Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

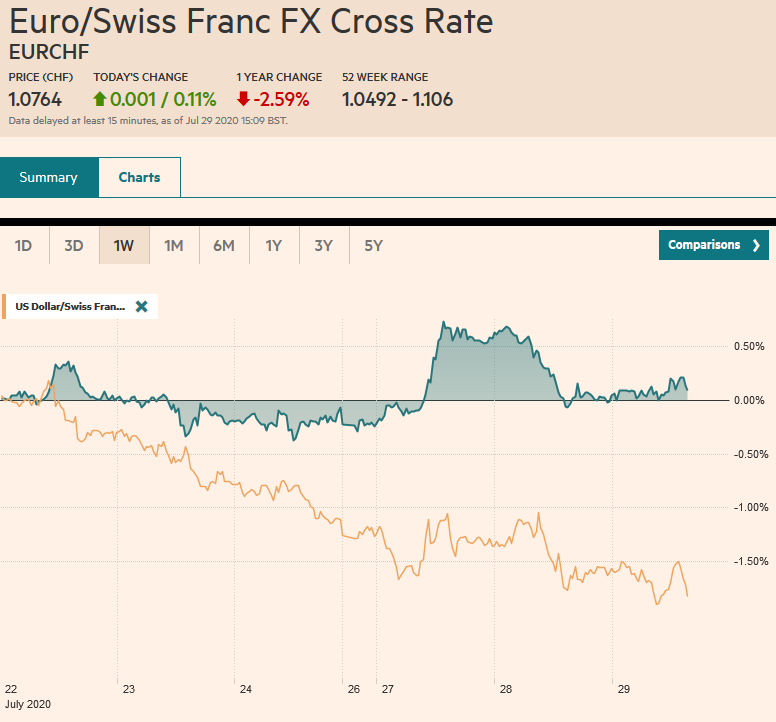

Swiss FrancThe Euro has risen by 0.11% to 1.0764 |

EUR/CHF and USD/CHF, July 29(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: Global equity markets are stabilizing today, and the dollar is once again on its back foot. Chinese markets led a mixed regional performance with a 2%-3% gain, while South Korea and Hong Kong markets also advancing. The strength of the yen appears to weigh on Japanese shares. The Nikkei fell for the fourth consecutive session. European stocks are posting small gains as financials and energy blunt strong gains in real estate and consumer staples. US shares are firm. Bond markets are quiet as the US 10-year hovers around 58 bp, and real yields are near record lows. The dollar value of negative-yielding debt hit a new record yesterday of $15.52 trillion. The dollar is weaker against all the major currencies, and the greenback fell further below JPY105 that was violated in the North American session yesterday. Emerging market currencies are mostly higher on the back of the dollar’s pullback, but the Turkish lira continues to struggle. The JP Morgan Emerging Market Currency Index is up for the third session in the past four. Gold and oil are firm but little changed. |

FX Performance, July 29 - Click to enlarge |

Asia Pacific

Fitch reduced the outlook of Japan’s long-term credit rating to negative from stable. S&P had announced a similar move last month. Japanese government bonds seemed unperturbed, and the yield of the 10-year benchmark slipped a hair to 1.4 bp. The combination of weaker growth, despite being able to apparently contain the virus (though Fitch did recognize the worrisome increase in cases recently) and the government’s spending plans add significantly to the debt burden. Fitch maintained the A rating.

Australia’s Q2 CPI fell to 1.9% from 0.3% in Q1. This pushes the year-over-year rate into deflationary territory of -0.3% (+2.2% in Q1). The underlying measures (trimmed mean and weighted median) held up considerably better at 1.2% and 1.3%, respectively (from 1.8% and 1.6% in Q1). Australian bonds rallied, partly playing catch-up with the move in US Treasuries yesterday, and the 10-year yield fell 4 bp to 87 bp, leaving it virtually flat on the month.

The Hong Kong economy contracted for the fifth consecutive quarter. The 0.1% contraction in Q2 follows a 5.3% contraction in Q1. However, that means that the Hong Kong economy is 9% smaller than a year ago. The median forecast in the Bloomberg survey was for an 8.3% contraction.

The dollar is in a 20 pip range on either side of JPY105, where a roughly $990 mln option is set to expire today. A week ago, the dollar settled at JPY107.15. For the month, the yen has risen by about 2.9%, making it the second-worst performing major after the Canadian dollar (+1.7%). The Australian dollar firmed to new highs for the year as it approached without yet trading at $0.7200. The next important chart point is near $0.7240. The PBOC set the dollar’s reference rate at CNY6.9969, in line with the median bank model. The greenback remained in narrow ranges, straddling the CNY7.0-level. The US demands that China maintains a stable yuan, and China is happy to comply. This prevents the US from gaining any competitive advantage on China from a weaker dollar while allowing China to increase its competitiveness as the yuan falls against its other trading partners (CFETS basket).

Europe

The EMU data highlight for the week is still ahead. On Friday, investors get the first look at Q2 GDP and July inflation. Comments by ECB officials today have not broken new ground. Officials will be reluctant to remove accommodation until inflation is back on a sustainable path toward the target. Also, the ECB has not exhausted its policy tools and is prepared to do more if necessary.

The Turkish lira remains under pressure, and the dollar is within a whisker of TRY7.0, while the euro is holding below the record high set on Monday near TRY8.2175. State banks have been active dollar sellers in the first two sessions this week, selling an estimated $3.5 bln. Turkey reports July CPI figures next week. It has been rising under as oil prices recover, bank lending is extended, policymakers are buying government bonds. The weaker lira also spurs inflation, and the lira is off around 1.6% this month to bring the year-to-date decline to 14.5%. The central bank increased this year’s CPI forecast today to 8.9% from 7.4% and next year’s to 6.2% from 5.4%. The official target is 5%. The one-week repo rate of 8.25% means that Turkish interest rates are among the lowest in the world. On the political front, under the apparent threat of sanctions by the EU, it has held back conducting the survey in the contested waters with Greece in the Mediterranean and Agean Seas.

The euro is firm. It has mostly held above $1.17 since moving above it Monday. Indeed, it has been consolidating within Monday’s range, when it reached $1.1780. Resistance is seen in the $1.1800-$1.1820 area. Sterling’s advance has carried into the ninth consecutive session, which is to say sterling has not fallen since July 16. It is approached the $1.30-mark that it has not traded above since March 10. The year’s high was set on the previous session near $1.32. The technical indicators are getting stretched. Sterling’s gains appear to be mostly an expression of a weaker US dollar. The euro’s setback yesterday snapped a five-day advance against sterling. The cross has traded between GBP0.9000 and GBP0.9150 over the last couple of weeks and tested the upper end at the start of the week.

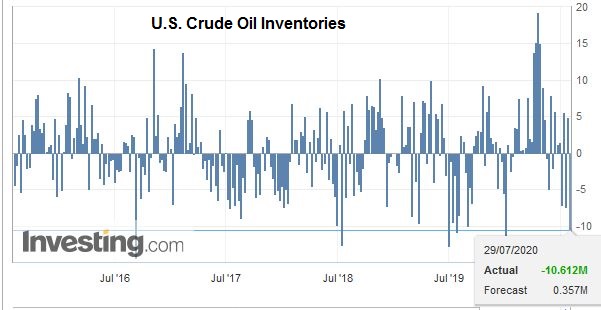

AmericaThe US reports June preliminary goods trade balance and retail and wholesale inventories. The data may see last-minute tweaks in Q2 GDP forecast for the first estimate on Thursday. The takeaway from the trade figures is the modest deterioration over the last few months with the May deficit of $75.26 bln being the largest since December 2018. Current demand appears is outstripping output and inventories are being drawn down. Inventories and trade are often difficult to estimate and are often the source of differences in forecasts. |

U.S. Crude Oil Inventories, July 29, 2020(see more posts on U.S. Crude Oil Inventories, ) Source: investing.com - Click to enlarge |

The highlight though, is, of course, the FOMC statement and Chair Powell’s press conference. Judging from recent official comments and high-frequency economic data, the Fed could express some concern, but its previous assessment in June was already downcast. The Fed indicated last month that it was monitoring a broad range of domestic and global data. Although the US and China tensions escalated, they have thus far not involved fresh trade action. The Fed referred to its inflation target as symmetric. There has been more talk about this between meetings, but it seems like a question of emphasis. A more material shift in the statement may come from how it describes its Treasury and mortgage-backed asset purchases “to sustain smooth market functioning.” The Fed may signal a shift toward supporting the economy, which creates space for a move next month that could entail more purchases and possibly some variant of yield-curve control, which both Bernanke and Yellen appeared to endorse.

Separately, and perhaps to distinguish from monetary policy proper, the Federal Reserve announced yesterday it was extending its facilities from the end of September to the end of the year. Note that the Muni facility was already slated to run until the end of December, and the commercial paper program is active until mid-March 2021. The Fed’s nine facilities have trillions of dollars of capacity, but so far, they have used something around $100 bln.

The US dollar continues to trade heavily against the Canadian dollar. Coming into today, the greenback has fallen in five of the past seven sessions. It is approaching the June low near CAD1.3315 after finishing last week around CAD1.3415. There is a large option ($2.1 bln) that expires tomorrow at CAD1.34. A break of the CAD1.33 area targets the CAD1.32 area seen in February. The year’s low set at the start of the year is closer to CAD1.2950. The greenback was sold to new lows for the month against the Mexican peso (~MXN21.85). It has settled below MXN22.00 in the first two sessions this week and appears poised to do so again today. Last month’s low was near MXN21.46. The peso’s gains reflect the attractiveness of its yields and the broader dollar decline against emerging markets as a whole, for which the peso is a proxy and the most active emerging market currency after the Chinese yuan.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,$CNY,Currency Movement,Featured,FOMC,HK,newsletter