Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

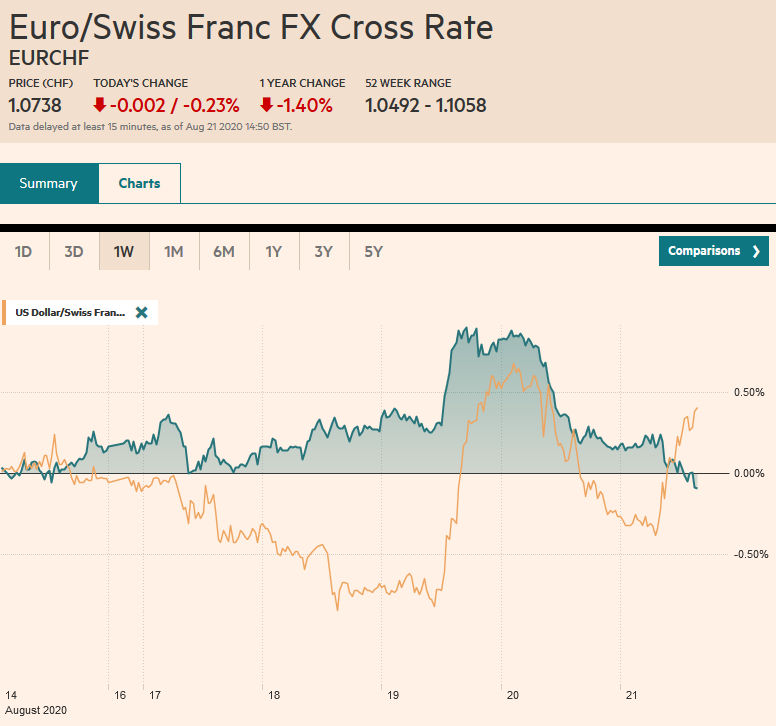

Swiss FrancThe Euro has fallen by 0.23% to 1.0738 |

EUR/CHF and USD/CHF, August 21(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The second disappointing Fed manufacturing survey report and an unexpected rise in weekly jobless claims helped reverse the disappointment over the FOMC minutes. Bonds and stocks rallied–not on good macroeconomic news, but the opposite, which underscores the likelihood of more support for longer. News that Pfizer’s vaccine may be ready for regulator review in a couple of months also lifted spirits. However, disappointing eurozone preliminary PMI sapped the enthusiasm. Asia Pacific equities moved higher, led by 1% gains in Hong Kong, Taiwan, and South Korea. Australia was a notable exception and slipped fractionally. On the week, only Chinese and Indian benchmarks rose. European bourses are posting small gains, which pares the week’s loss to little more than 0.3%. US shares are flat, and the S&P 500 is up about 0.4% for the week coming into today. Bond yields are softer on the day and week. The US 10-year yield was near 70 bp at the end of last week and is now below 65 bp. Core European yields are off 5-6 basis points on the week as well. The dollar is firmer against all the majors but the Japanese yen. Continental European currencies are off around 0.3%-0.5%. Emerging market currencies are mostly lower, but what appears to be a short-covering bounce, perhaps helped by reports of a large energy find in the Black Sea, is lifting the beleaguered Turkish lira. Gold was turned back from $1955 and is holding a little above the low for the week (~$1930). October crude oil is holding in a 50-cent range below $43.00. |

FX Performance, August 21 - Click to enlarge |

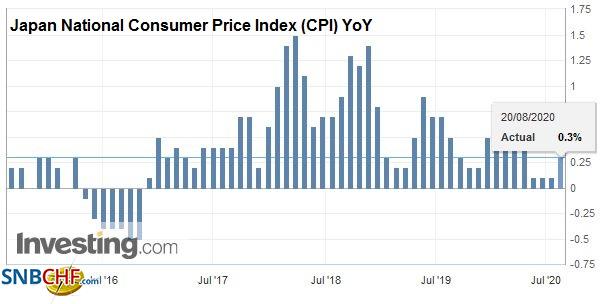

Asia PacificJapan reported disappointing price pressures (August CPI) and a mixed PMI. Headline CPI rose by the expected 0.3%, but underlying measures were unchanged while economists had forecast a small increase. Core inflation, which excludes fresh food, was flat year-over-year, and when fresh food and energy are excluded, prices rose by 0.4%. |

Japan National Consumer Price Index (CPI) YoY, July 2020(see more posts on Japan National Consumer Price Index, ) Source: investing.com - Click to enlarge |

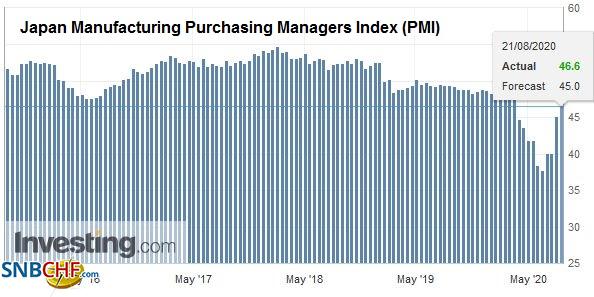

| Higher fresh food prices were partly a function of the weather and an unusual amount of rain. Looking ahead, deflationary forces may re-emerge when last year’s October sales tax hike is dropped from the year-over-year comparison. Separately, the PMI showed a slowing contraction in manufacturing (46.6 vs. 45.2) but some retrenchment in services (45.0 vs. 45.4). The composite was unchanged at 44.9. |

Japan Manufacturing Purchasing Managers Index (PMI), August 2020(see more posts on Japan Manufacturing PMI, ) Source: investing.com - Click to enlarge |

Australia’s preliminary July retail sales report showed improvement except in Victoria, but the August preliminary PMI showed greater weakness. Manufacturing slipped to 53.9 from 54.0, but the service PMI tumbled to 48.1 from 58.2. This knocked the composite to 48.8 from 57.8.

South Korea reported trade for the first 20-days of the month. Exports were off 7% year-over-year, improving from a 12.8% decline last month. Imports did not recover as much and were off 12.8% after a 13.7% decline previously.

The dollar is heavy but in a narrow range against the Japanese yen. It has been capped near JPY105.80 and found a bid in early Europe near JPY105.45. The greenback is off around 1% against the yen this week, snapping a two-week advance. A push above JPY105.80 runs into resistance around JPY106, where a nearly $750 mln option expires today. Similarly, the Australian dollar pullback back to $0.7170 where it too has found a better bid in the European morning. Resistance is seen near $0.7220. It finished last week near $0.7170, and a close above there today would extend the streak to the ninth consecutive week. The dollar traded at CNY6.90 today for the first time since late January, culminating a four-week slide. The PBOC set the dollar’s reference rate a little weaker than models projected at CNY6.9107.

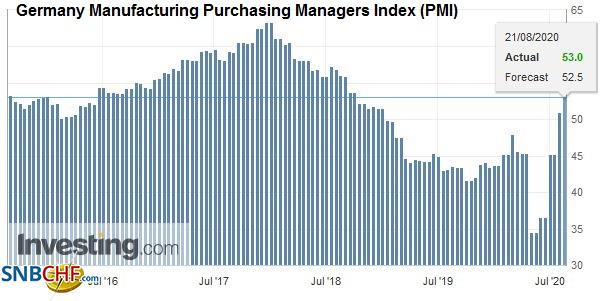

EuropeThe preliminary eurozone PMI disappointed. Germany reported a modest uptick in the manufacturing PMI (53.0 vs. 51.0), but this was more than offset by a weakness in the service PMI (50.8 vs. 55.6). |

Germany Manufacturing Purchasing Managers Index (PMI), August 2020(see more posts on Germany Manufacturing PMI, ) Source: investing.com - Click to enlarge |

| This produced a pullback in the composite to 53.7 from 55.3. France’s was even more disappointing as the manufacturing PMI fell back below the 50 boom/bust level. It stands at 49.0 after 52.4 in July. |

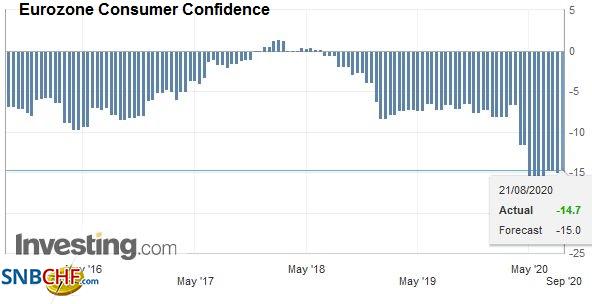

Eurozone Consumer Confidence, August 2020(see more posts on Eurozone Consumer Confidence, ) Source: investing.com - Click to enlarge |

| The service sector stalled, and the PMI fell to 51.9 from 57.3. Its composite is now at 51.7, down from 57.3.

Markit warned that output outside of Germany and France fell. |

Eurozone Markit Composite Purchasing Managers Index (PMI), August 2020(see more posts on Eurozone Markit Composite PMI, ) Source: investing.com - Click to enlarge |

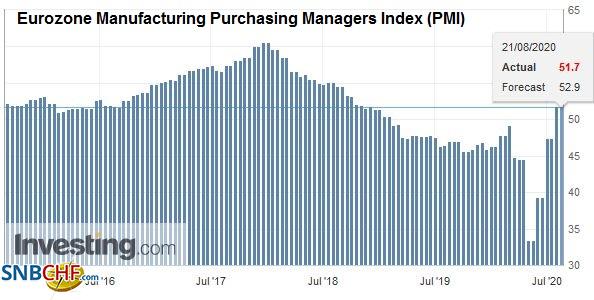

| The aggregate manufacturing PMI slipped to 51.7 from 51.8. |

Eurozone Manufacturing Purchasing Managers Index (PMI), August 2020(see more posts on Eurozone Manufacturing PMI, ) Source: investing.com - Click to enlarge |

| The service PMI fell to 50.1 from 54.7. The composite fell for the first time since April (51.6 vs. 54.9). |

Eurozone Services Purchasing Managers Index (PMI), August 2020(see more posts on Eurozone Services PMI, ) Source: investing.com - Click to enlarge |

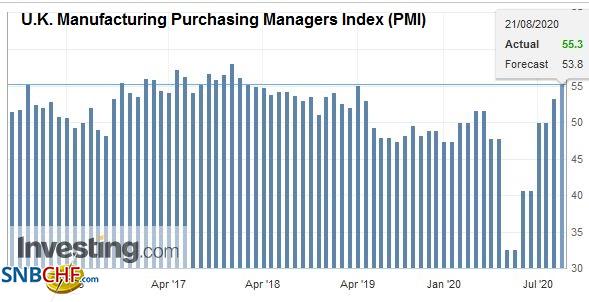

| The UK offered a pleasant upside surprise in both the July retail sales and the preliminary August PMI. Excluding gasoline, UK retail sales rose 2% in July. The median forecast in the Bloomberg survey was for a 0.2% increase after a 13.5% rise in June. Separately, it reported that the preliminary manufacturing PMI rose to 55.3 from 53.3, and the service PMI rose to 60.1 from 56.5. The composite increased to 60.3 from 57.0. Lastly, we note that the UK-EU trade negotiations ended this week with little progress. |

U.K. Manufacturing Purchasing Managers Index (PMI), August 2020(see more posts on U.K. Manufacturing PMI, ) Source: investing.com - Click to enlarge |

| The euro has traded on both sides of yesterday’s trading range, and a close below $1.1800 would warn of a test on the lower end of this month’s trading range (~$1.17) next week. The 20-day moving average is near $1.1810 today, and the euro has not closed below it since July 3. However, the North American market has been leading the dollar sales, and the intraday technicals warn the euro could recover toward the $1.1840-$1.1850 area. Sterling’s push toward $1.3250 has been repelled again, reinforcing the prevailing range, the lower end of which is seen near $1.30. Initial support may be found around $1.3150. |

U.K. Services Purchasing Managers Index (PMI), August 2020(see more posts on U.K. Services PMI, ) Source: investing.com - Click to enlarge |

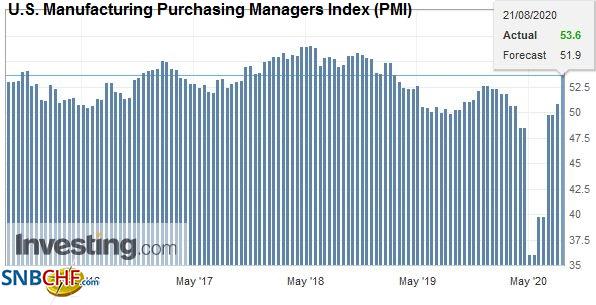

AmericaThe weakness in the Empire and Philadelphia Fed surveys, coupled with the unexpected rise in weekly jobless claims, lends more credibility to some high-frequency economic data that warned that the US economy has lost some momentum seen in late Q2 and early Q3. The data, coupled with the continued absence of new fiscal initiatives, make the July FOMC minutes seem particularly dated. Today’s economic reports include July’s existing-home sales (housing, goosed by low-interest rates, is a bright spot in the world’s largest economy). Economists expect small increases in the PMI, but after the Fed surveys, confidence may be shaken. Separately, reports suggest that in addition to new agriculture orders, China has boosted its energy purchases. An estimated 19 tankers carrying some 37 mln barrels of oil are expected to reach China next month. |

U.S. Manufacturing Purchasing Managers Index (PMI), August 2020(see more posts on U.S. Manufacturing PMI, ) Source: investing.com - Click to enlarge |

Canada has unveiled plans to extend emergency income support for another four weeks before transitioning some new programs (~C$37 bln) that will last the next year. New Finance Minister Freeland unveiled the initiative yesterday. Of the 4.5 mln people on assistance now, 3 mln will likely be included in a new employment insurance program, which appears to also include incentives for actively engaging in seeking employment. The other 1.5 mln will be shifted to new programs. Canada is wrestling with what other countries will, too, and that is how to extend income support for longer.

Canada also reports June retail sales today. They are expected to have been spectacular. The median forecast in the Bloomberg survey is for a 24.5% increase after the 18.7% jump in May (excluding autos, an increase of closer to 15% is expected). Mexico also reports June retail sales. Economists expect an 8.5% increase after a 0.8% rise in May.

The US dollar is straddling the CAD1.3200 area. The low since January was recorded at mid-week near CAD1.3135. It reached almost CAD1.3250 yesterday before coming back off. The greenback found bids today around CAD1.3160. It closed a big figure higher last week (~CAD1.3260). Without reversing higher today, the US dollar will extend its losing streak for a sixth consecutive week against the Canadian dollar. The US dollar remains in a narrow range against the Mexican peso and has mostly been confined to MXN21.95-MXN22.15 this week. Lastly, the Brazilian real recovered last yesterday after selling off in response to the Senate overturning a presidential veto to cap civil servant pay. The issue has not been resolved, but the House reaffirmed the cap.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,Canada,Currency Movement,EMU,Featured,Japan,Korea,newsletter,U.K.