Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

Swiss FrancThe Euro has fallen by 0.10% at 1.108 |

EUR/CHF and USD/CHF, July 15(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The new record highs in US equities ahead of the weekend coupled with Chinese data that suggested the economy was gaining some traction as Q2 wound down is helping underpin risk appetites to start the week. Japanese markets were closed today, but equities were mostly firmer in the Asia Pacific regions, markets in China, Hong Kong, Taiwan, and India firmed. Europe’s Dow Jones Stoxx 600 was marginally higher through the morning session, and US shares also enjoyed a firmer bias. Benchmark 10-year yields were mixed. Asia Pacific bond yields were dragged higher by the rise in US rates at the end of last week, while yields are two-four basis points lower in Europe. The dollar is narrowly mixed, +/- 0.15% band against most of the majors, with the New Zealand dollar the main exception. It pushing higher ahead of the Q2 CPI report first thing Tuesday in Wellington, helped by sales against the Australian dollar. |

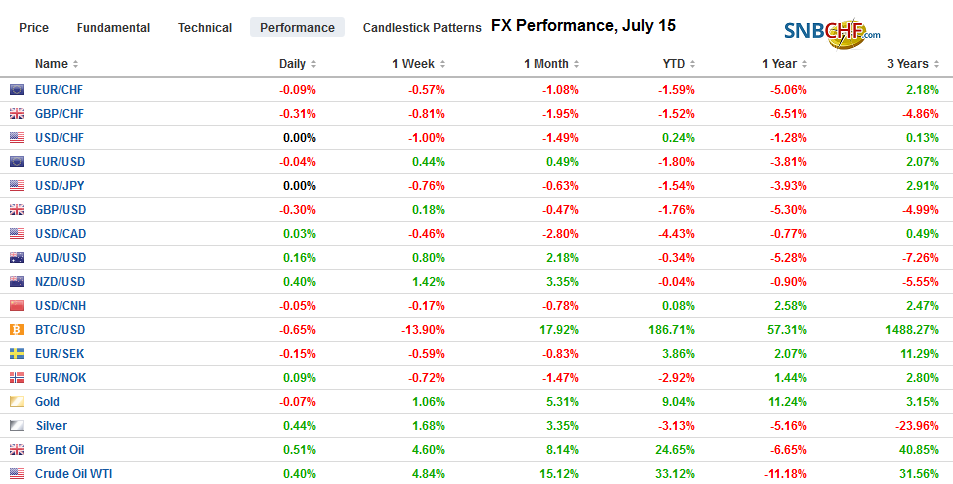

FX Performance, July 15 - Click to enlarge |

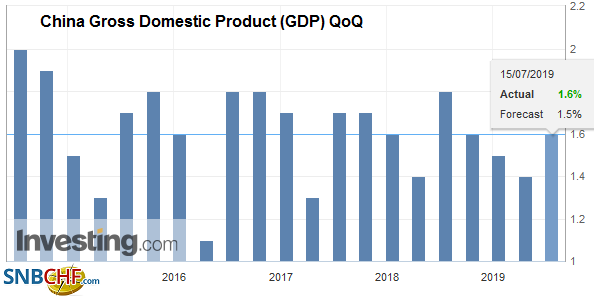

Asia PacificChina’s 6.2% year-over-year GDP in Q2 19 was the weakest in more than a quarter of a century and follows a 6.4% reading in Q1. However, investors see the proverbial glass as half full because the June reports all bested expectations and May’s results. |

China Gross Domestic Product (GDP) QoQ, Q2 2019(see more posts on China Gross Domestic Product, ) Source: investing.com - Click to enlarge |

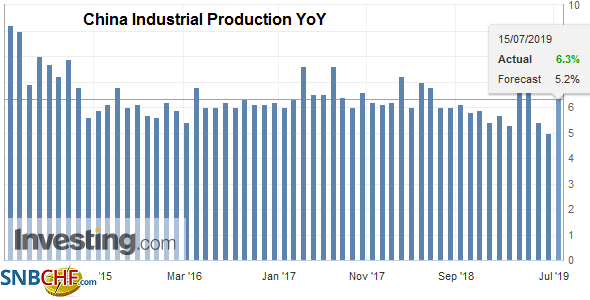

| Industrial output rose 6.3% year-over-year after the 5.0% increase in May. |

China Industrial Production YoY, June 2019(see more posts on China Industrial Production, ) Source: investing.com - Click to enlarge |

| Retail sales increased to 9.8% from 8.6% year-over-year, and fixed asset investment rose 5.8% from 5.6%. Despite the world’s second-largest economy finding better traction, more support from the government and central bank are expected. The risks are still biased to the downside, and the trade tensions may be at a lull as talks resume, but progress remains difficult. Reuters reported that US companies may not get the licenses to sell to Huawei for two-four more weeks, while other reports suggest China has not stepped up its purchases of US agriculture. Other reports indicate that China may sanction some US companies if the US goes forward with the $2 bln weapons package to Taiwan. |

China Retail Sales YoY, June 2019(see more posts on China Retail Sales, ) Source: investing.com - Click to enlarge |

The Financial Times provided two pieces of insight into developments in Hong Kong, where protests continued over the weekend. First, Chief Executive Lam reportedly has offered her resignation several times, but Beijing has refused it. Second, and related, is that the situation is considered Lam’s doing because the controversial extradition bill was her initiative’s not Beijing’s. The idea is that she ought to clean up the mess she created. She is the fourth chief executive since the handover from the UK, and they all left office under a cloud of distrust.

The Australian dollar is trying to extend its advance for the fourth consecutive session today. However, it has stalled near $0.7035 in both Asia and the European morning. Above there is the high from earlier this month near $0.7050, though we have suggested technical potential toward $0.7100. Support is pegged in the $0.6980-$0.7000 area. Without the local participants, the yen has been sidelined today. The dollar remains pinned near its recent lows around JPY107.80. It has spent practically no time above JPY108.10. We suspect the range can be extended in North America and see resistance in the JPY108.40-JPY108.50 area. The Chinese yuan continues to move sideways, and it spent today’s mainland session mostly within the pre-weekend range.

Europe

Tomorrow the EU Parliament will vote on the Von der Leyen’s nomination as the next European Commission President (to replace Juncker). She needs a simple majority, which is the support of 374 MPs. The Leftists and Green’s are not supporting her. The ostensible reasons are that she is a compromise candidate and was not discussed before the vote, and her agenda is not sufficiently ambitious. The Social Democrats and Liberals have demanded additional commitments, and the interest in the “rule of law” in this context is about confronting the illiberal actions in Hungary and Poland despite their seeming ability to veto Timmermans’ nomination. The PP, which secured a plurality of MPs in the election support her as does Macron’s Renaissance. PredictIt.Org wagers show she widely to be confirmed (~9-to-1 odds). Separately, it is not clear what the precedent means for the “spitzenkandidat” process of ensuring the electoral process and the European Parliament has a greater role in shaping its executive arm (European Commission).

Turkey may be challenged this week. Before the weekend, Fitch reacted to the dismissal of the central bank governor by downgrading Turkey to BB- and maintaining a negative outlook. It still a notch above the equivalent at Moodys (negative outlook) and S&P (stable outlook). Today is the three-year of the anniversary of the failed coup attempt, rather than draw fresh attention to it, the US will reportedly announce sanctions against Turkey over the next week or so for purchasing Russia’s anti-aircraft missile defense. President Erodgan has played down the threat of sanctions, suggesting the Trump may override his staff recommendations. The issue of sanctions seems when not if, but the question about interest rates is not when but how much. The central bank meets on July 25 and Erodgan’s unorthodox understanding that high-interest rates cause inflation will be put to get. The one-week repo rate stands at 24%. Inflation expectations have fallen 250 bp since peaking last November near 17.4% (June estimate will be reported toward the end of the week). The interest rate premium may not be only inflation but could be compensation of other risks as well, such as political risk.

The euro is firm near last week’s highs (~$1.1285) but has gone nowhere, confined to a fifth of a cent range. A modest (535 mln) euro option struck at $1.1275 expires today. The broader range of around $1.1240-$1.1290 may mark the most the can be hoped for without fresh incentives. Sterling edged to a marginal new seven-day high just above $1.2580, but it is struggling to sustain even a modicum of upside momentum and the 20-day moving average just above $1.26 may deter the upside. Support is pegged near $1.2520.

America

With a July rate cut by the Fed as done of a deal as these things get, market participants must turn their attention from Q2 to Q3. Today’s Empire State survey is the first data point, outside weekly jobless claims, for July. The median forecast in the Bloomberg survey is for a 2.0 reading up from -8.6 in June. It is still yellow-card territory as the June reading had fallen off the proverbial cliff, having averaged almost 15 in the previous two months. The July Philadelphia Fed survey will be released later in the week and is expected to show the same profile: the breakdown in June was partly recovered in July. Canada reports June existing home sales. There may be some downside risks after solid gains in April and May (1.9% and 3.6%, respectively).

With the US debt ceiling and spending authorization issues not resolved, many observers are getting more pessimistic about the likelihood that the US Congress passes the USMCA this year. We have long been skeptical of the prospects. In the past, Congressional approval of free-trade agreements has required careful coordination and some tough negotiating, which does not appear present now. There seems to be little interest in bipartisan action. Since July 4, PredictIt.Org wagers give ratification at less than a 30% chance.

The US dollar is pinned near the year’s low against the Canadian dollar recorded before the weekend near CAD1.3020. The CAD1.3000 level is more important psychologically than technically. The charts warn that a break of CAD1.3000 may spur a move toward CAD1.2960. The US dollar is trading heavily against the Mexican peso. Near MXN18.9350, the dollar is at its lowest level since last week’s surprise resignation of the finance minister, which saw the dollar spike to around MXN19.3550. The day before the resignation, the greenback closed near MXN18.81. The Dollar Index is testing support in the 96.70-96.80 area that houses the 200-day moving average and the (50%) retracement objective of the rally from the late June lows.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,$CNY,China,China Gross Domestic Product,China Industrial Production,China Retail Sales,Currency Movements,EUR/CHF,newsletter,Turkey,USD/CHF