Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

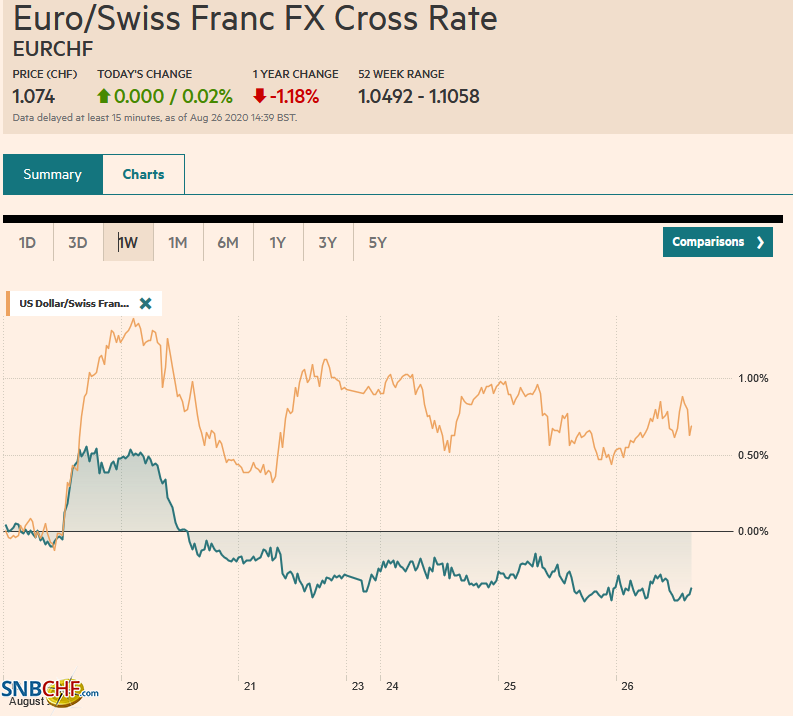

Swiss FrancThe Euro has risen by 0.02% to 1.074 |

EUR/CHF and USD/CHF, August 26(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: A consolidative tone has emerged after US equity benchmarks reached new highs yesterday. The MSCI Asia Pacific Index had reached seven-month highs on Tuesday, but Japan, China, and Australian stocks saw modest profit-taking today. European shares are recouping yesterday’s minor loss, and US shares are flat. Benchmark 10-year yields firmed yesterday, and the Asia Pacific region played catch-up today. The US 10-year is near 70 bp, the upper end of a two-month range. In Europe, the periphery is doing a little better than the core. The dollar is mixed with the Antipodean currencies and yen performing better than the euro and Swiss franc, which are nursing small losses. Among emerging market currencies, the Turkish lira, Chinese yuan, and South African rand are leading the way higher though most of the central and eastern European currencies are underperforming. Gold appears to be carving a floor near $1910, but there is little new enthusiasm for the upside. With Hurricane Laura looming and threatening US oil and refining capacity, October WTI is firm near the 200-day moving average (~$43.35). The next important chart area is near $46.50. |

FX Performance, August 26 - Click to enlarge |

Asia Pacific

News that Japan’s Prime Minister Abe has scheduled a press conference for Friday morning in Tokyo heightened speculation of his imminent resignation. Concerns about his health have circulated over the past couple of weeks, and there have been several press reports discussing possible succession. National elections would have to be held by late October 2021 in any case. In the interim, Finance Minister and former Prime Minister Aso would likely succeed Abe. Foreign Minister Motegi may be an early leading contender among LDP leadership. Kuroda’s term at the helm of the BOJ extends to April 2023. The yen showed little reaction to the news. An alternative explanation seems more likely. The current surge of COVID infections is reportedly bigger than the first wave that spurred lockdown measures. Abe’s public support has waned partly over the handling of the virus. His press conference could unveil new measures to contain the spread of the virus.

Hong Kong and New Zeland reported July trade figures earlier today. Hong Kong’s exports fell 3% year-over-year after a 1.3% decline in June. Imports fell by 3.4%, almost half the 7.1% pace of decline seen in June. The trade deficit narrowed to HKD29.8 bln from HKD33.3 bln. Hong Kong exports to the mainland rose by 5.2%, and the trade surplus stood at about HKD30 bln. Exports to the US were off 20%, and the surplus is about HKD10 bln. New Zealand reported slightly lower exports (NZ$4.97 bln vs. NZ$5.08 bln) with imports little changed that resulted in a smaller trade surplus (NZ$282 mln vs. NZ$475 mln). The rolling 12-month balance is still in deficit, but it is the smallest since 2014 when it last reported a surplus on this metric.

Saudi Arabia has decided against a $10 bln refining/petrochemical joint venture with China’s Norinco. It is not clear the factors that went into the decision, but US lobbying may have been a critical factor. Norinco reportedly has ties to the Chinese military. After the Israeli-UAE normalization of relations, securing a similar agreement with Saudi Arabia may be the next big score.

The dollar is trading sideways in the upper end of yesterday’s range against the Japanese yen. So dar, it is the first session since August 14 that the greenback has not traded with a 105-handle. It appears to be caught between two large option expirations today. There are options for about $1.5 bln struck between JPY106.00 and JPY106.15. On the top side, there are options for nearly $970 mln at JPY106.50-JPY106.60. The Australian dollar is in a very tight range today, hardly moving more than a tenth of a cent from $0.7200. A break of this narrow range is likely, and the bias is likely lower. Initial support is seen around $0.7180. The greenback lurched lower against the Chinese yuan, falling to almost CNY6.8880 before finding support. The reference rate was set at CNY6.9079, while the median bank model in the Bloomberg survey projected CNY6.9100. The yuan has risen against its basket (CFETS) for the fourth consecutive session.

Europe

Virus cases are on the rise in Europe. According to reports, the rolling seven-day average number of cases has accelerated to 6.5% from 3.2% for the 4 largest eurozone economies (Germany, France, Italy, and Spain). In the US, the rate has fallen from 11% to about 5.5%%.

This is spurring a fresh policy response. In Germany, Finance Minister Scholz secured the government’s approval to extend the wage support program until the end of next year. The program covers about 2/3 of the wages of households with children and allows the employers to maintain their workforce. IFO estimates that in May, seven million Germans were in the program. Now it is closer to 5.6 mln. Reports suggest France will unveil a new 100 bln euro stimulus effort next week.

Meanwhile, two foreign policy issues are unresolved. First, Turkey has rejected German mediation efforts and refuses to stop its exploration in contested waters in the Mediterranean as a precondition to negotiations. Second, Merkel’s attempt to get Putin to explain the poisoning of opposition leader Navalny has yet to produce a response from Moscow.

So far, today is the first in four sessions that the euro has held above $1.18. It is trading within yesterday’s range (~$1.1785-$1.1845), and through midweek, it has not moved outside the range set last Friday (~$1.1755-$1.1885). There is an option for almost 690 mln euros at $1.1830 that will be cut today. There is another for nearly 800 mln euros at $1.1775 that also expires today.Sterling is little changed and is hovering around the $1.3150-level where a GBP385 mln option will expire today. It looks to be confined between $1.3120 and $1.3170.

America

While the manufacturing surveys have been mixed, there is no doubt about the strength of the housing market. Consider the recent string of data. Housing starts jumped 22.6% in July. The median forecast in the Bloomberg survey was for a 5% increase. Permits rose 18.8%, Existing home surged 24.7% compared with median estimates for a 14.6% increase, and follows a 20.2% rise in June. New home sales were expected to have edged higher in July, but instead, they rose by 13.9% after the June series was revised to 15.1% from 13.8%. To sure, it is not merely about the pace of activity, but note that the level of existing and new home sales are the highest since late 2006.

As some US companies in some industries looking for alternatives to Chinese suppliers, Vietnam is seen as a candidate. However, the US Treasury Department claimed yesterday that Vietnam had purposely undervalued the dong by 3.5%-4.8%. It cited its $22 bln of intervention as the main driver. This is the first assessment issued under new rules that allow the Commerce Department to recognize currency undervaluation as a form of subsidy when calculating anti-subsidy duties. There is some suspicion that yesterday’s report paves the way to include Vietnam in the Treasury’s next report on currency manipulation. In the scale of currency misalignment, an imprecise measure, a 3.5%-4.8% deviation does not seem particularly significant, and Vietnam is a poor country with GDP per capita of around $2500. Previously, it appears that the US would tolerate deviations from the rules it set to allow space for small, poor countries to develop. The new thinking seems to be that no slight it too small and umbrage must be taken no matter the magnitude of the wrong. Vietnam has enjoyed a rising trade surplus with the US, but this appears to be a shift in the global division of labor and not a result of small currency misalignment.

The US reports July durable goods orders. Although June’s gain of 7.6% is unlikely to be repeated, the median forecast (Bloomberg survey) of 4.7% would start Q3 off on a firm note. Most of the gains are coming from the transportation sector (think autos) and excluding both defense and aircraft, the gain will be a more modest 1.7% or around half of the June gain. Yesterday’s $50 bln sales of two-year notes was well received, with a higher bid-cover than seen recently, and dealers took a smaller part than it has in recent auctions of this tenor. Today, Treasury sells $22 bln of a two-year floating-rate note (re-opening) and $51 bln of a new five-year note. The focus to is on Hurricane Laura that is impacting refinery runs and oil output. The storm and the drawdown in oil inventories (API estimate 4.5 mln barrels) are underpinning oil prices. Fed chief Powell speaks at the Jackson Hole symposium tomorrow. Canada’s economic calendar is empty. Mexico reports its final look at Q2 GDP (-17.2% quarter-over-quarter). Still, it will be the central bank’s report on inflation, which will command attention as rising prices are seen limited the scope for additional rate cuts.

The greenback has been unable to resurface above CAD1.3200 so far today. It found support though at CAD1.3160, and the intraday technicals favor a push higher. Above CAD1.3200, resistance is seen in the CAD1.3225-CAD1.3240 area. Meanwhile, the US dollar remains pinned near recent lows against the Mexican peso. In the first two sessions this week, the greenback has found support in the MXN21.88 area. Last month’s low was closer to MXN21.85. Immediate resistance is seen near MXN21.96 and then MXN22.02. Only a move above MXN22.05 is noteworthy.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,China,Currency Movement,EUR/CHF,Featured,Japan,newsletter,OIL,Saudi-Arabia,USD/CHF