Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

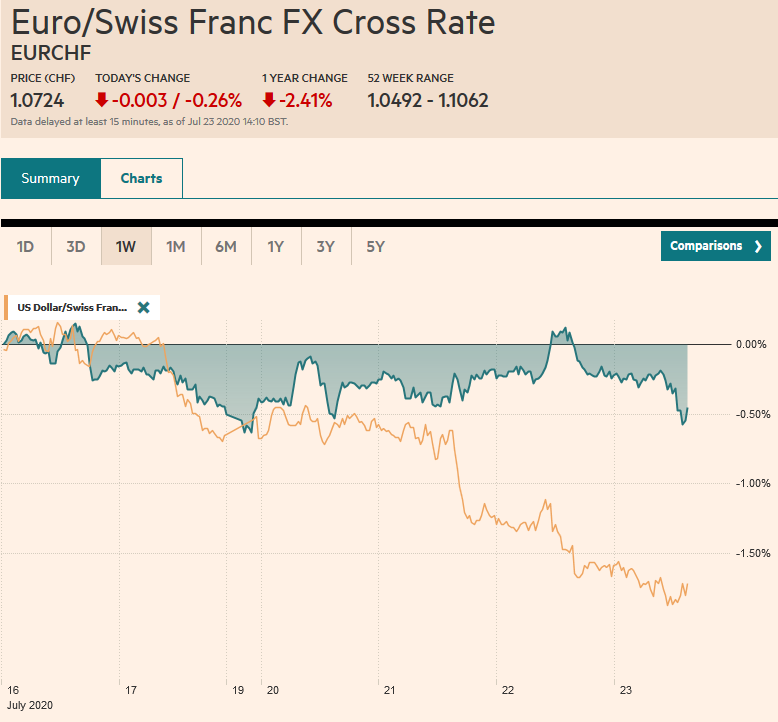

Swiss FrancThe Euro has fallen by 0.26% to 1.0724 |

EUR/CHF and USD/CHF, July 23(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The powerful momentum moves in the capital markets continues unabated by escalating US-China tensions and continued spread of the virus. Asia Pacific equities were mixed. Tokyo was closed for a holiday, but several other large markets in the region, like China, South Korea, and Taiwan markets slipped lower, while Hong Kong, Australia, and India advanced. Helped by autos and food and beverages, Europe’s Dow Jones Stoxx 600 is recouping around half of yesterday’s losses. US shares are trading with a firmer bias, and the S&P 500 looks to extend its advance for a fifth consecutive session today. Bond markets are quiet with the US 10-year holding below 60 bp, and Italian yields slipping despite the government approved another 25 bln euro spending measures. The Italian 10-year yield is poised to move below 1% for the first time in nearly five months. The dollar is mostly softer, though sterling and the Norwegian krone are not participating. The Dollar Index is falling for the fifth consecutive session and 10 of the past 11, illustrating the recent push lower. Many emerging market currencies are also participating in the movement against the greenback. The JP Morgan Emerging Market Currency Index is off for the fourth consecutive session. The market is expecting Turkey to leave rates steady today, and the odds seem to favor another rate cut by South Africa today. Gold is pushing to a new high near $1890. It would be the eighth advance in the past nine sessions. Oil is firm with the September WTI contract above $42 a barrel. The next big target is near the 200-day moving average around $44.40. |

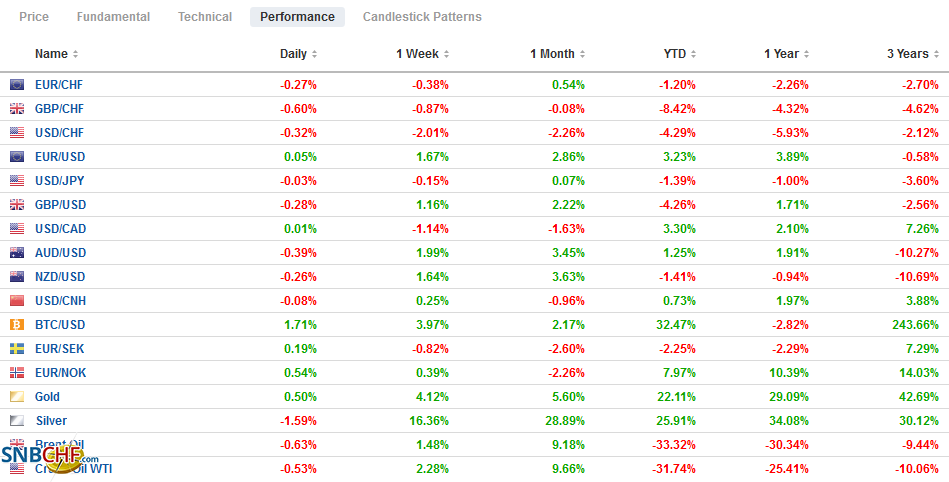

FX Performance, July 23 - Click to enlarge |

Asia Pacific

The shuttering of the Chinese consulate in Houston for the persistent theft of US technology, according to reports, represents a new escalation of the growing tension. It is not immediately clear which consulate office China will order to be shut in retaliation. Initial talk was of the Wuhuan office, but the focus has shifted toward the consulate office in Chengdu. This tit-for-tat has little serious substantive impact. China, for example, reportedly, is moving ahead with increasing its orders for US agriculture. Separately, the UK-China relationship is souring. US sanctions against Huawei appears to have helped force the UK’s hand in dropping the Chinese 5G champion, and the UK has suspended its extradition treaty with Hong Kong. China dropped coverage of a Premier League game from the UK, as it has US basketball games previously.

Australia is forecasting a record A$184.5 bln deficit in the fiscal year that began this month. That compared with an almost A$86 bln shortfall in the fiscal year that ended June 30. Still, even with that projection, the country’s debt to GDP ratio remains relatively low, just below 36% of GDP. The Treasurer’s report projects the economy will contract by 2.5% in the fiscal year, and inflation will be around 1.25%. Of note, the budget assumes that Australia’s largest export, iron ore, will fall to $55 a ton from around above $100 currently.

The South Korean economy contracted by 3.3% in Q2. The market had expected a decline in output of closer to 2.5% after a 1.3% contraction in Q1. Net exports were the largest drag. Exports plunged 16.6% in Q2 (-1.4% in Q1). Imports slumped by 7.4% (-3.6% in Q1). Helped by government support, consumption rose 1.4% after dropping by 6.5% in Q1. Government spending rose 1% in the quarter, a little slower than the 1.4% increase in Q1. Exports in the first 20 days of July were still depressed, but the worst appears behind it. The economy is expected to return to growth in the current quarter, and a third extra budget was passed earlier this month that will also support growth.

With Japanese markets closed, the dollar has been confined to an extremely narrow range against the yen so far today. Bloomberg has a range of JPY107.07 to JPY107.20. Nearby resistance in North America is seen in the JPY107.30-JPY107.50 area. The Australian dollar is holding below yesterday’s high that was a little above $0.7180. The market seems to be hesitating as it nears the $0.7200-level. Initial support is seen in around $0.7100-$0.7120. The PBOC set the dollar’s reference rate at CNY6.9921, which was stronger than the models suggest and about 0.3% above where it closed yesterday, which is a relatively large more for China. Many see it as a not-too-subtle protest to the US decision to close China’s Houston consulate.

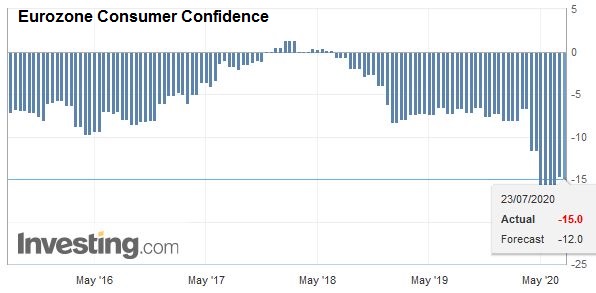

EuropeNews from Europe is light. Participants are looking forward to tomorrow’s preliminary July PMI. The composite is expected above 51.0 from 48.5 in June. It would be the highest since February after it finished 2019 at 50.9. A reading above 50 implies expansion. Such a report would underscore the idea that Europe is enjoying a stronger recovery than the US. It is doing a better job of limiting the new flare-ups of the virus as the economies open. The US, Brazil, and India account for more than half the cases and around 40% of the fatalities. |

Eurozone Consumer Confidence, July 2020(see more posts on Eurozone Consumer Confidence, ) Source: investing.com - Click to enlarge |

Italy is pushing ahead with its plans for more fiscal support. The government approved a 25 bln euro spending bill to help support those that have lost their jobs and to subsidies local and regional governments. The ECB and EU support is helping to prevent a backing up of yields. Italy’s 10-year benchmark yield has fallen by 25 bp over the past month to flirt with the 1% level for the first time since February. The generic two-year yield is at minus 20 bp, the lowest in almost five months.

The euro reached $1.16 yesterday and has barely backed off. That area corresponds to a 50% retracement of the drop from early 2018 high around $1.2550. A convincing break would target the $1.1800-$1.1820 area. The single currency has fallen in only one session since July 9. initial support is seen around $1.1550, where an option for about 825 mln euros will expire today. Sterling reached a high on Tuesday near $1.2770 and has been consolidating since then. It reached a low just below $1.2650 yesterday. These two areas mark the near-term range and note that the 200-day moving average is a little above $1.27. The intraday technicals favor another test on the upside in North America today.

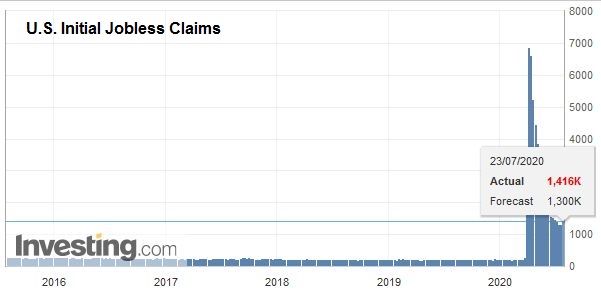

AmericaThe Senate Republicans and the White House are moving closer to an agreement that will allow negotiations with the House Democrats to begin. That said, it is still not clear about what will happen to the unemployment benefits. The $600 a week federal insurance is set to expire at the end of the month. A short-term measure is possible to bridge the time, but it does not look particularly likely. Separately, the US reports weekly jobless claims, and there is some risk that they may have shown an increase from the 1.3 mln from the previous week. It would be the first increase since the end of March. It could reflect a seasonal adjustment quirk, but the time series has been sticky has generally been above economists forecasts. The US Treasury also auctions $14 bln of 10-year inflation-protected securities. There has been some interest in inflation-protected funds, and the demand is expected to be strong. |

U.S. Initial Jobless Claims, July 23 2020(see more posts on U.S. Initial Jobless Claims, ) Source: investing.com - Click to enlarge |

Some progress has been reported in Mexico’s efforts at pension reform. The government’s draft proposals call for greater private sector contributions. Previously, there had been talk that AMLO wanted to increase state control. However, the bill, which is now before the lower house of congress, requires employers to triple to 13.87% (of salaries) over the next eight years the amount it pays toward pensions. The bill also reduced the length of time one must work to qualify for the pension from 1250 weeks to 750. Meanwhile, Brazil’s government has offered a small tax reform bill that essentially unifies two taxes (PIS and Cofins) to create a single value-added tax. While the bill seems milder than the efforts in Congress, Finance Minister Guedes is delivering his long-awaited tax reform in piecemeal.

Higher than expected June CPI readings from Canada yesterday helped push the US dollar to CAD1.3400 yesterday, and follow-through selling today has seen the greenback fall to almost CAD1.3370. The post-crash low was set on June 10 near CAD1.3315, and that is the next important chart point. Today would be the fourth consecutive decline in the US dollar and matches the longest depreciating streak of the year. The CAD1.3400 area may now offer resistance. The greenback is offered against the Mexican peso, but it is within yesterday’s ranges. The dollar dripped below MXN22.19 yesterday to record a two-week low. The intraday technical indicators suggest the dollar’s decline can be extended today.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,$CNY,Brazil,Currency Movement,Featured,Italy,Mexico,newsletter,South Korea