Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

Swiss FrancThe Euro has fallen by 0.06% to 1.0761 |

EUR/CHF and USD/CHF, January 21(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The S&P 500 and NASDAQ gapped higher yesterday to record-levels, and the reflation theme lifted Asia Pacific shares for the third session today. South Korea, Taiwan, and China led the advance. Europe’s Dow Jones Stoxx 600 gapped higher and is consolidating, seemingly waiting for fresh directional clues from the US, where a small higher opening is anticipated. The US 10-year yield is steady around 1.08%, while European yields are a little softer. The US dollar is lower against nearly all the major and emerging market currencies today. Sterling, the Norwegian krone, and the New Zealand dollar are jostling for the lead with around a 0.6% gain. The yen and Canadian dollar are laggards. The JP Morgan Emerging Market Currency Index is posting small gains as its advance stretches into the fourth consecutive session. Gold extended its bounce off the week’s low near $1805 and made it to around $1875 today before steadying. The $1880 area is the halfway mark of the recent leg lower from near $1960. Oil prices are softer but at the upper end of their recent ranges. March WTI stalled in front of $54 a barrel last week and yesterday and has backed off today to around $52.75. API estimated a small (2.5 mln barrel) increase in US crude inventory, which, if confirmed by the EIA later today, would be the first build of the year. |

FX Performance, January 21 - Click to enlarge |

Asia Pacific

The Bank of Japan stood pat as widely expected. It shaved its GDP forecast for the fiscal year, ending in March to -5.6% from -5.5%. However, it lifted the forecast for FY21 to 3.9% from 3.6%, and the FY22 GFP forecast was raised to 1.8% from 1.6%. CPI is expected to fall by 0.5% in the current fiscal year compared with a 0.6% decline previously anticipated. Inflation is expected to rise to 0.5% in FY21 (from 0.4% previously) while FY22 was left at 0.7%. The takeaway is the pattern, which will likely be seen by other officials, is the near-term pessimism but the medium-term confidence encouraged by the vaccine.

Separately, Japan reported December trade figures. For the first time in two years, exports rose on a year-over-year basis, helped by strong Chinese demand. The trade surplus of JPY751 bln was smaller than expected because exports were a little less than expected and imports were not quite as weak. The average trade surplus in 2020 was JPY56.2 bln. It was the first surplus recorded on a 12-month rolling basis since October 2018. Exports rose by 2.0% in the year through December, and imports fell by 11.6%. Elsewhere on trade, and following on the heels of a strong export order report by Taiwan, South Korea reported its trade figures for the first 20-days of January. Exports rose 10.6% compared with a 7.9% gain last month. Imports also edged higher.

Last month, Australia grew 50k jobs, spot-on forecasts, though off the 90k growth seen in November. The unemployment rate slipped to 6.6% from 6.8% despite the tick-up in the participation rate to 66.2%(from 66.1%). Full-time positions rose by 35.7k, down from 84.2k., while part-time positions rose by 14.3k after a 5.8k gain in November. The Reserve Bank of Australia meets on February 1. No change in the stance is expected.

The dollar had appeared to forge a shelf around JPY103.50 but slipped through it yesterday, and the losses were extended today to a little through JPY103.35. There is an option for $940 mln at JPY103.25 that expires today, which is also roughly the (61.8%) retracement of the bounce off the January 6 low (~JPY102.60). The Australian dollar is higher for the third consecutive session. The high since April 2018 was set on January 6 near $0.7820. The Aussie is knocking on the $0.7780 area in the European morning. Support is seen near $0.7740. The PBOC set the dollar’s reference rate at CNY6.4696. The Bloomberg survey of bank models put it at CNY6.4674. The dollar is heavy for the third-straight session but remains within the consolidative range seen recently (~CNY6.45-CNY6.50). The PBOC left the Loan Prime Rates unchanged for the ninth month.

Europe

It is about central banks today. Norway’s central bank meeting outcome is already known. It left policy on hold as widely expected, but it is still on track to raise rates in H1 2022. Rather than pursue the unorthodox monetary policy, which has frankly become more standard, it tapped one of the largest sovereign wealth funds in the world. That said, its policy rate (zero), when adjusted for inflation (~1.4%), is among the most negative among high-income countries.

South Africa’s Reserve Bank is expected to have left rates steady at 3.5%. Note that December CPI was 3.1% year-over-year, and the core rate was at 3.3%. Turkey’s central bank also left its one-week deposit rate unchanged at 17.00%. Despite Prime Minister Erdogan’s pressure, the shift to a more orthodox monetary stance has helped stabilize the exchange rate. The lira has risen by about 0.5% so far in 2021, making it among the better performing emerging market currencies. The dollar spiked higher on the announcement, but the greenback met sellers near TRY7.42 and quickly drove it to new session lows (below TRY7.38)

The ECB takes center stage. However, there is not much to be seen or done here now. No fresh policy initiatives are likely. With the lockdowns and social restrictions being extended, the toll on the households and businesses is significant. Lagarde is likely to play up the near-term downside risks, but she may also underscore the medium-term better outlook. Uncertainty over the US election and Brexit has been resolved. The EU’s budget and Recovery Fund are being approved and can be operational shortly. The ECB’s Pandemic Emergency Purchase Program has been consistently buying between 57 and 68 bln euros a month of securities. We see no compelling reason to expect this to change any time soon.

The euro is trading within yesterday’s range (~$1.2075-$1.2160), which is more or less the range since Monday. We have been anticipating the pullback after the $1.2350 level was approached on January 6. What level does the euro need to rise above to indicate the underlying uptrend has resumed? A move to $1.22 would be a warning, but it probably needs to rise above the $1.2240 area to boost chances that the corrective low is in place. For its part, sterling is at new highs since April 2018, having approached $1.3750 in the European morning. The thrust higher appears to have exhausted the bulls. Initial support is seen in the $1.3680-$1.3700 area. The euro is at its lowest level against sterling (~GBP0.8830) since last May.

| America

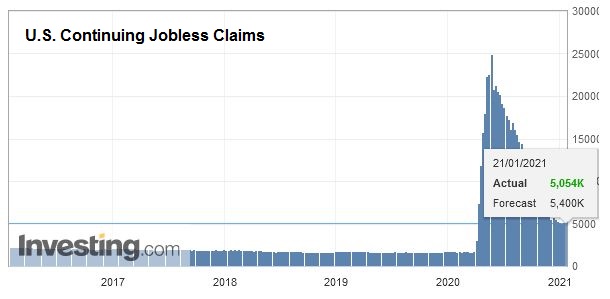

The Bank of Canada left its target rate at 25 bp yesterday. Some, including ourselves, thought there was a chance of a small cut following comments from the Governor. When it was not delivered, the Canadian dollar extended its gains and reached its best level since April 2018. The BoC seemed more confident of the medium-term and hinted that as its confidence grew in the recovery, it would adjust its bond-buying, which was left at C$4 bln a week. This could happen in Q3. Separately, Brazil’s central bank left the Selic Rate at 2%, as widely anticipated. However, it dropped its pledge to keep rates lows for the foreseeable future, which is seen as a signal that it could lift rates later this year. Three new data points will be provided by the US today. December housing starts are expected to have remained firm. Residential investment and housing remain strong sectors of the US economy. The Philadelphia Fed survey offers an early look into this month’s activity. A small gain is expected (~11.8) after the December series was revised to 9.1 from 11.1. Recall that the Empire State manufacturing survey for January disappointed by slipping to 3.5 from 4.9. A gain had been forecast. Lastly, the US reports weekly jobless claims, and the week covers the period in which the national jobs survey is conducted. Recall that last week’s report, for the week through January 8, saw an unexpectedly large increase of 181k to 965k, the highest since August. A modest decline is expected (Bloomberg’s survey median forecast is for 935k). Canada has a light calendar today and reports November retail sales tomorrow. Mexico reports December unemployment figures today. A small decline to 4.28% is expected after November’s 4.40% rate. |

U.S. Continuing Jobless Claims, January 21 2021 Source: investing.com - Click to enlarge |

The US dollar has been unable to distance itself from the CAD1.26 level approached yesterday. There is a $555 mln option struck there that expires today, and a battle could be waged over that area today. A break signals a test on the CAD1.2550 area, where another option for about $610 mln is struck and also expires today. The next important chart area is closer to CAD1.25. The Mexican peso is also edging higher, leaving the greenback at its lowest level (~MXN19.55) since last March when it saw almost MXN19.15. Initial resistance is seen near MXN19.60.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,central-banks,Currency Movement,ECB,Featured,newsletter,South Africa,Trade,Turkey