Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

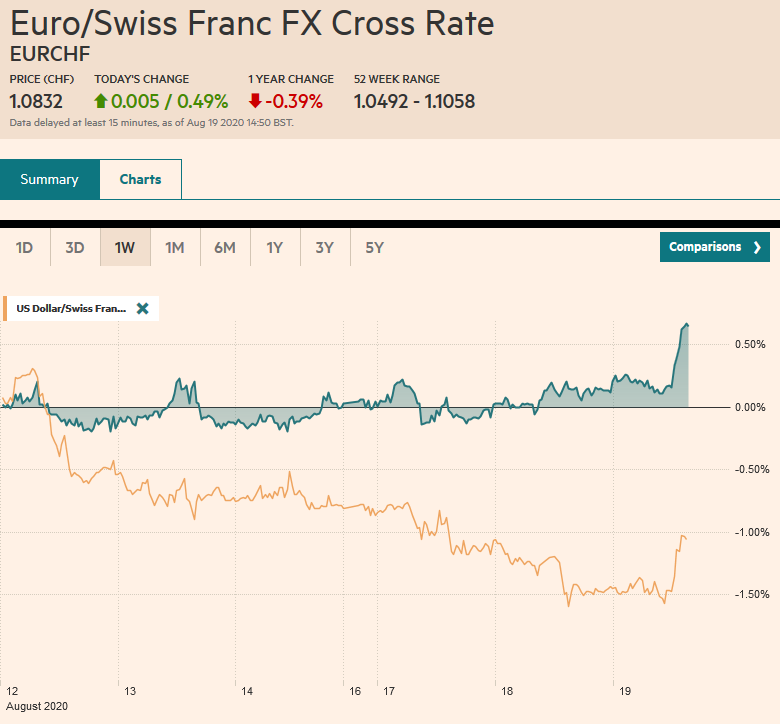

Swiss FrancThe Euro has risen by 0.49% to 1.0832 |

EUR/CHF and USD/CHF, August 19(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The S&P 500 and NASDAQ set new all-time highs yesterday, but the continued outperformance of US equities have failed to lend the dollar much support. It was sold to new lows for the year yesterday against the euro, sterling, the Swedish krona, and the Australian dollar. Asia Pacific equities were mixed. China, Taiwan, and Hong Kong fell, while Japan, Australia, and South Korea advanced. In Europe, the Dow Jones Stoxx 600 remains confined to last Friday’s ranges and is practically unchanged so far this week. US shares are a little firmer. Benchmark bond yields are 1-2 basis points lower, putting the US 10-year around 65 bp. The German 30-year bond, which yields around minus five basis points, saw record demand at today’s auction. The dollar is softer against most of the majors, with the dollar bloc and the Norwegian krone leading. The greenback is mixed against the complex of emerging market currencies. Gold is paring yesterday’s gains but found support near $1980. September WTI posted a five-month high close, but it remains stuck between the about $41.60 and the 200-day moving average (~$43.40). |

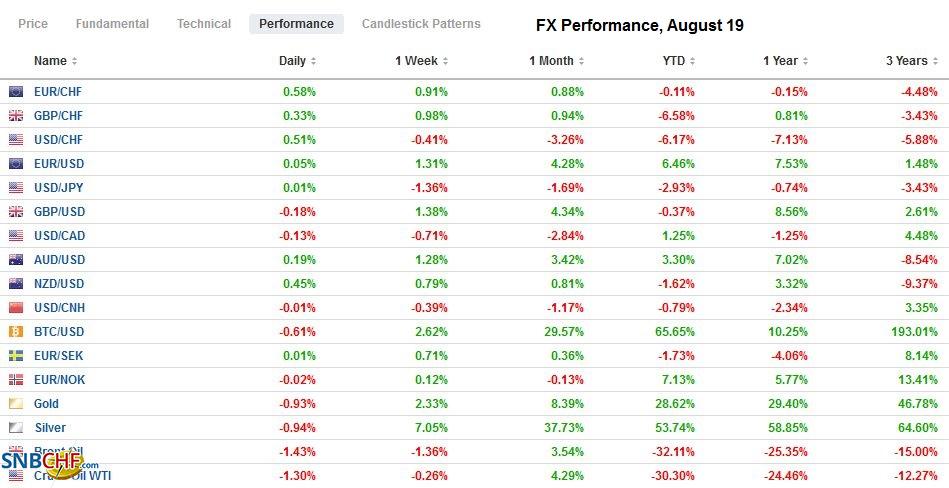

FX Performance, August 19 - Click to enlarge |

Asia Pacific

The South China Morning Post had reported that US-China officials were to talk over the past weekend to review the Phase 1 trade deal. The meeting apparently never made it onto the official calendars, and the meeting was ostensibly canceled due to scheduling conflict, which was attributed to the fact that China wants to discuss the latest US sanction. President Trump says that he canceled the talks because he was troubled by Beijing’s response to the virus. Nevertheless, Trump and other senior officials (e.g., Navarro and Kudlow) have claimed the trade agreement is on track, and China is adhering to its commitment, and have highlighted recent agriculture purchases. Many observers are less sanguine and recognize that even if China can fulfill is agriculture purchases, it woefully behind in most other areas, including energy and airplanes.

Meanwhile, the Trump Administration is urging colleges to divest its Chinese equity exposures, as a new front in the financial decoupling is opened. Separately, Beijing has allowed United and Delta to double to four the number of roundtrip flights, and the US reciprocated by allowing eight roundtrip flights a week by Chinese carriers.

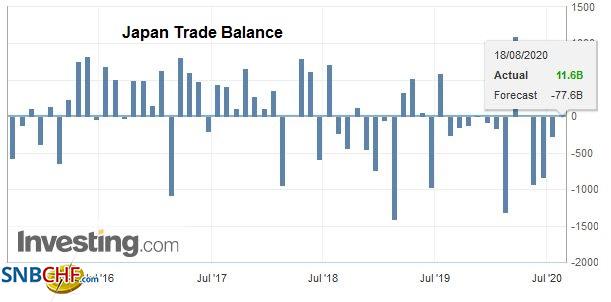

| Japan reported an unexpected but small trade surplus in July, as exports improved while imports fell. Exports fell for the fifth consecutive month on a year-over-year basis, but at 19.2%, it was the smallest decline in four months. Autos (`-30%) and auto parts (~-32.5%) remain problematic. The decline in net exports accounted for about 40% of Japan contraction in Q2. Exports to the EU are off around 30.5% and to the US 19.5%. Japan reported the first increase in exports to China (~8.2%) for the first time this year. Imports fell 22.3% from a year ago. In June, they were off 14.4%. Separately, Japan reported a disappointing fall (7.6%) in June’s core machinery orders. The median forecast in the Bloomberg survey was for a 2% increase. The report raises questions about capex here in Q3. |

Japan Trade Balance, July 2020(see more posts on Japan Trade Balance, ) Source: Investing.com - Click to enlarge |

Japan’s Prime Minister Abe’s health has been a perennial issue that is resurfacing now. Recall that in his first term (2006-2007) due to ulcerative colitis he has been aided by medicine that was previously unavailable in Japan. He visited the hospital at the start of the week amid some press reports suggesting illness and has been unusually absent from parliament and press conferences. Reports suggest he has check-ups every six months, and the most recent one was in June. Not to get too far ahead of the story, but speculation of succession has begun swirling. Yet to be clear, an election will be held by late October next year. Abe and his cabinet have sagged in the opinion polls. If Abe steps down, Finance Minister Aso, who also served as Prime Minister for a year (September 2008-September 2009) would serve on an interim basis. Reports suggest Foreign Minister Motegi is trying to organize a bid. Abe has supported LDP policy chief Kishida over objections from his close advisers, but some think that Abe’s rival, former LDP General Secretary Ishiba have the inside track.

The dollar extended its pullback after it was rejected a little above JPY107 last week. It found bids today a little above JPY105, where there is an option for around $960 mln that expires today. There is another expiring option at JPY105.25 (~$530 mln) and a set between JPY105.80-JPY106.00 (~$855 mln). The Australian dollar is trading at new highs for the year (~$0.7275) in the European morning. It has risen above its 200-week moving average (~$0.7255) for the first time in over two years. The next important chart area is near $0.7300, but the intraday technicals are stretched. The Aussie’s 10-day rally against the New Zealand dollar ended yesterday, and the cross has been subject to more profit-taking today. The PBOC set the dollar’s reference rate at CNY6.9166, a touch firmer than the bank models implied, but the greenback fell anyways to a new seven-month low (~CNY6.9042)

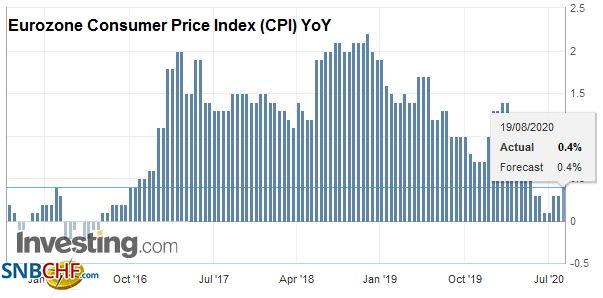

EuropeThe UK reported stronger than expected gains in July consumer prices. CPIH rose 1.1% from a year ago. Economists had anticipated a decline to 0.7% from 0.8% in June. Core CPI rose to 1.8% from 1.4% instead of falling to 1.2% as predicted. |

Eurozone Consumer Price Index (CPI) YoY, July 2020(see more posts on Eurozone Consumer Price Index, ) Source: investing.com - Click to enlarge |

| The pandemic is changing both shopping and discount patterns, which in turn is impacting measured inflation. For example, seasonal clothing sales did not materialize, and this is translated into higher prices. Some businesses tried to pass on to the consumer the added costs of protective measures. Separately, gasoline prices rose by the most since January 2011. There are good reasons to expect that today’s report does not signal a resurgence in inflation. |

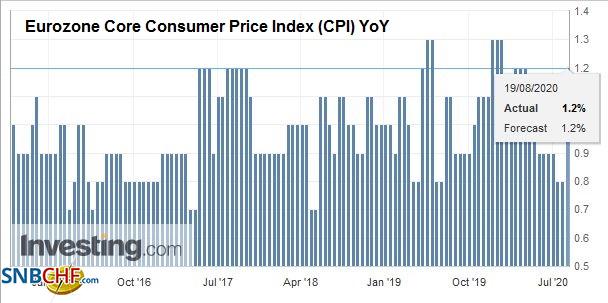

Eurozone Core Consumer Price Index (CPI) YoY, July 2020(see more posts on Eurozone Core Consumer Price Index, ) Source: investing.com - Click to enlarge |

| New measures, including a cut in the sales tax for some purchases and other government measures to support businesses (including subsidies for restaurant meals), and lower energy prices should see price pressures ease. |

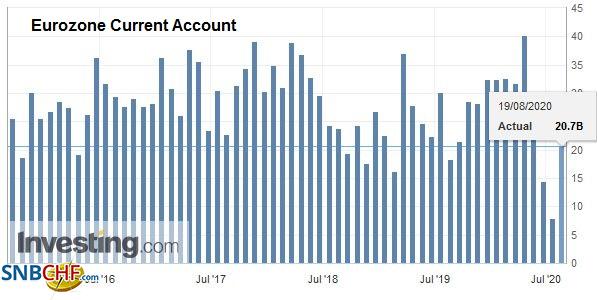

Eurozone Current Account, June 2020(see more posts on Eurozone Current Account, ) Source: investing.com - Click to enlarge |

With Belarus moving troops to its border, tensions are rising. There is some push for the EU to call for a new vote and unveil sanctions to enforce its will. The pressures have yet to impact the markets, but it is simmering below the surface.

Turkey’s central bank suspending what had been the key one-week repo operations last week, which had provided funds at 8.25%. Yesterday, it took another step toward tightening financial conditions by reducing by 50%, banks’ ability to borrow overnight funds in the interbank market. It looks as if banks would increasingly be forced to the Late Liquidity Window, which offers funds for 11.25%. With the help of broad-based dollar weakness, the lira snapped a four-day decline to post a minor gain yesterday and is slightly firmer today.

The euro is firmer but holding just below yesterday’s two-year high near $1.1965. So far, today, it is holding above $1.19 for the first time. There is a 1.7 bln euro option struck there that expires today. Below there, support is seen near $1.1880. On the top side, the $1.20 level has psychological value, and recall that is the euro’s average value since its launch in 1999. Sterling extended yesterday’s gains to poke through $1.3265. The momentum has not been sustained, and sterling slipped to session lows in the European morning below $1.3230. Initial support is seen near $1.32.

America

Canada’s Deputy Prime Minister Freeland has replaced Morneau as Finance Minister, and investors continued to do what they were doing before the change. The Canadian dollar strengthened for the 11th time in the past 14 sessions. Canada’s bond yields tracked US Treasury yields lower for the third consecutive session, and the Canadian stocks were unable to keep up with the S&P 500 and NASDAQ to pare Monday’s gains. Month-to-date, Canada’s shares have gained a solid 2.8%, putting them a little above Italy at the bottom of the G7 rally. Canada committed C$240 bln to support the economy, generating a deficit of around 16% of GDP. More support will likely be needed. Freeland has a strong reputation for pragmatism and competence.

North American highlights today include Canada’s July CPI, US EIA energy estimates, and the FOMC minutes. Headline inflation in Canada remains subdued, and the year-over-year rate may ease to 0.6% from 0.7%. However, this continues to pick up the drop in energy prices. The underlying measures remain firm (~1.6%-2.0%). The report is unlikely to have much market impact. API warned that US oil inventories continued to fall. Still, the large gasoline build means 1) seasonal demand remains weak, and 2) plays on fears of lower refinery demand amid reports that four refineries have been idled). The FOMC minutes will be scrutinized for clues of what the central bank may be prepared to do (formally embrace a symmetrical inflation target, yield curve control?).

The US dollar is falling against the Canadian dollar for the third consecutive session after declining in four sessions last week before bouncing a little ahead of the weekend. The greenback has dipped below CAD1.3140. It finished last month a little above CAD1.34. It is at its lowest level since late January. The US dollar has a five-week losing streak in tow and looks set to extend it for the sixth week. Nearby resistance is seen around CAD1.3170. The US dollar’s weakness appears more pronounced against the majors than most emerging market currencies, including the Mexican peso. The greenback is in narrow ranges around MXN22.00. Monday’s range was roughly MXN21.9070 to MXN22.2160. It continues to define the price action. FOMC minutes that hint at more work next month could see the peso gain later in today’s session.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,Canada,China,Currency Movement,Featured,Japan,newsletter,SPX,Turkey,U.K.