likely been offset.

America

The main obstacle to US fiscal stimulus may indeed be the proximity of the election, but not in the way the partisans have suggested. While the moving target of the White House position might find common ground with the Democratic-led House of Representatives, the problem is that the White House cannot deliver the Senate. Senate leader McConnell reiterated that the Senate’s support is for a package a third of the size of the $1.8 trillion that the White House as endorsed. With the President lagging in the polls nationally and in several swing states, Trump no longer has the clout to swing the Senate around. Note that the Pandemic Emergency Unemployment Compensation (13-week extension) that is rising as people exhaust their benefits under the normal program expires in December.

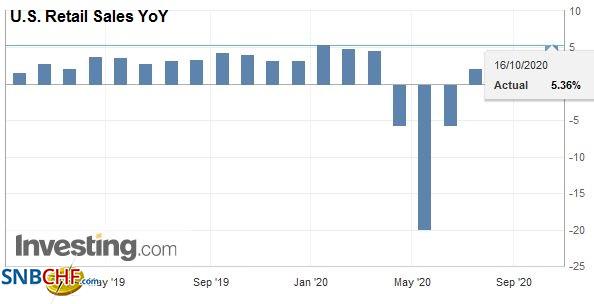

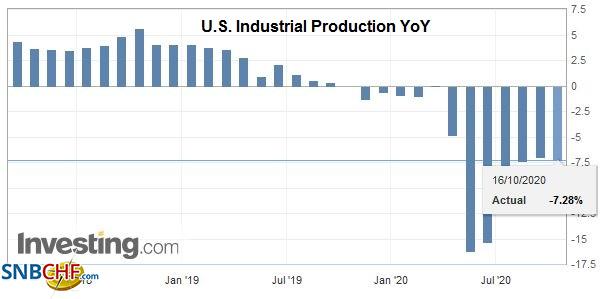

| The US reports September retail sales and industrial output figures today. Retail sales were disappointed in August, and the core measures that exclude autos, gasoline, and building materials were contracted in August. The headline is expected to rise by 0.8% and the core by 0.3%. The pace of headline sales slowed in June, July, and August. Industrial production is expected to edge 0.5% higher after a 0.4% gain in August. |

U.S. Retail Sales YoY, September 2020(see more posts on U.S. Retail Sales, ) Source: investing.com - Click to enlarge |

| The manufacturing sector is the driver. It rose 1% in August and is expected to have risen by 0.6% in September. It would be the third successive slower month, but still a solid number. Consider that last September and October, manufacturing output fell by 0.6% each month. The University of Michigan releases its preliminary consumer confidence an inflation expectation for October, and at the end of the day, the TIC data (August) will be reported. |

U.S. Industrial Production YoY, September 2020(see more posts on U.S. Industrial Production, ) Source: investing.com - Click to enlarge |

The US dollar reached almost CAD1.3260 yesterday, having begun the week near CAD1.3130. It is consolidating between CAD1.3200 and CAD1.3240 so far today. The $670 mln option at CAD1.3220 that expires today has most likely been hedged. The 20-day moving average is near CAD1.3270. A break of CAD1.3200 could spur a move back toward CAD1.3160 but may need a firmer tone to equities. The S&P 500 began the week with a third consecutive gap higher opening. As we noted, a three successive gap higher openings are a sign of an over-extended market. Wednesday’s decline closed Monday’s gap and yesterday’s loss closed last Friday’s gap. Yesterday’s strong close was nice, but follow-through buying is needed to secure the gains. The greenback is little changed against the Mexican peso. The dollar rose in the first two sessions this week but has softened since. It fell by nearly 5.5% over the past two weeks, and near MXN21.26, it is up about 0.6% this week. Initial resistance is seen near MXN21.35, and support is closer to MXN21.15.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,$CNY,Brexit,Currency Movement,ECB,Featured,newsletter,Politics