Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

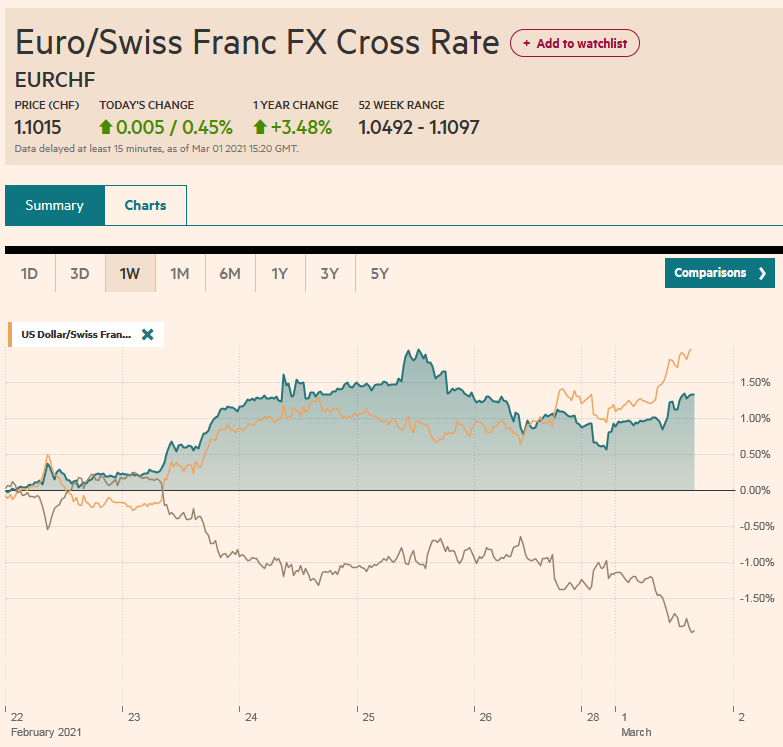

Swiss FrancThe Euro has risen by 0.45% to 1.1015 |

EUR/CHF and USD/CHF, March 1(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: Equities and bonds jump back. Most Asia Pacific markets advanced 1.5-2.5% after the regional MSCI benchmark dropped 3.65% before the weekend and 5.3% last week. The recovery in European stocks was even more impressive. The Dow Jones Stoxx 600 was up around 1.55% near midday, recouping the pre-weekend loss in full and making a gallant effort to recoup last week’s 2.4% loss. US shares are trading higher, and the futures’ benchmarks are up 1.0%-1.4%. While the US 10-year yield is firm at 1.43%, yields have fallen elsewhere. Benchmark yields are 4-7 bp lower in Europe. The markets await the ECB report to confirm it stepped up its bond-buying efforts last week. Australia’s 10-year yield plummeted nearly 25 bp following the central bank’s aggressive purchase today. New Zeland’s 10-year yield fell 17 bp. The dollar is back to the fulcrum among the major currencies. The dollar-bloc, Norwegian krone, and sterling trade higher, while the European complex and yen are weaker. Emerging market currencies are mixed as well. The freely accessible currencies, like Russia, Turkey, South Africa, and Mexico, advance. Central European currencies appear to be weighed down by the heavier euro. The JP Morgan Emerging Market Currency Index is posting minor gains after sliding 2.1% last week. Gold is recovering. It is up almost $12, around $1746, as it snaps a four-day slide of more than $75. April WTI is up almost $1 a barrel to recoup half of its pre-weekend drop. On February 1 was near $53.40. Today it is near $62.40. |

FX Performance, March 1 - Click to enlarge |

Asia Pacific

China’s manufacturing PMI fell to 50.6, the lowest since last May. The report was weaker than economists expected if understanding the Lunar New Year holiday would weigh on activity. New export orders fell to 48.8 from 50.2, and employment weakened further to 48.1 from 48.4. The non-manufacturing PMI softened to 51.4 from 52.4. It has not been this low since last February. Still, counterintuitively, the composite reading of 51.6 remained above both the manufacturing and non-manufacturing PMI, though down from 52.8. The Caixin manufacturing PMI was softer than expected to at 50.9 compared to 51.5 in January.

Japan’s manufacturing PMI was revised to 51.4 from 50.6 preliminary reading and 49.8 in January. It is the first reading above 50.0 since January 2019. Tomorrow Japan reports January employment data. Later in the week, the weekly portfolio flow report will be watched closely after last week’s report showed Japanese investors sold almost JPY1.9 trillion of foreign bonds, the most since August 2018.

The Reserve Bank of Australia meets first thing tomorrow. The upward pressure on interest rates challenges the credibility of its yield curve control policy that caps the three-year yield cash rate of 10 bp. It finished at 14 bp before the weekend, and despite its purchases earlier today, estimated to be more than A$3 bln, the yield is at 13.5 bp. The RBA is unlikely to be deterred by the market right away, and it will need to expand its bond-buying. Note that Australia runs a trade deficit with the US. Ostensibly, this would give it a freer hand to intervene in the foreign exchange market and not be accused of currency manipulation under the US Treasury rules. Australia’s manufacturing PMI was revised to 56.9 from the initial 56.6 reading, but still off the 57.2 seen in January. Perhaps of greater concern to officials, according to CoreLogic, house prices rose 2% in February, the largest monthly increase in 17 years, and home loan value grew by over 10% in January. The low-interest rates needed given the low price pressures and high unemployment may be spurring excess in the housing market. The Reserve Bank of New Zealand has recently had house prices included in its remit, and the Governor of the Bank of Canada has also expressed some initial concerns.

The dollar reached a new high against the Japanese yen since last August, near JPY106.75. An option for $510 mln at JPY106.85 may be the last hurdle ahead of JPY107.00. Initial support is around JPY106.40. The Australian dollar has stabilized after falling about 3.4% over the past two sessions. It held above $0.7700, but the bounce lost momentum around $0.7770, where options for A$2.2 bln expire today and a little above the 20-day moving average (~$0.7760). The PBOC set the dollar’s reference rate at CNY6.4754, a little softer than expected. The dollar was settled around CNY6.4583 ahead of the Lunar Holiday on February 10. It is trading near CNY6.4635 now. It has moved broadly sideways so far this year.

EuropeThe eurozone manufacturing PMI was revised higher from the preliminary reading of 57.7 after January’s 54.8. The final reading came in at 57.9 after Germany and France’s flash readings were revised higher, and both Italy and Spain’s reports were better than expected. Germany’s stands at 60.7, up from 57.1 in January, and the French reading is at 56.1, not the flash’s 55.0, and up from 51.6. Italy’s edged above expected to stand at 56.9 from 55.1 in January. Spain remains the laggard but returned above the 50 boom/bust level to 52.9, up from 49.3. The takeaway is that the European manufacturing sector has weathered the lockdowns better than last February and March. |

Eurozone Manufacturing Purchasing Managers Index (PMI), February 2021(see more posts on Eurozone Manufacturing Purchasing Managers Index, ) Source: investing.com - Click to enlarge |

Attention turns back to inflation, and the eurozone’s preliminary February report is due tomorrow. Italy has already reported its figures today. Prices fell 0.2% on the month for a 1.0% year-over-year increase. In January, Italy’s CPI fell by 0.9% for a 0.7% year-over-year increase. Spain’s figures were reported last week, and it may be one of the few eurozone members experiencing deflation (negative CPI). Its CPI fell by 0.6% month and -0.1% year-over-year. Officials pointed to the decline in electricity prices after January’s increase. Prices at hotels and restaurants rose less than last February. Germany’s states are reported now and will report the national figure before European markets closed. In most of the states, the year-over-year increase is larger than in January. The national figure is expected to rise by 0.5% for a 1.6% year-over-year increase, unchanged from January.

Like the eurozone, the UK’s manufacturing PMI was revised higher from the flash report. It stands at 55.1 in February, up from the 54.9 preliminary estimate and 54.1 in January. While the manufacturing sector is proving resilient, consumer borrowing less so. Net consumer credit fell by GBP2.4 bln in January, the fifth consecutive monthly decline, and leaving it almost 9% below year-ago levels. On the other hand, mortgage lending remained strong at GBP5.2 bln, and mortgage approvals remain strong. The market may be more sensitive to house prices, and tomorrow, Nationwide’s February figures are on tap. The week’s highlight is the budget on Wednesday, where more economic support will be provided while at the same time plans to begin bringing fiscal policy back under control are expected to be announced.

The euro has extended the pre-weekend decline to test the $1.2025 area that provided support on the last pullback (February 17-18). The market shied away from the $1.20-level of psychological importance, and it holds an expiring option for about 720 mln euros. The low was recorded early in Europe, and it appears to have brought in some buying. Resistance is seen near $1.21. Sterling is firm within its pre-weekend range. It was unable to reclaim the $1.40-handle despite two tries in Asia. The market has not given up on it, and another thrust looks likely. Beyond it, the $1.4050 area may provide the near-term cap.

America

It is as if the easy monetary or fiscal policy is the root of all the economic risks to hear some talking heads. Rising prices are laid at the feet of policymakers. This is to place all the pressure from the demand side, and the situation appears considerably more complicated. Consider oil, for example. OPEC has kept supply off the market, and this will change shortly, including the one million barrel a day unilateral cut by Saudi Arabia that extends to the end of this month. Russia and other producers were to continue to boost output.

Similarly, the shortage of chips is not a function of monetary or fiscal policy. It could be partly aggravated by the US trade policy that limited sales to Huawei and Semiconductor Manufacturing International Corporation (SMIC). It may be partly a function of the industry structure that gives Taiwan Semiconductor Manufacturing Company (TSMC) a virtual monopoly on the new generation of chips, the wafer of which is reportedly as thin as the length your fingernail grows in three seconds. Computer sales rose 13% last year, and the new 5G smartphones are said to use 30%-40% more chips than 4G. Another example is the near doubling of the cost of sending a 40-foot container from the US to China in the past year. It is a function of the sharp deterioration in the US trade imbalance. The price increase of oil, chips, and shipping seems transitory and not directly related to fiscal stimulus or the Fed’s purchases of bonds.

The US reports the final manufacturing PMI, construction spending, and the February ISM. However, investors are confident of a strong Q1 economic performance and continue to revise GDP estimates higher. Rather than the data, the market is more interested in Fed officials’ reaction function, and no fewer than five speak today. The week’s highlight will be Powell’s comments, which may be the last ahead of the conclusion of the FOMC meeting on March 17. Canada sees its February manufacturing PMI. It stood at 54.4 in January and 51.8 last February. Tomorrow, Canada reports Q4 GDP. It is expected to have risen by 7.2% at an annualized pace. Mexico’s manufacturing PMI was below 50 in January, and indeed at 43.0 was well below the 49.0 reading in January 2020. The Mexican economy was contracting before the pandemic struck. Mexico also reports January worker remittances. This has been an unexpectedly positive development for Mexico. Even if remittances also from December, they are expected to remain high. Consider that the monthly average for remittances was $3.38 bln in 2020, while the trade surplus averaged $2.87 bln a month.

The US dollar jumped from the three-year low near CAD1.2470 to almost CAD1.2750 ahead of the weekend. It is seeing those gains pared today. The first retracement target is near CAD1.2640. Consolidation is to the point as momentum traders have lost some conviction. The peso has fallen out of favor. The greenback jumped from around MXN20.35 in the middle of last week to almost MXN21.05 ahead of the weekend. It settled last month near MXN20.8550, and after falling to almost MXN20.69, it is back around MXN20.8350 in Europe.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,Currency Movement,Featured,inflation,newsletter,PMI,RBA