Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

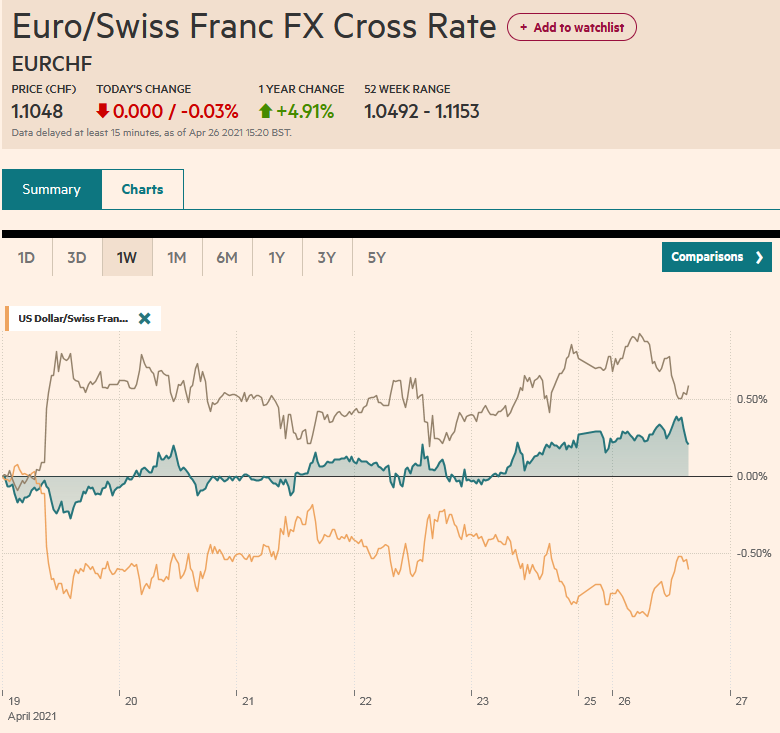

Swiss FrancThe Euro has fallen by 0.03% to 1.1048 |

EUR/CHF and USD/CHF, April 26(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: What promises to be a notable week has begun off quietly: the US, EMU, and South Korea report Q1 GDP. The eurozone also provides its first estimate of April inflation. Corporate earnings feature tech and financial firms. Equities are mostly firmer in the Asia Pacific region and Europe. Hong Kong, China, and Australia were exceptions, and their equities slipped lower. Taiwan, South Korea, and Indian indices advanced. Europe’s Dow Jones Stoxx 600 snapped a seven-week advance last week but is slightly higher today. US futures are narrowly mixed. Ahead of the FOMC meeting and US data, the yield of the 10-year benchmark is firm near 1.57%. Yields in Europe and the Asia Pacific area are a little higher as well. The dollar is sporting a soft profile. The euro rose a little above $1.2115. Sterling is trying to establish a foothold above $1.39, and the dollar-bloc currencies are firm. Among emerging market currencies, eastern and central European currencies, outside the Turkish lira and Czech koruna, are trading lower, while Asian currencies are mostly a little stronger. Gold is has edged up along with the industrial metals. A strike of port workers in Chile over being denied being able to have early withdrawals from their pension funds has driven copper prices to their highest level in a decade. Oil prices are softer amid concerns about weaker Indian demand. June WTI was turned back from the $62.30 area and is trading around a dollar lower near midday in Europe. Last week’s low was near $60.60. |

FX Performance, April 26 - Click to enlarge |

Asia Pacific

India reported a million new covid cases over the past three days as the pandemic surges. Its request that the US allows the export of the vaccine’s raw material was rebuffed on the grounds that the US had a responsibility to look after Americans first. A State Department spokesperson was quoted: “It is, of course, not only in our interest to see Americans vaccinated, it is in the interests of the rest of the world to have Americans vaccinated.” Aside from the hubris, it was a poor response, and the US quickly amended it. Between Friday and Sunday, a different tone was struck. The US will be sending India raw materials for the AstraZeneca vaccine and provide financial aid for vaccine production. The UK, Germany, and France pledged aid, as has China. The US has a stockpile of an estimated 20 mln AstraZeneca vaccines by earlier this month, but still, American regulators have not approved its use. It has loaned 4 mln vaccines to Canada and Mexico.

Japan held three byelections for the upper chamber of the Diet, and the LDP failed to win a single one. In Hokkaido and Hiroshima, scandals hit the LDP incumbents, and the seat in Nagano stays within a family dynasty. The results may be a warning to the LDP-Komeito national coalition. A general election needs to be held by late October. Prime Minister Suga’s support is waning. He continues to support going forward with the Olympics even Japan’s largest urban areas are in a formal state of emergency with less than 100 days before the opening ceremonies. Sunk costs and pride seem to be the main motivations for going forward.

Foreign exchange market participants drawn to seasonal patterns, but we are often unimpressed. Most recently, the claim is that the dollar typically rises against the offshore yuan by an average of 1.5% in May-June. The narrative links the yuan’s weakness to dividend payments, which peak this year in the June-August period. The five-year period is not long enough for serious analysis, and “average” could be deceiving if the dispersion of the data is high. Bloomberg’s data for CNH goes back to 2011. The dollar has risen in six of the past 10 May’s and four of the past 10 June’s. The dollar’s performance in May has ranged from falling 2.2% to rising by nearly 3.1%. In June, the greenback has rallied 3.5% and has also fallen by 1%. The most extreme pattern is actually in October when the dollar has risen twice in the past decade. Still, the sample size is too small to draw a meaningful conclusion.

The attempt to take the dollar higher stalled in Asia near JPY108.15. It trended lower to about JPY107.65 in early European turnover. It is holding above the pre-weekend low near JPY107.50. When/if this is taken out, the next target is near JPY106.80. The greenback settled last week a little below JPY107.90. A failure to close above there today would be the sixth consecutive dollar loss and the 10th in the past 11 sessions. The Australian dollar is firm, and a close near the current level (~$0.7775) would be the highest this month. Last week’s intraday high was about $0.7815. Note that the $0.7825 area corresponds to the (61.8%) retracement objective of the down move since the multiyear high was recorded in late February, a little above $0.8000. The Chinese yuan slipped lower ahead of the weekend to end a nine-day rally. The respite was brief, and the yuan traded higher today. The dollar eased from almost CNY6.4965 at the end of last week to CNY6.4855 today. Last week’s intraday low was about CNY6.4825, which was the greenback’s lowest level since mid-March. The reference rate has been predictable and has hardly deviated from the median in the Bloomberg survey. However, today the fix was for a somewhat higher dollar (CNY6.4913) than the models suggested (~CNY6.4893). The market is on the lookout for an official push back against additional yuan gains.

Europe

The April German IFO survey was mixed. The current assessment ticked up (94.1 vs. 93.1), but not as much as had been expected. While the vaccine rollout has accelerated, social restrictions have tightened. The expectations component softened (99.5 vs. 100.3) but remains at elevated levels. The net result was that the overall assessment of the business climate edged up to 96.8 from 96.6, which missed the median forecast (97.8).

The UK vaccine rollout continues, and over 50% of the adults have had at least one vaccine. Last week’s March retail sales (5.4% month-over-month) and April PMI (composite reading of 60.0 above the 2020 peak). However, political developments have not been so favorable, and local elections are a little more than a week away. The new antagonism comes from claims by Johnson’s former chief adviser and Brexit force Cummings. His claims of corruption, incompetence, and egoism appear to be dominating the news cycle.

This week’s economic highlights are all at the end of the week. Three EMU reports stand out; March unemployment (expected unchanged at 8.3%), April CPI (the year-over-year pace to increase to around 1.5% from 1.3%), and the first look at Q1 GDP (a contraction on par with Q4 0.7% contraction). ECB President Lagarde has already dismissed the CPI as being, well, inflated by technical and transitory factors. The PMI readings have held in better than expected, and this could indicate a more resilient regional economy than projected, but the market appears to have already largely written off Q1 for the eurozone.

The euro extended the pre-weekend advance and rose a little above $1.2115 to reach its best level since the end of February. It is struggling to maintain the upside momentum and has spent the European morning straddling the $1.2100-area. A break of $1.2080 might begin shaking out some of the new euro longs. Note that the (61.8%) retracement of the euro’s losses since the January 6 high and the trendline connecting the January and February highs are found just above $1.21. Sterling is firm after extended the pre-weekend week’s gains to almost $1.3930. Last week’s high was near $1.4010. The euro edged up to GBP0.8720, a new high since February, but it was greeted by sellers that pushed the euro back to around GBP0.8680 and may have helped cable.

America

The Federal Reserve Open Market Committee meets, the US releases its first estimate of Q1 GDP, the Treasury will auction over $200 bln of notes and bonds, but what has spurred the most consternation are the details that leaked last week about a proposed jump in the capital gains tax on for those who enjoy an annual income of more than a million dollars. Biden is expected to unveil the second half of the “build American back better” initiative, dubbed the “American Families Plan.” The price tax will be around $1.8 trillion and is aimed at childcare and education and includes more ambitious paid family leave. At least part of it is expected to be funded by at least half a dozen tax increases. A Bloomberg poll found 45% expect the Fed to taper in Q4, and nearly 15% expect the tapering in Q3.

Today’s US economic data feature is March durable goods orders. A strong rebound from the weakness in February is expected, and that coupled with the advanced goods trade balance and inventory data in the middle of the week are the last inputs to fine-tune GDP forecasts. The forecasts have been gradually improving toward nearly 7%, helped by projections of more than a 10% jump in consumption. Canada’s economic highlights include February retail sales on Wednesday (strong gain expected after a 1.2% decline in January) and February monthly GDP at the end of the week (~0.5% after a 0.7% rise in activity in January). Mexico’s economic diary highlights include March trade figures (tomorrow) and Q1 GDP on Friday (0.3% quarter-over-quarter is the median forecast in Bloomberg’s survey after a 3.3% expansion in Q4 20).

Last week, the Bank of Canada announced a 20% reduction in its weekly bond purchases and brought it forward to H2 22 when it anticipates the economic slack to be absorbed. The market understands that the closing of the output gap opens the window to a rate hike. The Canadian dollar is bid to start the week, and the US dollar has slipped through last week’s lows. There is little technical support before the CAD1.2400 area and the multi-year low set on March 18 near CAD1.2365. That said, note that the lower Bollinger Band (two standard deviations below the 20-day moving average) is found near CAD1.2455, where it is hovering near midday in Europe. The greenback is holding just above last week’s low against the Mexican peso (~MXN19.7850). It has not been above MXN20.00 since April 15. Coming into today, the dollar has fallen in eight of the past ten sessions against the peso. Here in April, the dollar is off around 3% against the peso after falling 2% in March.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,China,COVID-19,Currency Movement,Featured,India,Japan,newsletter,U.K.