Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

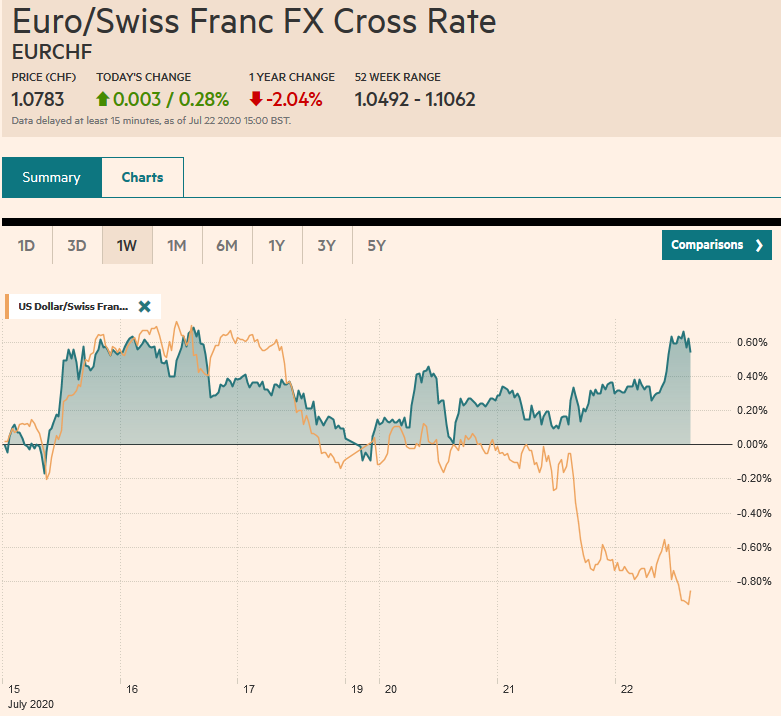

Swiss FrancThe Euro has risen by 0.28% to 1.0783 |

EUR/CHF and USD/CHF, July 22(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The optimism among investors appears to have evaporated in the face of new US-Chinese tensions, possible delays in the next US fiscal stimulus, and new record virus infections in Australia and Hong Kong. US stocks had pared early gains yesterday, and the high-flying NASDAQ finished lower after setting new record highs. Hong Kong (-2.25%) and Australia (-1.3%) led the regional declines, though China eked out some modest gains, helped by the energy sector. The MSCI Asia Pacific and Europe’s Dow Jones Stoxx 600 are snapping three-day advances today, and US shares are pointing to a lower open. Bond markets are narrowly mixed, and the peripheral European bonds have lost bid seen earlier this week on the EU agreement. The US 10-year has slipped below 60 bp. The dollar is mixed. The euro has is at new 14-month highs, near $1.1570. The Australian dollar is just below 15-month highs near $0.7170. Sterling and Norwegian krone are leading the decliners with 0.4% and 0.2% declines near midday in Europe. Emerging markets currencies are also seeing profit-taking after the JP Morgan Emerging Market Currency Index rose 1.1% yesterday, the most in a month. Gold reached almost $1866 before profit-taking saw it fall $20 before buying re-emerged. Oil is also pulling back after reaching a four-month high near $42.50 yesterday basis the September WTI contract. It is trading about a dollar below yesterday’s highs. |

FX Performance, July 22 - Click to enlarge |

Asia PacificThe US has apparently ordered China to close its consulate in Houston within a few days. It is not immediately clear why, though some are linking it to surveillance or attempts to steal or disrupt US efforts to find a vaccine. There are reports that officials in the consulate were destroying documents. Chinese officials threaten a tit-for-tat response. The yuan did appear to weaken on the news, though most currencies, as we noted, are softer today against the greenback. Preliminary July PMI readings will mostly be reported Friday, but Japan’s was released today and confirms that the world’s third-largest economy continues to struggle at the start of Q3. The manufacturing PMI edged up to 42.6 from 40.1 and the services to 45.2 from 45.0. The composite stands at 43.9, up from 40.8 in June. Recall that it finished last year at 48.6. The BOJ does not meet again until the middle of September, and there continues to be talk of another supplementary budget in the second half of the fiscal year that begins October 1. |

Japan Manufacturing Purchasing Managers Index (PMI), July 2020(see more posts on Japan Manufacturing PMI, ) Source: investing.com - Click to enlarge |

The dollar found support near its recent lows against the yen around JPY106.65 yesterday, and Tokyo refrained from selling it. It edged back above JPY107 in the European morning, but we suspect the JPY107.20 area may cap it and what appears to be a risk-off day. The Australian dollar’s 1.6% advance yesterday was the largest in nearly seven weeks. Limited follow-through buying saw it rise to almost $0.7170 today before the profit-taking was seen. It is finding support about half a cent lower. The PBOC set the dollar’s reference rate at CNY6.9718 compared with a median model estimate of CNY6.9712. The dollar rose back above CNY7.0, and its 0.4% advance is the largest in a couple of months.

Europe

The UK Telegraph reports that post-Brexit trade negotiations with the EU are on the verge of breaking down. Businesses are apparently being instructed to prepare to have future trade on WTO terms. UK Prime Minister Johnson had previously threatened to walk away from the talks if there was no substantial progress by the end of this month, and the two sides are still far apart, according to reports. Given the disruption that is bound to happen regardless of the talks, game theory would suggest negotiating until the last minute to demonstrate everything was done to minimize it. The virus slowed the negotiations in the first place, and to stop now seems more like a threat.

The EU agreement has not been approved by the EU Parliament, but there are already some different interpretations. The EC is claiming a link between access to the new funding and adherence to the rule of law. Both Hungary and Poland are subject to EU probes and reportedly given some assurances to secure their support for the historic Recovery Plan and EU budget. Separately, Greece and Turkey’s simmering conflict is escalating as Turkey explores contested water on the continental shelf.

The euro is the second largest reserve currency behind the dollar. Leaving aside theoretical debates about monetary union without fiscal union, many, if not most observers, see a chief obstacle to a greater reserve role is the lack of a common bond and bill market. A new EU bond is clearly a welcome step in this context. However, the size is relatively modest, and it could be a one-off, emergency-spurred offering. A common bill market is also not in the cards. This is why we are reluctant to fully embrace the EU’s new budget and Recovery Plan as a major game-changer for the euro’s reserve role.

The euro made marginal news highs, a little shy of the $1.1550 level before profit-taking set in and knocked the single currency to almost $1.1500 in early European trade when new buying emerged. It could be linked to the 1.1 bln euro option at $1.15 that expires today and another one at the same strike for 1.2 bln euros tomorrow. Recall that the 2019 high for the euro was near $1.1570. Sterling reached almost $1.2770 yesterday and is trading a cent below it near midday in Europe and is back below the 200-day moving average (~$1.2700). It found support a little below $1.2650, and the intraday technicals warn that the option at $1.2725 for roughly GBP460 mln that expires today may still be in play.

America

Negotiations between the Republicans in the Senate and the White House appear to be stuck, and this may delay the next fiscal package into next month. After the Republicans reach an agreement, then talks will be held with the House, where the Democrat-majority passed a bill for over $3 trillion that will be the basis of its position. Meanwhile, the risk is that some programs, like the $600 a week federal unemployment insurance payment, expire.

The other controversy is over Federal Reserve nominee Shelton, who, on a partisan vote, was approved by the Senate Banking Committee yesterday. Critics do not like her gold views or that she apparently changed her views on other issues to become a more attractive nominee for President Trump. However, the most important issue here is not the content of her views but the legitimate process that has been pursued. Some observers urging the media and others to treat her differently if she is confirmed by the entire Senate, which is still an open question. Six Republican dissenters could defeat the nomination. Trump has appointed the majority of Fed governors, and the resilience of the institution tends to be under-appreciated by many of those who claim that Shelton will be a disruptive force.

Canada’s May retail sales showed a strong recovery from April’s revised 25% drop (initially -26.4). However, at 18.7%, it was not quite a strong as economists hoped. Auto sales drove the gain, but even excluding them, retail sales rose 10.6%, as 10 of the 11 sectors improved, and the Statscan pointed to substantial gains last month as well. Canada reports June CPI figures today. The collapse in oil prices had driven the headline below zero, and it likely emerged from there for the first time since March. Its three core measures have been more stable, but in any event, officials are more concerned about the economic slack. The 10-year breakeven (the yield difference between conventional and inflation-linked bonds) set a new four-month high yesterday of a little more than 88 bp. Before the pandemic, it was closer to 140 bp.

The US reports June existing home sales. A strong gain is expected after the nearly 10% decline posted in May. Housing and manufacturing appear to be leading the US recovery. EIA oil inventory estimate will be watched as well following the API estimate of a 7.5 mln barrel build. Mexico reports May retail sales. A modest bounce (~3.5%) is expected after the 22.4% plunge in April.

The US dollar was sold to around CAD1.3425 yesterday, its lowest level since June 11. It is consolidating in a narrow range just above there so far today. Previous support in the CAD1.3480-CAD1.3500 area should now offer resistance. Like the Canadian dollar, the Mexican peso is little changed through the Asian session and the European morning. The greenback is trading at the lower end of the recent range seen near MXN22.25. Below there support is seen near MXN22.15. The MXN22.50 may offer initial resistance.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,Brexit,Canada,China,Currency Movement,EU,Featured,newsletter