Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

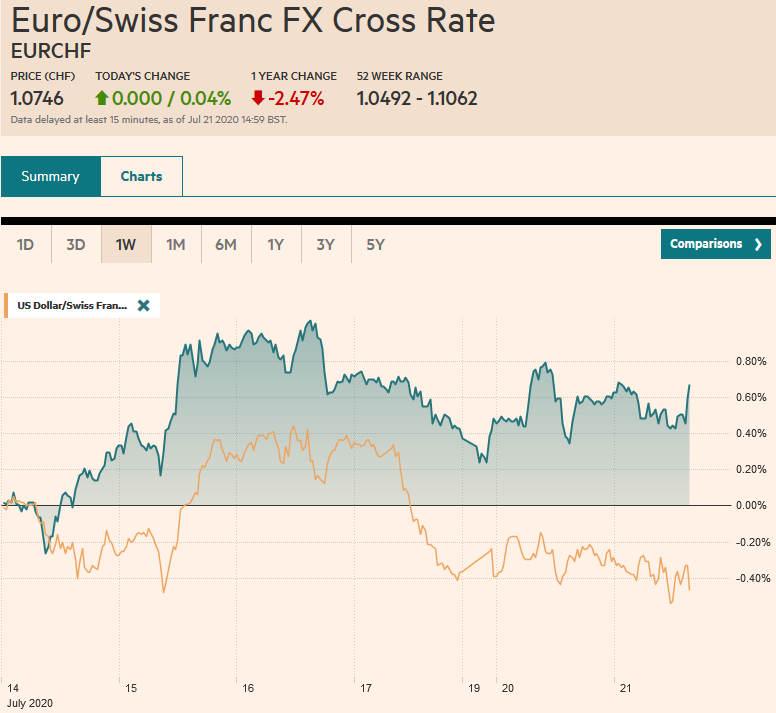

Swiss FrancThe Euro has risen by 0.04% to 1.0746 |

EUR/CHF and USD/CHF, July 21(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The continued domination of the tech sector and Europe’s tentative agreement are lifting equities and risk assets more generally today. Australia and Hong Kong’s 2.3%-2.5% rally led Asia Pacific markets. The Dow Jones Stoxx 600 is higher for a third session and above its 200-day moving average for the first time since February. The Dax is turning positive on the year. The S&P 500 did so yesterday, though nearly 2/3 (320 companies) remain lower on the year. The S&P 500 is set to gap higher and is likely to move into the old gap (February) between roughly 3260 and 3328.5. The European peripheral yields are falling by a couple of basis points, and Italy’s two-year yield is below zero for the first time in five months. Core yields are little changed, as is the US 10-year benchmark (~61 bp). The dollar is mostly lower, led by the Australian and Canadian dollar and the Scandis. The euro, yen, and Swiss franc are hovering around little changed levels. Most emerging market currencies are stronger, led by the liquid and accessible currencies, like Russia, South Africa, and Mexico. The Chinese yuan, alongside the Singapore dollar, slipped lower. Gold has made a new multiyear high near $1825, and crude oil is firm, with the September WTI contract near recent highs around $41.50. A gap we have targeted extends toward $42.50. |

FX Performance, July 21 - Click to enlarge |

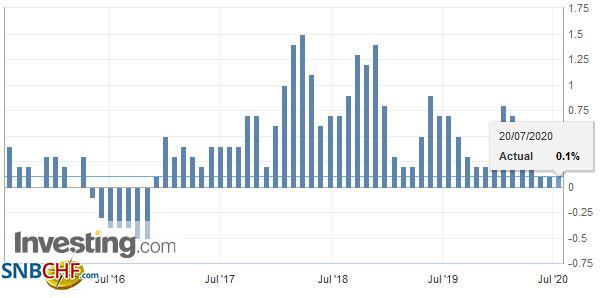

Asia PacificJapan’s June CPI readings were largely in line with expectations. Headline inflation was steady, rising by 0.1% over the past year. However, the core rate, which excludes fresh food, ticked up to zero from minus 0.2%. This is a touch stronger than expected. It is the first time in three months, the core rate is not below zero. When fresh food and energy are excluded, June prices rose by 0.4%, the same as in May. Phone services and durable goods prices rose. It is not a gamechanger. Last week, the BOJ forecast inflation would fall by an average of 0.5% this fiscal year. Energy prices stabilized. Gasoline, for example, fell 12.2% year-over-year after falling nearly 16.5% in May. |

Japan National Consumer Price Index (CPI) YoY, June 2020(see more posts on Japan National CPI, ) Source: investing.com - Click to enlarge |

South Korea’s trade figures for the first 20-days June were weaker than expected, and are seen as a cautionary bellwether for the region. Exports fell by 12.8% year-over-year, after falling 10.9% in May. It was partly distorted by the number of business days, and when adjusted accordingly, exports fell 7.1%. Imports fell 13.7% after falling 11.2% in May. Semiconductor chip exports were off 1.7%. In June, they were flat. The exports of computer peripherals rose by almost 57%. On the other hand, the import of semiconductor fabrication equipment rose more than 131% from a year ago after a 140% rise in June and a 168% increase in May as new investment takes place. Of note, shipments to China fell by 0.8% year-over-year after increasing 9.5% in June. Exports to the US, Europe, and Japan are still falling on a year-over-year basis, but the pace has slowed.

The dollar is in a quarter of a yen range in the first half of today’s 24-hour session below JPY107.40. It is the fourth session that the greenback is recording higher lower. There are options for $1.1 bln that expire today between JPY107.30 and JPY107.35. There is another set at JPY107.55 for nearly $450 mln. The Australian dollar is moving higher for the third consecutive session and is trying to solidify a foothold above $0.7000. The next immediate target is the post-crash high set last month, a little below $0.7065. The intraday technicals are stretched in the European morning. The PBOC’s reference rate for the dollar of CNY6.9862 was a little weaker than the models suggested. China’s money market rates have fallen in recent days, and the 10-year yield fell three basis points to 2.91%, the lowest in a couple of weeks.

Europe

Initially, Merkel and Macron proposed 500 bln euros in grants as the core of the Recovery Plan, and that apparently has been negotiated down to 390 bln and 360 bln in low-interest loans. The rhetoric got brutal as Dutch Prime Minister Rutte, whose party has only half the seats in Parliament and hence in a vulnerable political position, was accused of blackmail. European Council President Michel may have found a compromise with a handful of creditors, in part by granting nearly 53 bln euros in rebates (to Denmark, Germany, Netherlands, Austria, and Sweden). Hungary appears to have secured a dilution of the “rule of law” conditionality, and the Article 7 procedures against it will be closed by the end of the year, according to reports. This may prove to be controversial for the European Parliament that also must approve the agreement. Michel’s compromise also includes some conditionality and a mechanism for qualified majority voting that dilutes the veto of the unanimity requirement. The newest proposal will be cast as more friendly for the creditor countries, it also injects more Europe into the Recovery Plan as well. Separately, EC is proposing to put a level on imports of goods from countries that have lower carbon emission standards than it does.

The eurozone reported an 8 bln euro current account surplus for May. In May 2019, its current account surplus was 23.3 bln euros. In the first five months of 2020, the eurozone current account surplus has averaged 14.3 bln euros compared with 26.3 bln in the first five months of 2019. Despite the falling external surplus, the euro is rising for the third consecutive month. It is within striking distance (though probably not today) of the year’s high a touch below $1.15. The next target is last year’s high set near $1.1570.

The UK reported a June budget shortfall of GBP35.5 bln, which brings the deficit in the first three months of the new fiscal year to almost GBP128 bln. That is a little more than double the deficit of the previous fiscal year. The government is spending and cutting taxes by GBP190 bln to help cope with the pandemic. A deficit of GBP370 is projected this fiscal year or around 19% of GDP. Meanwhile, the Bank of England has purposefully not rejected a sub-zero base rate, and the yield curve is negative out seven years.

The euro reached $1.1470 in Asia but has not been able to sustain the momentum. There is an option for 650 mln euros at $1.15 that will be cut today. It has found support near $1.1430 in the European morning—yesterday’s low a hair above $1.1400. A close below $1.1420 would be disappointing and would be the first close below the five-day moving average in nearly two weeks. Note that an option for 1.3 bln euros at $1.1450 expires tomorrow. Sterling rose above $1.27 for the first time in more than a month and briefly traded above its 200-day moving average (~$1.2705). Here too, the early momentum could not be sustained, and sterling is consolidating in the European morning. Initial support is seen near $1.2650. After reaching almost GBP0.9140, a new high for July, the euro reversed course and settled below the pre-weekend low. Follow-through selling today has seen the euro test GBP0.9000. Last week’s low was near GBP0.8945.

America

The Trump Administration has two targets in mind with the sanctions and tariffs on China. Of course, in the first instance, it wants China to change its behavior. However, often overlooked is that it wants companies to change their behavior as well. US Attorney General Barr was as explicit as any official has been: Apple, Disney, and other companies are pawns of China. Eleven more Chinese companies were put on the entity list for aiding human rights abuses. Two of the companies claim to have previously supplied product for Apple and several popular clothing labels. It raises questions about the resilience of supply chains in China. At the same time, last week, Luxshare bought a couple of Wistron factories that assemble iPhones in China. Apple now has a local partner. Taiwanese companies appear to have a two-prong strategy to compete: exit low margin-business and develop production facilities in India.

A Republican Senator from Louisana (Kennedy) has said he will support Shelton’s controversial nomination to the Federal Reserve at the Senate Banking Committee today. All 13 Republican Senators on the committee must approve her to take the vote to the entire Senate. The other nominee Waller is considerably less controversial and will easily be approved. Separately, even though the Republicans have not entirely sorted out its fiscal stance, negotiations between Treasury Secretary Mnuchin and House leader Pelosi are set to get underway today. There seem to be three key issues for Mnuchin: A payroll saving tax cut (strongly favored by the President), limiting the liability of businesses re-opening, and not a renewal of the $600 a week in federal unemployment assistance.

Canada reports May retail sales today. A sharp jump (~20%) is expected after a 26.4% plunge in May. Canada will report June CPI figures tomorrow. While the headline has been weak due to energy prices, among others, the underlying measures have held up considerably better. Mexico reports May retail sales tomorrow. A modest 3% rise is expected after tumbling 22.4% in April.

The US dollar has pushed below the CAD1.35 support area, which also houses the 200-day moving average. It is testing the recent low near CAD1.3485 after posting an outside down day yesterday. The June low would be the next obvious target, set near CAD1.3315. The intraday technicals are stretched, suggesting that North American operators may have difficulty sustaining a significant range-extension now. The greenback reversed lower against the Mexican peso yesterday as well. Some follow-through selling has pushed it to around MXN22.3850 today (~MXN22.7650 was yesterday’s high). Support is seen near MXN22.25 and then MXN22.15.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,$CNY,Currency Movement,EU,Featured,federal-reserve,newsletter,South Korea