Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

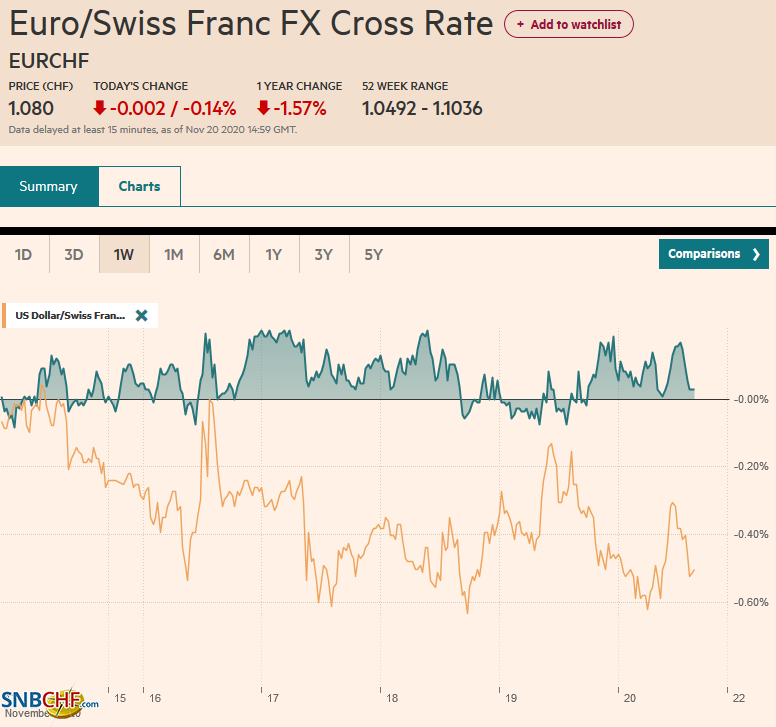

Swiss FrancThe Euro has fallen by 0.14% to 1.080 |

EUR/CHF and USD/CHF, November 20(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: News that the stimulus talks between the House Democrats and Senate Republicans was the excuse traders were looking for to extend the US equity gains yesterday, but shortly after the close, confirmation that Treasury was not going to agree to extend several Fed facilities sent stocks reeling. However, the MSCI Asia Pacific Index showed little reaction, and after snapping a 13-day advance yesterday, returned to its winning ways today. The Nikkei, Taiwan, and Thailand were exceptions. European shares are advancing today, and the Dow Jones Stoxx 600 is recouping around three-quarters of yesterday’s 0.75% loss. Barring a strong reversal, it will extend its rally for a third consecutive week for a little more than 13%. US stocks are narrowly mixed, and the S&P 500 is off by about 0.1%, and the NASDAQ is up roughly 0.6% for the week coming into today. Benchmark 10-year yields are a little changed across the board. The 10-year Treasury yield near 0.84%, off seven basis points this week. European and the Asia Pacific yields are slightly softer on the day and around 2-3 bp lower on the week. South African bonds are little changed on the session and for the week ahead of the rating decisions by S&P (possible cut the outlook of its rating three steps below investment grade) and Moody’s (expected unchanged rating, one notch below investment grade). The US dollar is mixed. The dollar-bloc currencies are firmer, while the euro and Swedish krona are trading a little lower. On the week, the greenback has depreciated against all the majors. Most emerging market currencies are trading higher today. Still, the Turkish lira is seeing some profit-taking after yesterday’s advance following the central bank’s rate hike and signal of a return to more orthodox policies. The yuan has risen about 0.5% this week, its third consecutive weekly advance. The JP Morgan Emerging Market Currency Index is up nearly 1% this week, also its third weekly increase. Gold is trying to snap a four-day slide today. It is consolidating quietly today and appears in a new near-term range of $1850-$1875. Oil is steady, and the January WTI contract is putting its final touches on the third consecutive weekly advance, during which time it has rallied about 15% to around $42 a barrel. |

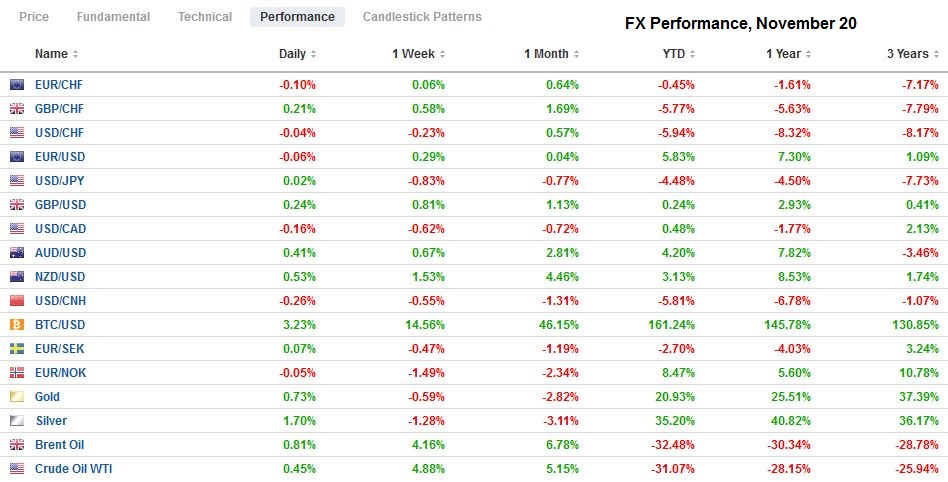

FX Performance, November 20 - Click to enlarge |

| Asia Pacific

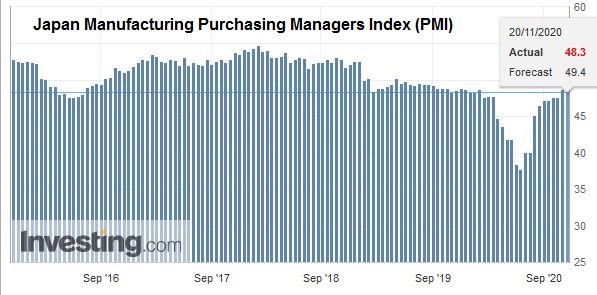

News from Japan was not good. Deflationary pressures deepened as last year’s sales tax increase drops out of the year-over-year comparison, and the flash PMI showed a weaker economy. Headline October CPI was -0.4% year-over-year, the weakest in four years. The core rate, which excludes fresh food, was off 0.7% year-over-year, the most in nine years. Gasoline and electricity prices fell, and government efforts to boost internal tourism lowered the price of accommodations. The preliminary November PMI readings pushed further below the 50 boom/bust with manufacturing at 48.3 (from 48.7), services 47.0 (from 47.7), and the composite to 47.0 (from 48.0). The government is preparing another supplement budget. |

Japan Manufacturing Purchasing Managers Index (PMI), November 2020(see more posts on Japan Manufacturing PMI, ) Source: investing.com - Click to enlarge |

China launched a yuan-denominated futures contract. It will be helpful for local producers and consumers. Still, it does not do much for the yuan’s internationalization, any more than an oil futures contract did or what a yen-denominated rubber contract does for Japan. SWIFT figures out earlier this week showed the yuan use on its platform m slipped to 1.66% last month from 1.91% in September. It had a 1.94% share at the end of last year. Instead, the integration of its capital markets is the more important track now. The Trump administration is thought to be pushing ahead with efforts to delist Chinese companies who refuse to subject themselves to an audit. Separately, and as widely expected, the one and five-year Loan Prime Rates were left unchanged at 3.85% and 4.65%, respectively.

The dollar is in a narrow range against the yen today, holding within less than a fifth of a yen above JPY103.75. An option for roughly $680 mln struck there expires today, and another for $970 mln at JPY104 also will be cut. The greenback has eased against the yen for the past six sessions and is trying to break that streak today. The Australian dollar is little changed today, and around $0.7290 is up about 0.25% for the week, its third weekly advance. This week, it has been in about a 40-tick range on both sides of $0.7300. The PBOC set the yuan’s reference rate at CNY6.5786, which was a little stronger than the average forecast in the Bloomberg survey. The dollar surrendered about half of the 0.4% gain it recorded over the past two sessions and is finishing the week about 0.5% lower than it began.

| Europe

UK October retail sales surprised to the upside. Including gasoline, retail sales were expected to have fallen by 0.3% but instead rose 1.2% after a revised 1.4% gain in September (initially 1.5%). Excluding “petrol,” economists had expected a flat report. However, UK consumers were busy and boosting sales by 1.3%. The September series was revised to 1.5% from 1.6%. However, the new closures and restrictions make these data points less relevant. The Bank of England expects the economy will contract around 2% this quarter. |

U.K. Retail Sales YoY, October 2020(see more posts on U.K. Retail Sales, ) Source: investing.com - Click to enlarge |

| The EC continues to fight a two-front battle. Trade talks with the UK are extending into next week. While there has been little tangible process, the word being sent privately is that some progress is taking place. On the other front, Hungary and Poland refuse to sanction linking aid to adherence to the rule of law conditions that have been attached. It seems rather naive to think that any member’s interests can be rode roughshod over when the decision requires unanimity. While the rule of law is indeed a worthy goal, there must be other ways for the EC to enforce its will. |

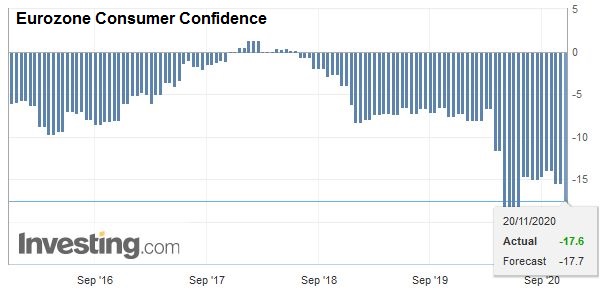

Eurozone Consumer Confidence, November 2020(see more posts on Eurozone Consumer Confidence, ) Source: investing.com - Click to enlarge |

The euro has traded between roughly $1.1815 and $1.1895 this week. It is trading a little softer after again stalling in front of $1.19. There is an option for around 765 mln euro at $1.1850 that expires today. Support near $1.1840 may be sufficient today ahead of the weekend. The euro settled last week around $1.1835. Sterling is slightly firmer, but it is in a half-cent range, mostly above $1.3250. The high this week and last was a little above $1.3310. Sterling finished last week near $1.3180. This would be the third consecutive weekly gain for sterling. The euro is losing about 0.5% against sterling this week, which roughly matches last week’s decline as well.

America

For those following the issue, it was clear that many Republican Senators and Treasury Secretary Mnuchin were opposed to extending the Fed’s special lending facilities that expire at the end of the year. The argument is that the emergency is over, and the light use of the programs demonstrated that they were not needed, and the funds earmarked could be better used. The Federal Reserve argued in favor of extending the programs, which serve as a backstop, and their mere presence helps facilitate orderly market conditions. Late yesterday, it became official. Five of the nine facilities will end this year, including the primary and secondary corporate bond program, the local government, term ABS, and the Main Street facilities. The other programs (commercial paper, primary dealer, money market, and Payroll Protection) will be extended for 90 days. The Federal Reserve is to return the unused CARES Act funds (roughly $260 bln of the $455 bln) back to Congress, where they may help finance the next stimulus package.

While the US and Mexico have light economic calendars today, Canada reports September retail sales figures. The headline is expected to rise by 0.2% after a 0.4% gain in August. The increase is anticipated to stem from the higher auto sales, and without which Canadian retail sales may be flat 0.5% in August). Canada’s economic releases for the rest of the month are not market-movers, but the investors are expected a fiscal update in the coming weeks. Ahead of it, Moody’s affirmed its Aaa rating for Canada yesterday. Recall Fitch had cut its rating to AA- in July partly due to the deterioration of Canada’s fiscal position.

The US dollar is little changed against the Canadian dollar, around CAD1.3060. It is sandwiched between two expiring options today: an $880 mln option at CAD1.30 and a $1.1 bln option at CAD1.31. So far, today is the first session since the middle of last week that the greenback has not traded above CAD1.31. It has not been below CAD1.30 since November 10. The US dollar has not traded below CAD1.3035 this week. The Mexican peso is firm and is closing in on its third consecutive weekly gain against the US dollar. The greenback settled near MXN20.4075 last week and almost MXN21.18 at the end of October. The dollar’s low for the week was set yesterday near MXN20.11, which may be challenged today. Last week’s low was nearer MXN20.03. Since February, it has not traded below MXN20 but looks poised to do so near-term, even if not today.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,Brexit,Canada,China,Currency Movement,Featured,federal-reserve,Japan,newsletter,South Africa,U.K.