Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

Swiss FrancThe Euro has fallen by 0.03% to 1.0743 |

EUR/CHF and USD/CHF, August 25(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: Soaring US stocks, optimism about a vaccine, and the affirmation of the US-China trade agreement are buoying global equities today. The MSCI Asia Pacific Index is near seven-month highs and was led today by more than 1% gains in the Nikkei and Kospi. Europe’s Dow Jones Stoxx 600 is around 0.5% firmer to approach the 200-day moving average, which has capped the upside. US stocks are firmer, and the S&P 500 is set to gap higher again at the opening. Bond yields 2-4 bp higher today, and that puts the US benchmark near 67 bp. Italian bonds are the outlier and the 10-year yield is jumping seven basis points. The US dollar is mostly lower, with the European currencies outperforming the dollar-bloc and yen. Emerging market currencies are mixed. Turkey, Russia, and Hungary are heavy, and the JP Morgan Emerging Market Currency Index is paring yesterday’s gains. Gold is consolidating around $1933 after reversing lower yesterday. Crude oil is little changed with the October WTI contract hovering around $42.50. The 200-day moving average (~$43.30) provides the near-term ceiling. |

FX Performance, August 25 - Click to enlarge |

Asia Pacific

US Treasury Secretary Mnuchin and Trade Representative Lighthizer reportedly talked with senior Chinese officials and affirmed the commitment to the Phase 1 trade deal. It is not surprising and has been hinted at for the past week or so. China is recognized to have taken “significant” steps. Private estimates suggest China needs to purchase $130 bln of US goods here in H2 to fulfill its goals. Meanwhile, China has taken other measures that were called for, including reduce non-tariff barriers to US agriculture, ease the limits on investment in insurance, securities, and futures, and enhance protection of intellectual property.

Japan sold JPY1.2 trillion of a new 20-year bond today. With a yield of 40.5 bp, the auction saw strong demand. The bid-cover was 3.92, slightly above last month’s sale. This begins a heavy supply period that includes a two-year note sale tomorrow. Next week, Japan sells 10- and 30-year bonds.

The US dollar set a six-day high against the yen just shy of JPY106.40. However, the buyer may have exhausted itself in the European morning, and the intraday technical indicators warn of the risk of a pullback toward JPY106.00. The Australian dollar continues to trade inside last Friday’s range (~$0.7140-$0.7215). It found support near $0.7150 in late Asia trade and appears poised to retest the $0.7200 area. The PBOC set the dollar’s reference rate at CNY6.9183 compared with the median bank model projection of CNY6.9168. The greenback has remained within last Friday’s range against the yuan as well (~CNY6.90-CNY6.9255)

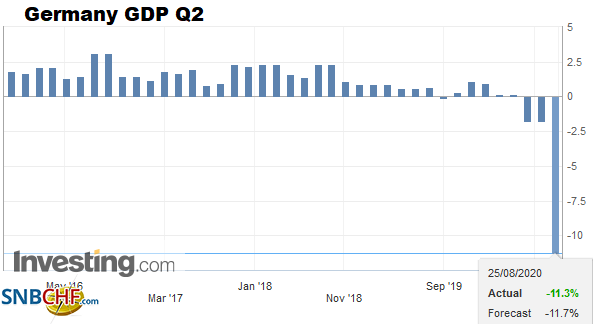

GermanyGermany’s August IFO showed investor confidence continued to improve. The impression of the business climate rose to 92.6 from 90.4, a little more than expected. It is the fourth consecutive increase and stands at its best level since February. The expectations component rose to 97.5 from 96.7. Economists in the Bloomberg poll projected a stronger result (98.0). That said, it is the highest since November 2018. The current assessment edged higher to 87.7 from 84.5. It is the best level since March. Separately, Germany reported details to its Q2 GDP, which was revised to show a 9.7% quarterly contraction instead of -10.1%. Consumption was weaker than anticipated, while capital investment was somewhat stronger. The key policy issue presently is whether to extend the wage support program of short-term work. |

Germany GDP, Q2 2020(see more posts on Germany Gross Domestic Product, ) Source: investing.com - Click to enlarge |

That US-Europe trade deal struck at the end of last week, with EU ending its (8-12%) tariff on US lobsters in exchange for reduced (50%) US levies on several consumer goods items, including crystal glassware, ceramics, cigarette lighters, and prepared meals, is not quite what it appeared. Rather than be a bilateral effort, the US and EU adjusted their WTO tariff schedule. This means that the changes apply to all WTO members, though the product mix intentionally picked for mutual benefit. The EU trade agreement with Canada (2017) eliminated tariffs on Canadian lobsters. Separately, last week, the US tweaked its retaliatory tariffs for the WTO’s finding that Airbus benefited from illegal subsidies. As early as next month, the WTO is expected to conclude that Boeing also drew illegal government support, and by allowing EU retaliatory tariffs, it could be an important step toward resolving the dispute.

The euro found new bids in Asia after testing yesterday’s late low near $1.1785. It has managed to return to the $1.1845 area in the European morning, but the intraday technicals are stretched, and there is a 1.1 bln euro option at $1.1850 that expires today, which might deter the bulls. Sterling also tested yesterday’s low (~$1.3055) and has returned to the session highs in Europe (~$1.3115). Even if new highs are recorded, the $1.3150 high seen yesterday seems too far today. Note that the 5-and 20-day moving averages, a proxy for short-term trend followers, crossed higher for the euro and sterling in early July and have crossed lower since. However, these are at risk in the coming days.

America

The re-jig of the Dow Industrials, announced yesterday that will take effect next week is partly a function of Apple’s decision to split its shares. The Dow is weighted by price rather than market value. The shift away from Exxon, Raytheon, and Pfizer for Amgen, Honeywell (returns), and Salesforce seems subjective and geared to the “new economy.”

In its ninth case over the US-Canada longlasting timber dispute, the WTO found in Canada’s favor. It concluded that the US duties imposed on Canada’s softwood lumber (17.99%) were improper. The US did not demonstrate the price paid for Canadian firms to purchase lumber for government-owned lands was not below market prices. A different panel last year upheld US anti-dumping duties. The US has threatened to appeal yesterday’s ruling. Yet, because the US is blocking new appellate judges and there are currently not enough to hear the case, appealing in this context means that the US would not have to give up its levies. Note that Canada, the EU, and China have settled on an interim arbitration process to workaround the effective US block of appeals, which the US fighting.

The US economic calendar looks full with house prices, new home sales, and the Richmond Fed manufacturing survey. But even in the best of times, these are not market-movers. The S&P CoreLogic house prices are for June. New home sales are for July, and we know that June sales were the strongest in around 13 years. The Empire and Philadelphia August manufacturing surveys were softer than expected, and even if the Richmond Fed survey surprises on the upside, it is unlikely to resolve the conflict between the weaker Fed surveys and stronger preliminary PMI. Mexico reports its Q2 current account. Mexico’s current account is likely to have recorded a small surplus. Dramatic improvement took place last year, and the four-quarter average is in surplus for the first time since the late 1980s.

The US dollar traded on both sides of Friday’s range against the Canadian dollar yesterday, but the close was inconclusive. There was no follow-through greenback buying as it bumped against a band of resistance that extends from CAD1.3240 to CAD1.3265. It found support in late Asia and early Europe near CAD1.3210. Below there support is seen around CAD1.3180. The greenback is softer against the Mexican peso. Although it continues to straddle the MXN22.00 area, it has been spending more time below it. Support is seen in the MXN21.85-MXN21.88 area.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: EUR/CHF,Featured,Germany Gross Domestic Product,newsletter,USD/CHF