Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

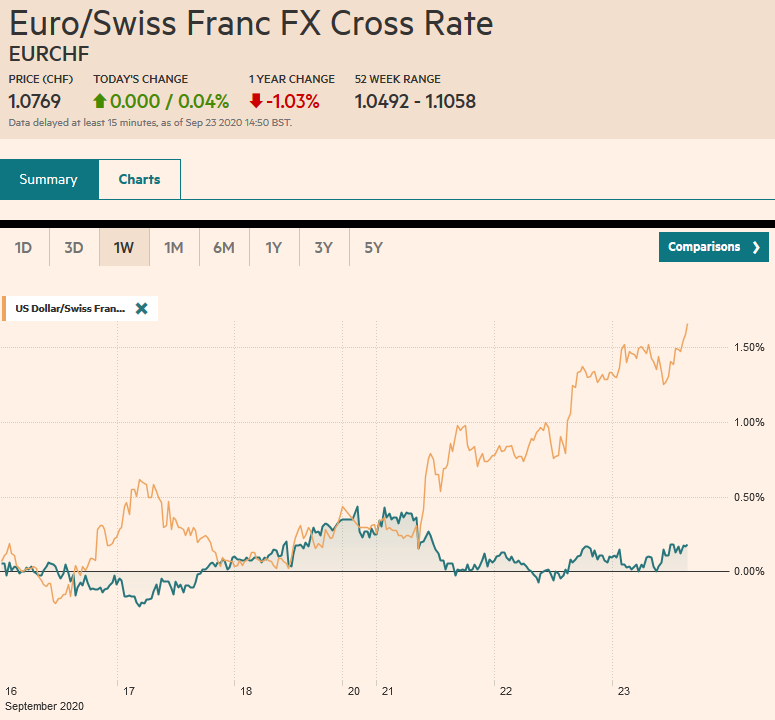

Swiss FrancThe Euro has risen by 0.04% to 1.0769 |

EUR/CHF and USD/CHF, September 23(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: A more stable tone is evident in the capital markets after the S&P 500, and NASDAQ rose more than one percent yesterday. Japan returned from a two-day holiday, and local shares slipped fractionally, while China, Hong Kong, South Korea, and Australian shares rallied. India and Taiwan fell. The Dow Jones Stoxx 600 is up around 1.5% near midday in Europe, its biggest gain in two weeks. US shares are extending yesterday’s gains. Soft preliminary PMI readings are helping to support the debt market, where benchmark 10-year yields are off 1-2 bp in Europe. The US 10-year is little changed near 67 bp. The euro is recovering from two-month lows near $1.1670, and most of the major currencies are little changed, and the Antipodean currencies are paring earlier losses. Gold’s losses were extended to around $1873 but it is stabilizing in the European morning. Last month’s low was near $1863. November light sweet crude futures are consolidating around $40 a barrel. |

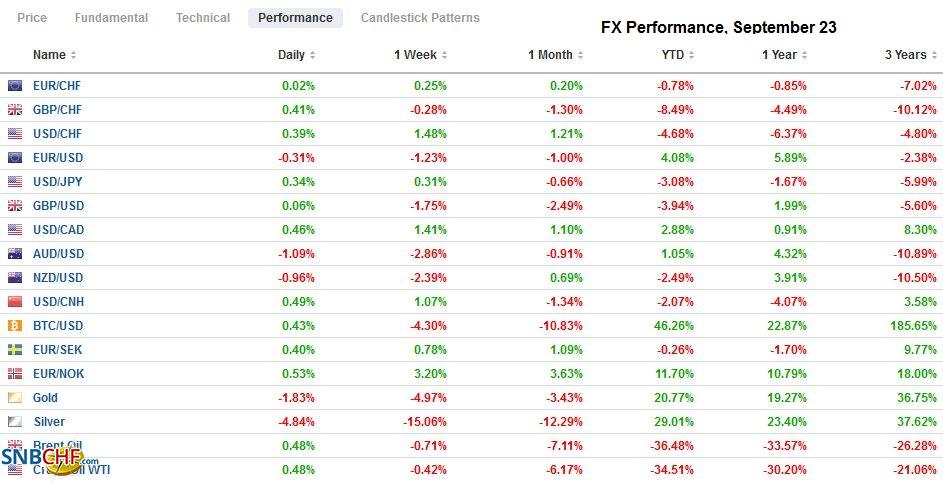

FX Performance, September 23 - Click to enlarge |

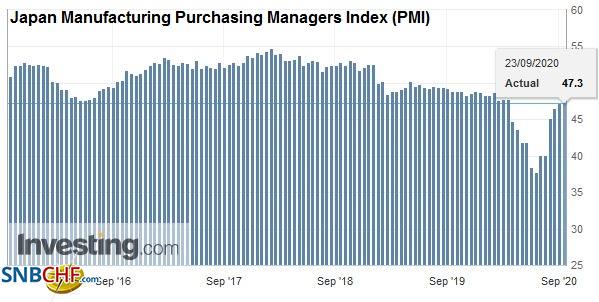

Asia PacificJapan’s preliminary September PMI was little changed from October, and the composite remained below the 50 boom/bust level. The manufacturing PMI edged to 47.3 from 47.2, and the service PMI rose to 45.6 from 45.0. This led to the composite to recovery to 45.5 from 45.2. This report is not inspiring optimism about the Q3 recovery in growth after contracting for the past three quarters. However, the All-Industries Activity Index rose by an expected 1.3%. A second supplemental budget by the new Suga government remains a distinct possibility. |

Japan Manufacturing Purchasing Managers Index (PMI), September 2020(see more posts on Japan Manufacturing PMI, ) Source: investing.com - Click to enlarge |

Australia’s preliminary PMI was better, and the composite rose back above 50. The 50.5 composite reading follows a 49.4 in August. The manufacturing PMI rose to 55.5 from 53.6, and the service PMI recovered to 50.0 from 49.0. Although we had the RBA cutting rates again last month and they did not, speculation is picking up that it could ease policy as early as the October 5 meeting. The Reserve Bank of New Zealand met and stood pat. No one expected a change ahead of the October 17 election, but additional measures are likely, and the next meeting is November 11.

Returning Tokyo traders bid the dollar to a six-day high near JPY105.20 before running out of steam. It is consolidating in a narrow range, mostly above JPY104.90. Note that there are nearly a billion in options rolling off today that are struck between JPY105.00 and JPY105.15. Tomorrow there are more than a billion dollar options expiring at JPY104 and JPY105. The Australian dollar’s losses extended into a fourth session. Last month’s low was near $0.7075. However, the downside momentum appears to be stalling, and the intraday technicals suggest the likelihood of a recovery attempt. The PBOC again set the dollar’s reference rate stronger than the bank models projected. Many see this as a sign that officials are resisting further yuan appreciation now after an eight-week advance. The market respects the signal and the dollar’s gain today is the fourth in the past five sessions.

EuropeThe preliminary German PMI was mixed. The manufacturing improved to 56.6 from 52.2. That is the highest reading since July 2018. On the other hand, the services PMI weakened to 49.1 from 52.5. Most economists had expected a small increase. The composite slipped to 53.7 from 54.4. Separately, reports suggest that Merkel is resisting efforts to completely ban Huawei, setting up a possible new confrontation with the US. |

Germany Manufacturing Purchasing Managers Index (PMI), September 2020(see more posts on Germany Manufacturing PMI, ) Source: investing.com - Click to enlarge |

| The French PMI showed a similar pattern to the German report, but a bit worse. The manufacturing PMI did recover from 49.8 top 50.9, which was a bit better than expected. However, the service PMI fell to 47.5 from 51.5. The median forecast in the Bloomberg survey was for an unchanged reading. The net result was that the composite fell back below 50 to 48.5 (from 51.6).

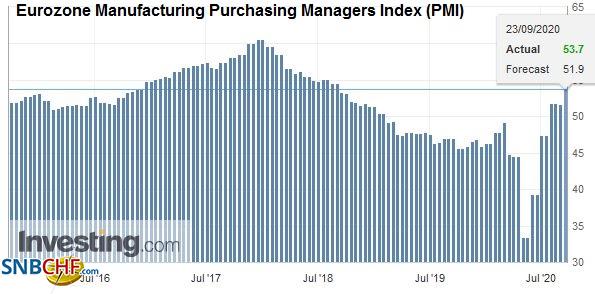

The EMU aggregate manufacturing PMI rose to 53.7 from 51.7, |

Eurozone Manufacturing Purchasing Managers Index (PMI), September 2020(see more posts on Eurozone Manufacturing PMI, ) Source: investing.com - Click to enlarge |

| while the service PMI fell to a three-month low of 47.6 from 50.5. |

Eurozone Services Purchasing Managers Index (PMI), September 2020(see more posts on Eurozone Services PMI, ) Source: investing.com - Click to enlarge |

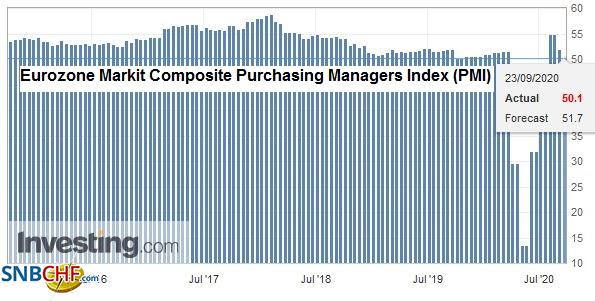

| The composite fell to almost the 50 boom/bust level (50.1) from 51.9. The implication is that the periphery also saw weakness in services, and the composite readings of Italy and Spain likely remained below 50. |

Eurozone Markit Composite Purchasing Managers Index (PMI), September 2020(see more posts on Eurozone Markit Composite PMI, ) Source: investing.com - Click to enlarge |

| In the UK, both the manufacturing and service PMI eased. The former slipped to 54.3 from 55.2, which was a little better than the Bloomberg survey projected. |

U.K. Manufacturing Purchasing Managers Index (PMI), September 2020(see more posts on U.K. Manufacturing PMI, ) Source: investing.com - Click to enlarge |

| The latter fell to 55.1 from 58.8, which was a bit worse than expected. The composite now stands at 55.7, its lowest level since June. Note that BOE Governor Bailey played down negative interest rates, the market pushed its expectations out until May from late Q1 21, and many still expect the BOE to ease via rates and asset purchases as early as the November 5 MPC meeting. Reports suggest that a new plan to subsidize wages is being considered. The current furlough effort is set to expire at the end of next month. |

U.K. Services Purchasing Managers Index (PMI), September 2020(see more posts on U.K. Services PMI, ) Source: investing.com - Click to enlarge |

| The euro is recovering in European activity back above the $1.1700 area, which had been the lower end of the recent trading range. There appears to be potential for additional gains in the North American session today, but the $1.1750 area may hamper stronger gains. After the quarter-end next week, many expect the focus to shift to the uncertainty around the US election. Sterling fell to nearly two-month lows near $1.2675 before finding a good bid in the European morning and has managed to resurface above the 200-day moving average (~$1.2725). The near-term potential extends toward $1.2800. |

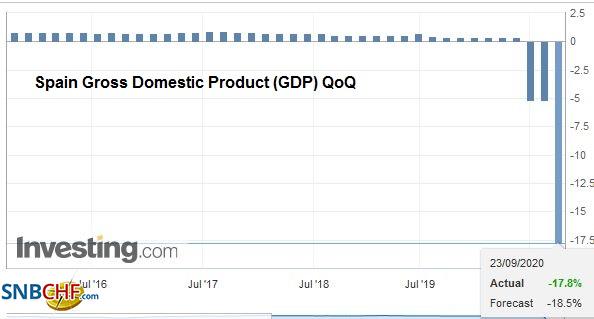

Spain Gross Domestic Product (GDP) QoQ, Q2 2020(see more posts on Spain Gross Domestic Product, ) Source: investing.com - Click to enlarge |

America

The House of Representatives passed stopgap funding to avert a US government shutdown on October 1. Funding is extended until December 11. The bill also includes aid for farmers and food assistance. The Senate will take up the measure and has a week to approve it. Separately, reports suggest that Beijing is objecting to the TikTok re-org than the US is foisting. Be on the watch for an FDA announcement that has been hinted at in the press that will pose another hurdle getting a vaccine out before the US election in early November.

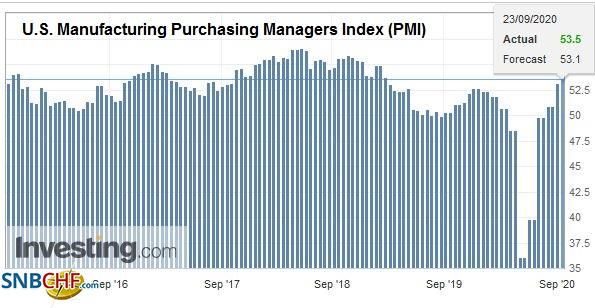

| The US preliminary PMI is expected to follow the European pattern of a continued recovery in the manufacturing sector and some softness in services. The median forecasts in the Bloomberg survey see the manufacturing PMI rising to 53.5 from 53.1, while the services PMI slips to 54.5 from 55.0. Meanwhile, no fewer than eight Fed officials speak today, including Chair Powell again before Congress. In Canada, the new Parliament session begins, and the government is expected to unveil new fiscal initiatives. Mexico reports July retail sales, and another substantial monthly gain is expected. |

U.S. Manufacturing Purchasing Managers Index (PMI), September 2020(see more posts on U.S. Manufacturing PMI, ) Source: investing.com - Click to enlarge |

Thomas Edison is once said to have quipped that he did not fail but found 1000 ways it did not work. It is in that spirit that we looked at currency expressions of equity opinions. The other major caveat is to appreciate that the correlations between currencies and equities are not stable. We looked at 60-day correlations on value, for purely directional, and percentage change to see if the returns are correlated between the S&P 500 and a few currency pairs. The yen may be the most popular guess, but the correlation on both scores do not stand out. The Australian dollar and the Mexican peso are also often picked, but there are better. Many strategists like the yen against the Norwegian krone and for a good reason. On a percentage change basis, the 60-day correlation is -0.57. Earlier this month is rose above -0.50 for the first time this year. On a directional, the correlation is- 0.92, among the most extreme in a decade. There may be more slippage in implementation as one often has to pay the spread twice. The Canadian dollar quantitatively virtually matches the yen-krone cross and more efficiently executed.

The US dollar is holding just inside yesterday’s range against the Canadian dollar. Immediate resistance is in the CAD1.3350-CAD1.3360 area. Overcoming it would target the CAD1.3400 area. Stabilizing risk appetites may help the Loonie stabilize. Support is seen in the CAD1.3280 area. The greenback is approaching MXN22.00, which it has not been above since late August. It is the fourth consecutive day the dollar is advancing against the peso. Above MXN22.00, the next target is MXN22.12. A move below MXN21.60 would likely be seen as confirmation that a high is in place.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,$CNY,China,Currency Movement,equities,Featured,newsletter,PMI