Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

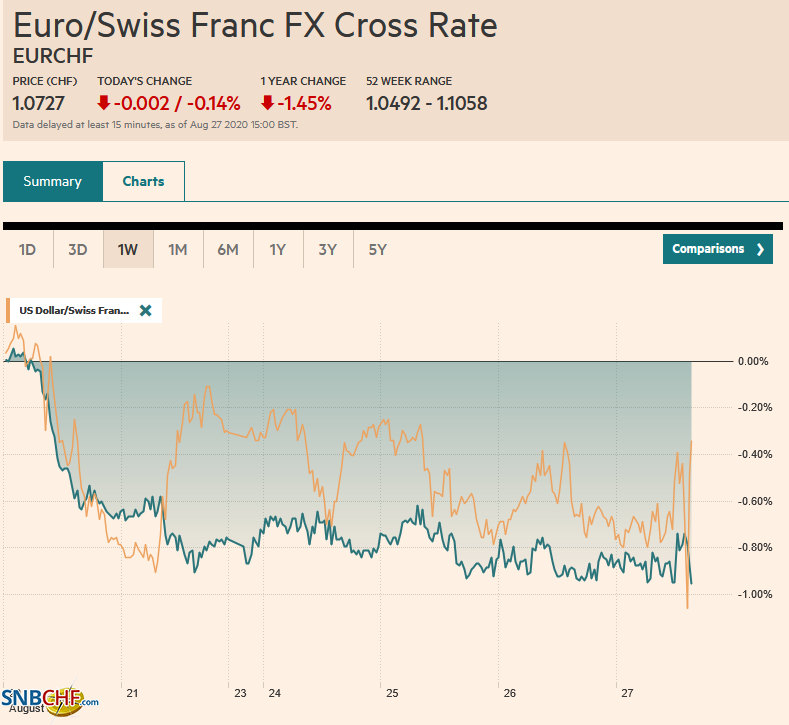

Swiss FrancThe Euro has fallen by 0.14% to 1.0727 |

EUR/CHF and USD/CHF, August 27(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The strong rally in US equities yesterday, with the fifth consecutive gain in the S&P 500 and a big outside up day in gold, failed to spur follow-through buying today. Asia Pacific equities were mixed. China, Australia, and India rose while most of the rest of the regional markets fell. Europe’s Dow Jones Stoxx 600 is around 0.30% lower near midday, and it continues to flirt with the 200-day moving average. US shares point to a lower opening, though Fed Chair Powell presents to the Jackson Hole Symposium just as the local markets open. Benchmark yields are 2-4 bp lower, putting the US 10-year near 68 bp. Of note, China’s 10-year bond yield rose and, at 3.05%, is at the highest in seven weeks. The dollar mixed. Among the majors, Australia and New Zealand dollar lead the move, and among the emerging markets, the Turkish lira and Indian rupee are the best performings. The JP Morgan Emerging Market Currency Index is moving higher for the third session this week. Gold’s constructive price action yesterday failed to shake off the corrective forces and has come back lower today and may test the $1930 area. Hurricane Laura made landfall, sapping some of its power, but some 80% of Gulf oil production and 3 mln barrels of refining capacity has been shuttered. October WTI is hovering near five-month highs above $43 a barrel. |

FX Performance, August 27 - Click to enlarge |

Asia Pacific

Within 24 hours or so that some press reports were playing up optimism about the US-China trade agreement, the dispute over the South China Sea escalated. The US imposed new trade and visa restrictions on 24 entities and people that helped “reclaim and militarize the outposts” in the South China Sea. Calling them islands grants certain rights, which the US does not recognize for China. Earlier in the day, as part of ongoing exercises, China fired as many as missiles in undisputed waters in the South China Sea. On Tuesday, Beijing objected to flyovers by a US spy plane. While a more aggressive stance against China is part of the US political cycle, China’s response is more thunder than rain, more symbolic than substantive. Vietnam called on China to cancel its drills as it violated its sovereignty over the Paracel Islands.

China’s industrial profits jumped 19.6% in July after an 11.5% gain in June. Still, through the first seven months of the year, profits are off 8.1% year-over-year. Reduced deflation in producer prices and stronger exports appeared to help. The August PMI is due over the weekend and will likely confirm a modest recovery remains intact.

There were a few other regional developments to note. First, South Korea’s central bank held rates steady (0.5%) as widely expected. It did revise its GDP forecast lower to -1.3% from its May forecast of a 0.2% decline. The central bank faces pressure to do more. Second, Australia reported a further slide in private sector investment. Capex fell 5.9% in Q2 after a 2.1% decline in Q1. Third, Japan’s All-Industry Activity Index jumped 6.3% in June after a revised 4.1% decline (from -3.5%) in May. The Japanese economy contracted for three consecutive quarters and is expected to be returning to growth in the current quarter.

The dollar is mostly confined to a 20-tick range on either side of JPY106 so far today. Two option expirations may sandwich the price action. One for about $705 mln is at JPY105.75, which is just above the week’s low, and the other set is in the JPY106.50-JPY106.60 area for $1.1 bln. The Australian dollar has risen every day this week, and near $0.7250 is knocking the year’s high set earlier this month near $0.7275. However, the intraday technicals are stretched, and a pullback seems likely. Initial support is seen near $0.7225. The PBOC set the dollar’s reference rate at CNY6.8903, a bit above the models in the Bloomberg survey, where the median projection was CNY6.8860. The low for the year was near CNY6.84 in January.

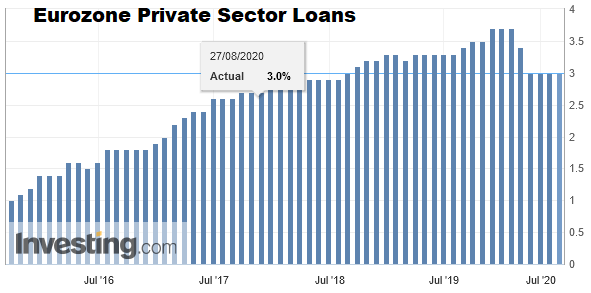

EurozoneEurozone money supply growth accelerated to 10.2% in July from 9.2% in June. During the Great Financial Crisis, EMU’s M3 growth peaked at 12.5% (November 2007). Loans to household and non-financial businesses maintained their June pace when sales and securitization are accounted for at 3% and 7%, respectively. While central banks have had to innovate and not all innovations will survive. Still, we suspect that the negative-yielding targeted loans arranged by the ECB, which expands the balance sheet as much as buying bonds, is an important and unsung success story. |

. |

Eurozone Private Sector Loans YoY, August 2020(see more posts on Eurozone Private Sector Loans, ) Source: investing.com - Click to enlarge |

EU Trade Commissioner Hogan resigned amid criticism of his behavior and attitude about attending a golf dinner last week that violated Covid-related social rules as well as his violation of quarantine rules when he returned to Ireland. Hogan was leading the negotiations with the US and had just reached an agreement that reduced WTO tariff schedules, which allowed the EU to scrap its levy on lobster, which seemed to see a level of discussion well out of proportion of its economic benefits. While Ireland will name a successor to Hogan, Ireland may lose this key post.

The German government approved the extension of the short-term work subsidy until the end of next year and today has extended the insolvency waiver as well. Separately, Germany has put Brexit off the agenda at next week’s EU ambassador meeting because there is has been no substantial progress in the negotiations.

The euro’s high for the week near $1.1850 was tested, and is held in Asia and lost the upside momentum that lifted it from the test on the $1.1770 in North America yesterday. An option struck at $1.1800 for 580 mln euros may come back into play. Reflecting the consolidative forces, the five-day moving average is crossing below the 20-day for the first time since early July. Sterling set a new high for the week near $1.3230, but its upward progress has stalled. Initial support is seen around $1.3170-$1.3180, but the lower end of the range is closer to $1.30. Near GBP0.8950, the euro is at its lowest level here in August. Last month’s low was a little above GBP0.8935. Resistance is pegged around GBP0.8980.

United States

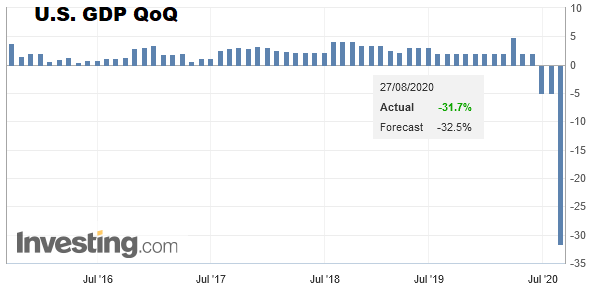

|

U.S. GDP QoQ, Q2 2020 Source: investing.com - Click to enlarge |

In addition to the strong housing data seen recently, news yesterday gives reason to expect the nearly “V” recovery in manufacturing, led by autos, to continue. It is not just that the headline numbers were better than expected or that the June series was revised higher, but orders for motor vehicles and parts jumped almost 22% in July after an 85.6% surge in June. As an aside, Boeing reported no new orders in July and only one in June. The Richmond Fed survey gains may not have really offset the disappointment from New York and Philadelphia, but the durable goods order report does, and economists may revise up Q3 GDP. The Atlanta Fed’s GDP tracker edged up to 25.6% (from 25.4%) after the report.

Separately, yesterday’s five-year auction was well-received despite its record size ($51 bln) and near record-low yield (less than 30 bp). Without stress, $22 bln of two-year floating-rate notes were also sold. Yesterday’s auctions follow the strong demand for the $50 bln conventional two-year note sale. The longer-dated paper sold recently did not meet such strong demand, which raised some questions about saturation. No coupons are being sold next week, and the following week features a three-year note sale and the re-opening of the 10-year.

The US dollar slipped to new seven-month lows against the Canadian dollar yesterday near CAD1.3130. It is consolidating in a narrow range below CAD1.3170. The greenback needs to resurface above CAD1.3200, and really above the high for the week (~CAD1.3240) to be noteworthy. The US dollar is also consolidating in tight ranges against the Mexican peso. Mexico’s July trade balance is unlikely to inject much volatility into peso trading today. Nearby resistance is seen in the MXN22.00-MXN22.05 area, while support has been found near MXN21.88.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,China,Currency Movement,Featured,federal-reserve,Germany,newsletter,South Korea