Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

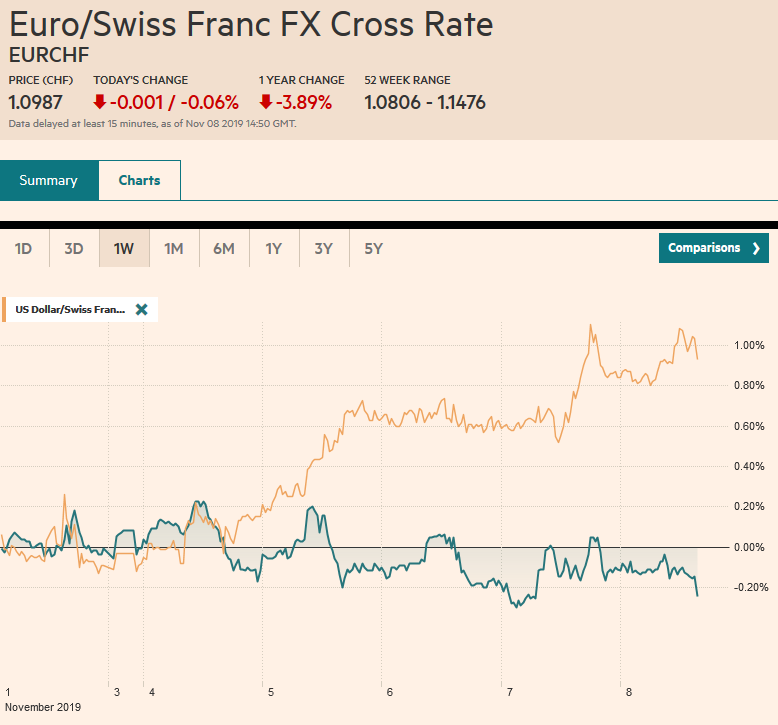

Swiss FrancThe Euro has fallen by 0.06% to 1.0987 |

EUR/CHF and USD/CHF, November 8(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The capital markets are consolidating the recent moves ahead of the weekend. Equities are paring this week’s gains, though the Nikkei, which was closed on Monday, extended its advance for the fourth consecutive session. Despite the profit-taking today, the MSCI Asia Pacific Index rose for the fifth week. Europe’s Dow Jones Stoxx 600 is snapping a five-day rally, but it is closing in on the fifth consecutive weekly advance. US shares are trading softer. It is up a modest 0.6% this week coming into today, where a five-week rally is on the line. The dramatic equity rally is being matched by just as dramatic sell-off in bonds. French, Belgian, and Swedish 10-year yields moved above zero for the first time in several months, The US 10-year benchmark yield pushed above 1.90% to new three-month highs. US and European yields are slightly softer today after the Asia Pacific yields backed up in line with the move in Europe and America yesterday. The amount of negative-yielding bonds has fallen more than a quarter since August to around $12.5 trillion. The US dollar is trading with a slightly firmer bias against nearly all the world’s currencies today. Oil is paring yesterday’s gains, and near $56.50 WTI for December delivery is up almost 0.6% on the week. Gold continues to trade heavily. It is off a little more than 3% for the week, which is its biggest weekly loss in a couple of years. |

FX Performance, November 8 - Click to enlarge |

Asia PacificChina reported its October trade figures. Exports fell less than 1% year-over-year. A Reuters survey found a median forecast for a 3.9% decline after a 3.2% fall in September. Imports fell by 6.4% in October. The median forecast in the Reuters survey was for an 8.9% decline. Imports fell by 8.5% in September. The overall trade surplus rose to $42.8 bln, from $39.6 bln. Over the past 12 months, China’s trade surplus stands at $439 bln, up from $344.5 bln last October. Exports to the US are off 16.2% year-over-year after nearly a 22% decline in September. |

China Trade Balance, October 2019(see more posts on China Trade Balance, ) Source: investing.com - Click to enlarge |

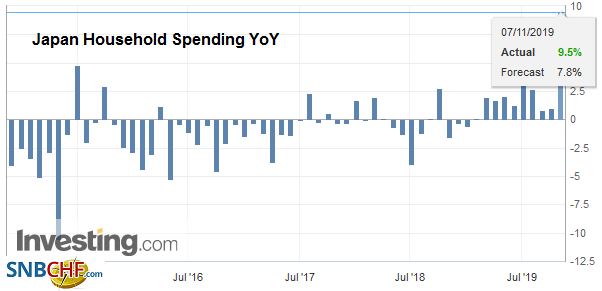

| Ahead of the hike in Japan’s sales tax on October 1, consumers went on a shopping spree. A surge in retail sales was already reported, and earlier today, the more comprehensive household spending report confirmed it. September’s household spending jumped 9.5% year-over-year after a 1.0% rise in August. This was the most since the 7.2% increase in 2014 before the previous sales tax increase. The problem is that it brings the buying forward. This, coupled with the typhoon, warns of a weak Q4.

Moody’s cut the outlook of India’s creditworthiness to negative from stable citing shadow banking challenges and the likelihood of a prolonged economic slowdown. The Baa2 rating is the second-lowest investment-grade rating, which is one step ahead of S&P and Fitch (both have stable outlooks). The deficit this year is projected to be near 3.7% of GDP, more than the government’s target of 3.3%. Further fiscal deterioration may spur a ratings cut, Moody’s said. |

Japan Household Spending YoY, September 2019(see more posts on Japan Household Spending, ) Source: investing.com - Click to enlarge |

In a big outside up day, whereby the US dollar traded on both sides of Wednesday’s range and closed above Wednesday’s high, the dollar reached almost JPY109.50 yesterday. That is its best level since late May. It is consolidating today in a narrow range above its 200-day moving average (~JPY109.05). There is increasing talk of JPY110, the next target. The Australian dollar traded on both sides of Wednesday’s range yesterday but did not close above that high yesterday and is back near yesterday’s lows (~$0.6860). The market appears to be giving up on the $0.6900 level, let alone the 200-day moving average (~$0.6950), which is capped rallies since last December. A close below $0.6950 would weaken the technical tone. The dollar initially extended its eight-day slide against the Chinese yuan but bounced back in late dealings. The PBOC fix was a slightly higher US dollar than the bank models implied. The greenback finished the mainland session below CNY7.0 for the third consecutive session. The offshore yuan did not trade as well as the onshore yuan, and it may hint at a better dollar performance next week.

Europe

Outgoing EC President Juncker appeared to speak confidently in claiming that the US was unlikely to impose tariffs on European auto imports next week. The threat has been hanging over Europe for the past six months. There had been some recent press stories suggesting that the US talks with European auto companies directly had been favorable. Still, given the underlying tension on a range of issues between the US and Europe, it is difficult to imagine that there will be no US action. The Commerce Department’s report six months ago warning that the auto imports were a threat to national security would seem to require some formal response. Will supply chains really shift as part of America’s import substitution strategy under the rubric national security? Will they be forced to under the domestic content provisions of the new USMCA, which still needs to pass the US Congress?

Germany reported better trade data, and by better it means exports and imports were stronger than expected. Exports rose 1.5% (month-over-month) in September, five times stronger than the median Bloomberg forecast and the best since November 2017. The August decline was halved to 0.9%. Imports rose by 1.3% after August’s 0.5% gain was cut to 0.1%. The increase in imports was the largest since July 2018. The net result was that the trade surplus increased to 21.1 bln euros from a revised 16.4 bln euro surplus in August. German data has been uneven, and next week it is expected to confirm a second consecutive quarterly contraction. However, we continue to suspect that the German economy is bottoming. Separately, French economic data (September industrial and manufacturing output, Q3 private-sector ) were better than expected. The trade balance deteriorated in September, but the current account deficit was reduced.

The euro is pinned near yesterday’s lows (~$1.1035) in a narrow range of less than a fifth of a penny. At the start of the week, it appeared that the momentum allowed one more leg up before a correction unfolded. It rose every session last week. That momentum did not carry into this week, and the euro fell every day this week. It has approached the (50%) retracement of its rally since October 1 (~$1.1030). A break of that likely signal a near-term push below $1.10. There is an option for about 870 mln euros at $1.1050 that expires today that may deter the upside ahead of the weekend. Sterling is hovering around unchanged levels today, but it has not closed higher this week. It is off about 1.3 cents this week. It is in a fifth of a cent range today above $1.28, where it has found support over the last few weeks. There is an option for GBP830 mln at $1.28 that rolls off today and another more nearly GBP260 mln at $1.2825 that also expires today.

America

It seems that both Chinese and US officials have confirmed that if there is an agreement, it will include some unwinding of existing tariffs. Reports indicate that some US officials claim it was not part of the original handshake deal last month. On the other hand, China has repeatedly insisted that the removal of the tariff threats for Oct 15 (initially Oct 1) and December 15 were not sufficient. The US appears to be willing to roll back (de-escalate) some tariffs as a sign of good faith, but wants to keep the majority until certain targets are achieved after the agreement. So as the week winds down, there still is no agreement on when or where the two presidents will meet or even if the handshake agreement can be codified. Is the market getting ahead of itself?

The US reports wholesale trade and inventory data, which is more important for economists fine-tuning Q3 GDP revisions that market participants. Following news that the Bloomberg Weekly Consumer Comfort Index fell to six-month lows last week, the University of Michigan’s Consumer Sentiment report will be looked upon for confirmation. The long-term (5-10 year) inflation expectation was in its trough (2.3%) in September. Did it increase in October? Next week the US reports October CPI, which is expected to be unchanged at 1.7% at the headline level and 2.4% at the core. The Fed’s Brainard and Daly speak today at a conference on climate change. Increasing we are hearing major central banks devote more time and mindshare to contemplating the economic consequences of climate change. At the end of the day, NY Fed’s Williams participates in a Q&A on global financial vulnerabilities.

Canada reports October jobs data. It is unreasonable to expect that it was able to come close to duplicating the 70k surge in full-time jobs in September. In a relative sense, it would be if US non-farm payrolls rose around 800k. The Bank of Canada softened its neutrality, but the market is not expecting a cut until well into next year. A shockingly poor report could see it brought forward. Mexico reported slightly firmer October CPI yesterday, but it is not seen standing in the way of a central bank rate cut next week.

The US dollar is flirting with a two-week high near CAD1.3200. It looks poised to test the CAD1.3230 area, and possibly 200-day moving average near CAD1.3275. A move below CAD1.3180 may signal that the upside momentum has been exhausted. It finished last week near CAD1.3140. The greenback has traded in a roughly MXM19.05-MXN19.25 range this week. It has rarely been out of that range in recent weeks. Although the market appears to be taking some profits on risk positions today, intraday technicals warn of the potential for the dollar to move toward the middle of the range.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,$CNY,Bonds,China,China Trade Balance,Currency Movement,EUR/CHF,Germany,India,Japan Household Spending,newsletter,Trade,USD/CHF