Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

Swiss FrancThe Euro has risen by 0.13% to 1.0756 |

EUR/CHF and USD/CHF, December 10(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: US threats to break-up Facebook and the stalled stimulus talks spurred profit-taking in US shares yesterday and is dampening enthusiasm today. The MSCI Asia Pacific Index fell for the third time this week, and Europe’s Dow Jones Stoxx 600 is little changed. US shares are trading with a firmer bias now. Ahead of the ECB meeting, new record lows in yields are being seen in Europe, and Italy’s 5-year yield turned negative for the first time yesterday. Spain auctioned 10-year bonds today with a negative yield for the first time, and some buyers at the three-month bill auction in Australia also will receive a negative yield for the first time. The US 10-year benchmark is hovering around 0.92%. The dollar is weaker against most of the major currencies. The two notable exceptions are the yen and sterling. The Antipodean currencies are leading today’s move against the greenback. Emerging market currencies are more mixed, with eastern and central Europe doing best. The JP Morgan Emerging Market Currency Index is a little weaker for what could be the second consecutive losing session. Gold remains on the defensive after falling by more than $30 an ounce yesterday, unable to rise above $1845, and pinned near the lows (around $1830). Crude oil, on the other hand, shrugged off a 15 mln barrel surge in US inventories, the most in eight months, and February WTI is hovering just below $46 a barrel |

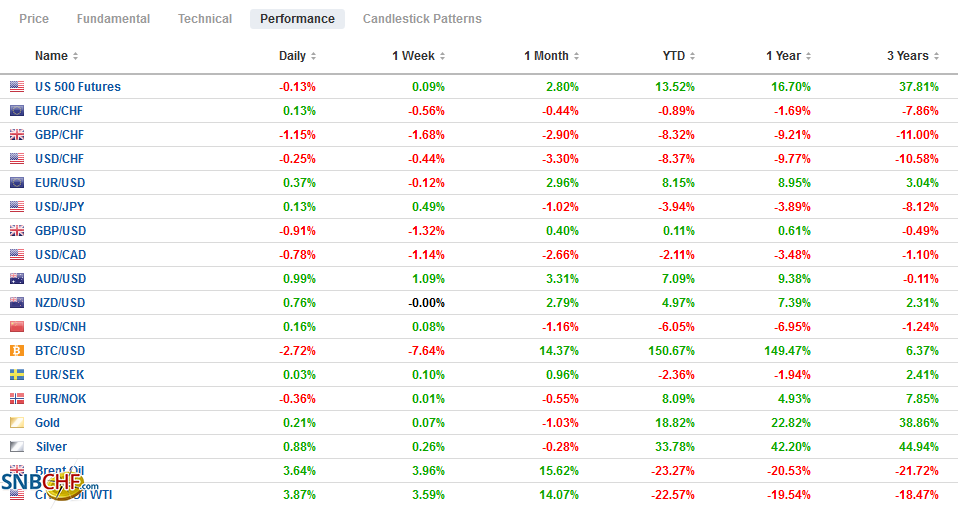

FX Performance, December 10 - Click to enlarge |

Asia Pacific

China is retaliating against the US by sanctioning diplomatic passports and revoking visa-free travel to Hong Kong and Macau. Starting tomorrow, it will also begin collecting extra duties on Australian wine, on top of the temporary anti-dumping duties announced last month. Australia, and to a less extent, Canada are being punished by China for essentially being US allies.

Japan reported producer prices were flat in November and off 2.2% year-over-year. Producer prices have not been positive in Japan since February. They rose by 0.9% in December 2019 and 1.4% in December 2018. Separately, note the divergence in estimates for growth. The government is optimistic that with the latest stimulus efforts, the economy can grow by more than 3% in the next fiscal year that begins April 1. Most private forecasts are for around 1%. Lastly, we note that the weekly MOF portfolio flow data shows Japanese investors have stepped up their purchases of foreign bonds. Last week was the fourth week of the past five that more than JPY1 trillion of foreign bonds were bought. The five-week average of nearly JPY1.2 trillion is the highest since early March, which itself was a four-year high.

The dollar reached a six-day high against the Japanese yen just below JPY104.60 in late Asian turnover. Initial support is seen in the JPYY104.20-JPY104.30 area. An option for about $655 mln at JPY104.90 may stand in the way of a test on JPY105, though the high for the past two weeks was about JPY104.75. The Australian stock market snapped a seven-day advance, and the 10-year yield fell back below 1%, but the Australian dollar is making new highs and drawing closer to $0.7500, where a A$572 mln option is struck that expires today. The Aussie settled at $0.7425 last week, and this would be the sixth consecutive weekly advance. Initial support is now seen near $0.7450. The PBOC set the dollar’s reference rate at CNY6.5476, in line with expectations. The dollar is a little firmer against the offshore yuan, dipping below CNH6.50 briefly yesterday, while the greenback is a little softer against the onshore yuan.

Europe

Some modest profit-taking was seen ahead of the ECB meeting, and a five-day low was recorded yesterday. Still, the euro remains above the upper end of the $1.1600-$1.2000 range that dominated from mid-July through the end of November. The focus is squarely on today’s ECB meeting, where the market feels fairly confident about the outcome. The ECB will extend and expand its emergency bond-buying program (PEPP). It is also widely expected to announce a new targeted longer-term refinancing operation (three-year loans at attractive rates). It could tweak some other settings, but the focus will be on the size of the increase in PEPP resources and how long it is extended beyond the middle of next year. Most are looking for around a 500 bln euro increase and the program’s extension until the end of next year. The risk is asymmetrically in favor of more for longer.

The ECB staff will update their forecasts, and ideally, provide the backdrop for the policy changes. The action, which was pre-committed to, must be because the situation has deteriorated more or quicker than expected. The emphasis is on the near-term risks that are materializing, not on the potential upside risks next year when the vaccine is available. The foreign exchange market will be sensitive to any comments, or indeed, lack thereof, about the euro. Besides the truism that the exchange rate feeds into the models of the economy and inflation, there is little that Lagarde will likely say. She will be prepared to be peppered with comments, but she is likely to give little away, if for no other reason than there is little to say. The ECB, like the Federal Reserve, does not have a currency policy per se. That said, ideally, the real broad exchange rate moves in the direction of policy. Otherwise, official efforts are diluted.

The dinner for UK Prime Minister Johnson and EC President von der Leyen failed to resolve the dispute, but the outcome was to extend talks through the weekend. The same three vexing issues remain; fishing rights, governance, fair competition, or “level playing field.” The EU has shown remarkable cohesion, and this appears to have also frustrated Johnson’s strategy to try to exploit potential fissures. German Chancellor Merkel, who appears to have found a compromise with Poland and Hungary to get the EU budget and Recovery Fund moving forward, took a hard line, warning that a dispute over what happens if/when the UK rules diverge from the EU could also prevent an agreement. Moreover, the UK’s unilateral defection from the tariffs levied in retaliation for Boeing’s improper US subsidies further undermined trust, with some officials seeing it as a betrayal.

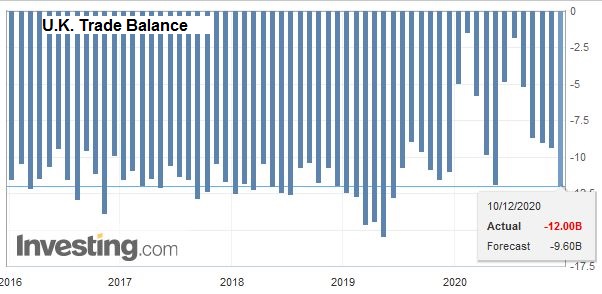

| The UK economy grew by 0.4% in October. While it is better than expected, it shows a marked slowdown from 1.1% in September, and with additional social restrictions, last month’s GDP may have contracted. Still, October was lifted by strong industrial output (1.3% vs. 0.5% in September), but services and construction slowed markedly, and net exports were a larger draw. The overall trade balance swung sharply back into deficit (GBP1.74 bln) from a GBP613 mln surplus in September. It is the first deficit since March. |

U.K. Trade Balance, October 2020(see more posts on u-k-trade-balance, ) Source: investing.com - Click to enlarge |

The euro is trading in about a third of a cent range above $1.2075 today. It is well inside yesterday’s range (~$1.2060-$1.2145) ahead of the ECB meeting. The initial risk seems to be on the downside, and initial support is seen in the $1.2060-$1.2080 area. There are a couple of expiring options to note. The first is for almost 690 mln euros at $1.2050, and the other is struck at $1.20 for about 570 mln euros. Sterling, which reached almost $1.3540 at the end of last week, is straddling the $1.33-area in the European morning. A break of $1.3290 could spur a test on the week’s low near $1.3225, and the $1.3200 area corresponds to the halfway point of the rally from last month’s low near $1.2855. The euro has swung between about GBP0.8980 to around GBP0.9140 this week and is firm today near session highs around GBP0.9100.

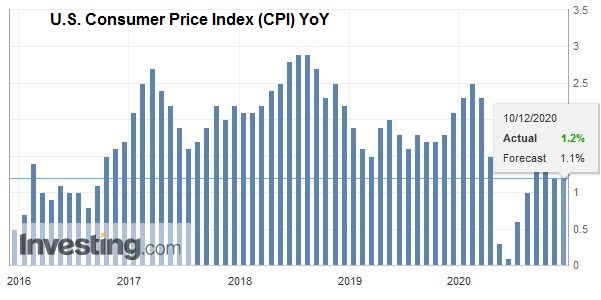

AmericaThe US Senate is expected to pass a one-week continuing resolution, as the House has already done, to buy negotiators an extra week to find a compromise on spending authorization and new stimulus measures. The sticking points now are reportedly shielding companies from Covid-related liability and aid to state and local governments. A possible workaround on the liability issue will be formally proposed by the bipartisan group today. Separately, the US reports weekly initial jobless claims (many look for a rise) and November CPI. |

U.S. Consumer Price Index (CPI) YoY, November 2020(see more posts on U.S. Consumer Price Index, ) Source: investing.com - Click to enlarge |

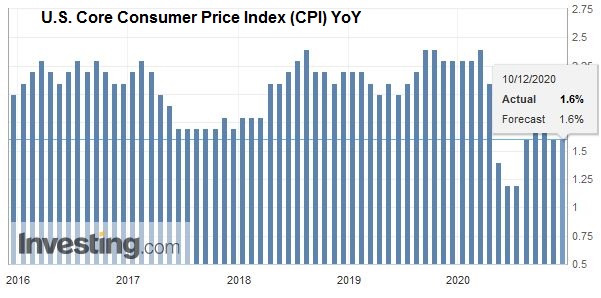

| While the headline and core rates may rise by 0.1% on the month, the year-over-year rates may tick down to 1.1% and 1.5%, respectively, due to the base effect. Many observers are playing up the risk of resurging inflation next year. Most arguments seem to be based on 1) pent-up demand post-Covid, 2) rising commodity prices, and 3) expansion of money supply. Of course, there are some structural arguments, too, like shifting demographics and the weakening of globalization. |

U.S. Core Consumer Price Index (CPI) YoY, November 2020(see more posts on U.S. Core Consumer Price Index, ) Source: investing.com - Click to enlarge |

The Bank of Canada stood pat yesterday, as widely expected. Its bond-buying (C$4 bln a week) will continue until the economic recovery is well underway. Its low-interest rate (0.25 bp) stance will remain until the economic slack is absorbed, and it is on a sustainable path to its 2% inflation target. It does not see the latter happening until 2023. The Bank of Canada did not address the exchange rate much. It did recognize the rise in commodities and the broad-based US dollar decline.

Mexico reported its first decline in headline CPI since July. It stood at 3.33% in November, down from 4.09% in October. The extended period of shopping discounts, a fall in food prices and gasoline drove the decline. Core prices also fell. Banxico meets next week, but the majority of the five-person board will likely want to see if the decline in prices is transitory. Last month, the Deputy Governor dissented in favor of a cut, while the other four voted to pause after 11 consecutive cuts. Brazil’s central bank kept the Selic rate at the record low 2% but seemed to caution that inflation expectations are rising. This strengthens views that Brazil is at the end of its easing cycle.

The US dollar continues to consolidate its recent losses against the Canadian dollar and remains trapped in the trough. It has struggled to rise above CAD1.2830 this week and has found support near CAD1.2770. The intraday technicals warn against playing for a sustained break today. Similarly, the greenback is in a MXN19.70-MXN20.00 range. The entire range was explored yesterday, and today it is chopping around the middle of the range around MXN19.85. It does not appear to be going anywhere quickly.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,Brexit,China,Currency Movement,ECB,Featured,newsletter,U.K.