Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

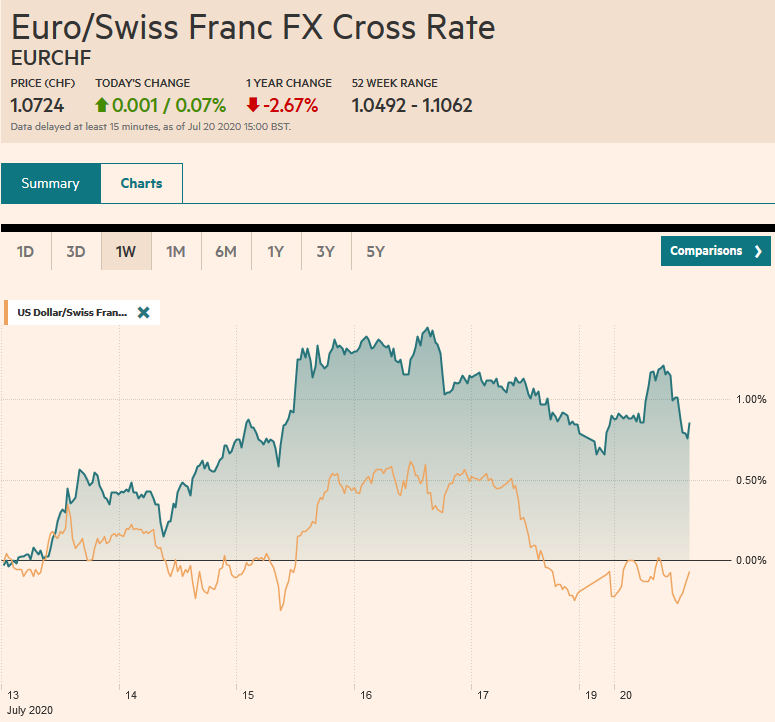

Swiss FrancThe Euro has risen by 0.07% to 1.0724 |

EUR/CHF and USD/CHF, July 20(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: While there are signs that Europe has reached a compromise on the grant/loan issue, the spillover into the markets is quite limited. China, with Shanghai’s 3.1% gain, led a few markets in the Asia Pacific region higher, including Japan and India. Most markets were lower, and Europe’s Dow Jones Stoxx 600 is a fractionally firmer, recovering from initial losses. US shares are a little heavy. Bond markets are quiet, with the US 10-year quiet around 61 bp and European peripheral yields off mostly1-2 bp, though Italy’s 10-year yield has slipped four basis points to about 1.12%. Core European yields straddle unchanged levels. The dollar is mostly softer against the major currencies, though the Swiss franc and Japanese yen are nursing small losses. The Scandis are up around 0.3%-0.4% to lead the move. Emerging market currencies are mixed. Eastern and central Europe, outside of Turkey, are generally firmer, while several East Asian currencies, including Indonesia and Thailand, are weaker. Gold is little changed around $1810, and September WTI is in about a 30-cent range on either side of $40.50. |

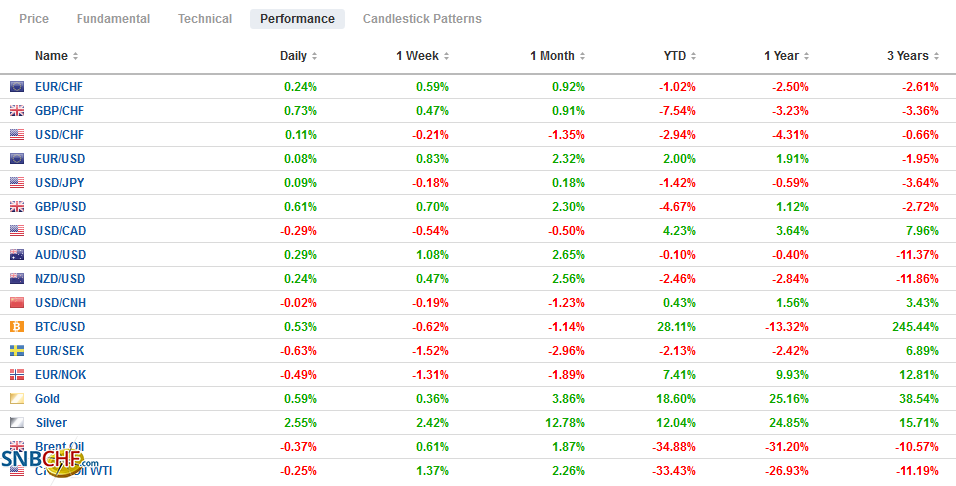

FX Performance, July 20 - Click to enlarge |

Asia PacificJapan recorded a June trade deficit of about JPY269 bln. It was about a third of the size of the May deficit but still considerably wider than expected and points to a considerable drag on Q2 GDP. Exports were weaker than forecast, falling 26.2% from a year ago. Economists forecast almost a 25% drop after a 28.3% fall in May. The decline in imports moderated more than expected. The 14.4% decline followed a 26.2% decline in May. The forecast was for around a 17.5% decline. Japanese exports account for a modest 15-18% of GDP, and foreign demand remains weak. Exports to the US were off 46.6%, but even exports to the rebounding China are uninspiring, down 0.2%. Japanese auto exports have been nearly halved from a year ago, and this reflects weakness in the US and Europe. However, auto exports jumped almost 19% to China after falling more than 20% in May. |

Japan Trade Balance, June 2020(see more posts on Japan Trade Balance, ) Source: investing.com - Click to enlarge |

Chinese regulators announced it was lifting the caps on equity investment from insurance companies. The maximum had been 30% of total assets. It is now 45%. Officials appear to be trying to bolster equities and, at the same time, curb excessive retail enthusiasm. Separately, the PBOC left the benchmark one-year Prime Loan Rate unchanged at 3.85% (five-year was also unchanged at 4.65%). It was the third month the rate was steady, and it illustrates the official cautious approach.

Australia updates its economic and fiscal outlook this week. It begins off with the RBA minutes tomorrow and Governor Lowe’s comments. The head of Australia’s banking regulation speaks Wednesday, leading up to the Treasurer Frydenberg’s update on Thursday. He is expected to project a 10% deficit in the new fiscal year that just began. Frydenberg already indicated that support for small businesses and extended employment schemes that are slated to end in September.

The dollar began on a firm note, rising a little above JPY107.50 for the first time in more than a week, but was greeted with new selling that pushed it below JPY107.20 by early European activity. There is an option fo about $475 mln at JPY107 that expires today. The Australian dollar is in a narrow range around $0.7000, and trading just inside the pre-weekend range. Last week’s high was just shy of $0.7040. Despite repeatedly testing the $0.7000 area over the past six weeks, the Aussie has only closed above it twice (once in June and once so far here in July). The PBOC set the dollar’s reference rate a little weaker than the models implied at CNY6.9928. Meanwhile, the central bank continues to inject liquidity into the banking system, and this is serving to drive down money market rates, including the overnight repo rate (~-36 bp to 1.95%). The seven-day repo rate fell for the second consecutive session and at 2.16%. In late March, the seven-day repo rate was cut to 2.2% from 2.4%.

EuropeIt is not official, but marathon negotiations appear to have produced an agreement on the Recovery Plan that would include 390 bln euro in grants and the remainder in loans. The at-times acrimonious talks will continue later today. The failure to reach an agreement was thought likely to fan populism in southern Europe, while the Dutch Rutte has exactly half the seats in the national parliament, and a misstep would see the government fall. On both sides of the issue, domestic politics were important considerations. We suspect whether or not this proves to be the “Hamiltonian moment” that many heralded will be decided in future negotiations and debates. Meanwhile, still to be resolved is the Hungarian/Polish position that is reluctant to support any measures that are conditional upon “the rule of law” demands by Brussels. |

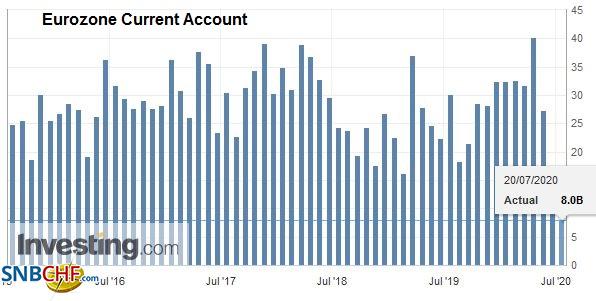

Eurozone Current Account, May 2020(see more posts on Eurozone Current Account, ) Source: investing.com - Click to enlarge |

After announcing a plan to remove Huawei, the UK joined the US, Canada, and Australia in suspending its extradition treaty with Hong Kong. New Zealand is also reportedly considering a similar measure. Separately, the UK and EU negotiating teams resume talks today. Many suspect that if there is no closing of positions in this round, the chances of an agreement dim. We already suspected the odds are tilted against, and what is involved is the extent of the disruption of the exit from this year’s standstill agreement.

The euro is firm and is within striking distance of the year’s high set in March just below $1.1500. However, intraday technicals are stretched, and the 1.1 bln euros in an expiring option at $1.15 looks safe. There are expiring options at $1.1450 (~615 mln euros) and $1.1425 (~845 mln euros). There are 2.6 bln euros in options at $1.14 will be cut. Sterling is firm after the 20-day moving average continued to lend support (~$1.2505). It moved above the pre-weekend high (~$1.2575) in the European morning on the back of the weaker US dollar. However, here too, the intraday technicals are stretched, and North American traders are likely to take advantage of the better prices to sell.

America

The Republicans are close to finalizing a proposal to counter the House’s $3.5 trillion bill passed several weeks ago. The negotiations can begin in earnest tomorrow for the fifth fiscal package since the pandemic struck. There is a limited window of opportunity as some fiscal measures, like the $600 a week federal unemployment, are set to expire shortly. There is also the annual legislative recession that is set to start August 10, The Federal Reserve and former Fed chairs, Yellen and Bernanke have advocated more fiscal support. The IMF has also endorsed more fiscal stimulus.

Judging from the recent public comments, the Federal Reserve is getting more concerned about the possibility the economy is losing some momentum. It widened the Main Street facility at the end of last week to include more non-for-profits, but this is likely fiddling on the margin. Some observers read greater urgency from the Fed and are playing up the risk that it could move as early as next week, with yield curve control measures, or possibly stepping up its bond purchases. While data from US retail sales, industrial output, and housing starts showed robust gains, the disappointingly firm weekly jobless claims have become somewhat of a pattern.

The US will bring over $175 bln of bills to market this week. Remember, while the Treasury is funding itself primarily in bills, the Federal Reserve is buying mostly coupons. The Treasury will also sell $17 bln in the new 20-year maturity and $14 bln of 10-year inflation-protected securities. Separately, dealers expected $15-$20 bln of investment-grade corporate bonds to be issued this week after $12 bln last week. Tech companies move into the center of the earning stage, with IBM, Microsoft, Intel, and Texas Instruments among the bellwethers. Tomorrow, the Senate Banking Committee takes up the Wallen and Shelton Federal Reserve nominations. The latter is more contentious than the former, but the odds seem to favor approval by the committee before the nominations get taken up by the entire Senate.

The US dollar found keen sellers near CAD1.36 in Asia. It did not find buyers until the European morning near CAD1.3565. There is support a bit lower, but the greenback is stretched on an intraday basis, and a bounce is likely. Last week’s high was around CAD1.3645. Meanwhile, the US dollar is walking down a trendline against the Mexican peso that comes in today near MXN22.60. A close above the pre-weekend high of around MXN22.6125 would violate the nearly three-week-old trend and signal a correction that would target the MXN22.80-MXN23.00 area. The greenback gained against the Brazilian real for the second week in a row last week, but it remains mostly in a BRL5.25-BRL5.50 trading range.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: $CNY,China,Currency Movement,EU,Featured,Japan,newsletter,SPX,US