Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

Swiss FrancThe Euro has fallen by 0.59% to 1.0743 |

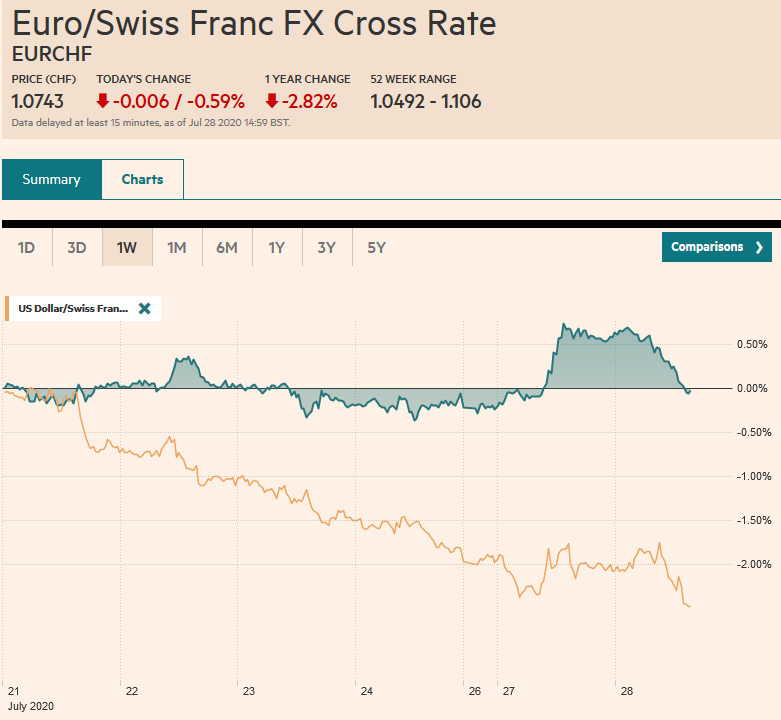

EUR/CHF and USD/CHF, July 28(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

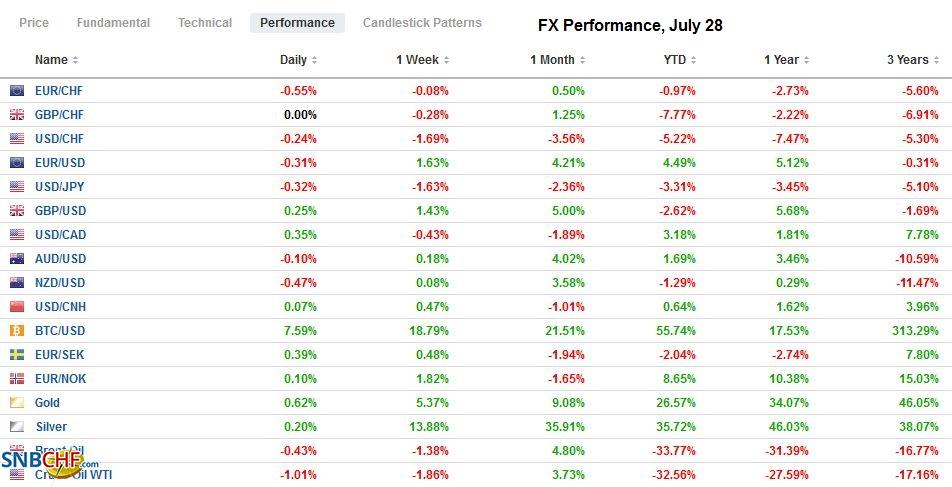

FX RatesOverview: The main development in the capital markets today is the firmer dollar against nearly all the major and emerging market currencies. Among the majors, the New Zealand dollar and Swedish krona are the heaviest (~-0.4%), while the Swiss franc and yen are marginally lower. In the emerging market space, the liquid and accessible currencies, like the Turkish lira, Mexican peso, and Russian rouble, are down the most. The lira has fallen 1% after intrasession volatility that pushed it to a record low against the euro yesterday. That seems to be the source of the pressure on the lira against the dollar. The South African rand is among the weakest among emerging market currencies today even though the IMF approved a $4.3 bln loan, the most granted so far to assist in combatting the virus. Despite the correction in the foreign exchange market, equities are mostly firm. In the Asia Pacific region, only a few markets could not sustain gains. Japan, Taiwan, and Australia were among them. South Korea led the region with a nearly 1.8% gain. Europe’s Dow Jones Stoxx 600 is up almost 0.5% after falling for the past two sessions (~2%). US shares are little changed. US bond yields backed up yesterday, with the 10-year yields popping back above 60 bp. This exerted upward pressures in Asia and Europe. Gold reached $1981 before the profit-taking pushed it to about $1907 from where it is recovering. September WTI is little changed around $41.50 a barrel. |

FX Performance, July 28 - Click to enlarge |

Asia Pacific

China is resorting to local lockdowns to combat the new outbreak in the virus. The 61 cases reported Monday were the most in four months. Separately, New Zealand became the latest country to suspend the extradition treaty with Hong Kong. That means that of the intelligence-sharing Five Eyes, only the US has not done so, though it has threatened to do so.

India has banned almost 50 Chinese apps to largely check the workaround the 59 apps banned last month. Another 250 apps are under review. India has cited threats to user privacy and national security. This is a new front in the confrontation with China. The US and Japan are considering their own bans on some Chinese apps.

The dollar is in a quarter of a yen range on either side of JPY105.45, as it is confined to yesterday’s range. The upside correction does not appear over, and the greenback could test previous support and now resistance near JPY106, where an option for $600 mln expires today (and a $1.8 bln option expires Thursday). The Australian dollar is little changed as it moves within the $0.7065-$0.7180 range that has confined it for around a week now. It has held above $0.7115 today, but it may be retested. The PBOC set the dollar’s reference rate at CNY6.9895 today, nearly spot on where the models suggested. After falling to a four-day low near CNY6.9870, the dollar recovered back above CNY7.0. China seems intent on not allowing the US to get an advantage by devaluing the dollar, something that President Trump has advocated. A stable dollar-yuan rate in a weak dollar environment means that the yuan falls against the CFETS basket. Against the basket, the yuan is at its lowest level in a little more than a month.

EuropeNews from Europe is light and the week’s highlights which include the first look at Q2 GDP (median forecast in the Bloomberg survey is for a 12% quarterly contraction), June unemployment (~7.7% vs. 7.4%), and the first look at July CPI (median forecast is for a 0.5% decline for a 0.2% increase year-over-year) still lie ahead. Today’s focus is mostly on earnings and bank earnings in particular. European banks are being encouraged to extend the hold off of dividend payout and share buybacks that were first introduced in March. This may be worth around 30 bln euros. The UK is fully aboard too. In terms of loan-loss provisioning, European banks are expected to set aside around the same amount as they did in Q1, which was about 25 bln euros. In comparison, the five largest US banks have added a little more than $60 bln in the first half to cushion sour loans. |

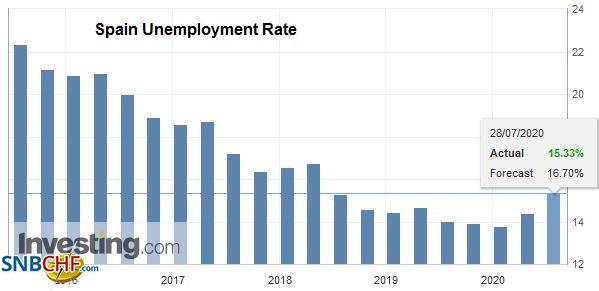

Spain Unemployment Rate, Q2 2020(see more posts on Spain Unemployment Rate, ) Source: investing.com - Click to enlarge |

Fitch lowered its five-year growth potential for the UK from 1.6% to 0.9%. It also took EMU’s potential to 0.7% from 1.2%. This could weaken the resolve of asset managers, where industry surveys suggest a desire to be overweight European stocks and the euro on ideas of economic and/or earnings outperformance. That said, the number of analyst upgrades has surpassed the number of downgrades in Europe for the first time this year.

The euro reached $1.1780 yesterday. As the momentum stalled in Asia, some light profit-taking has been seen that saw it briefly dip just below $1.17 in early European turnover. Intraday resistance is seen near $1.1740-$1.1750. In the recent move, the session high has often been recorded in North America, and we’ll watch to see if the pattern holds today. The market may turn cautious ahead of tomorrow’s outcome of the FOMC meeting. Sterling poked above $1.29 yesterday for the first time in four months. It made a marginal new high today (~$1.2905), but it too is consolidating. Support is seen in the $1.2830-$1.2850 area. As the euro was trending higher against the dollar yesterday, it also rose to about CHF1.0840, its highest level here in July. However, today’s consolidation has seen the euro slip back to around CHF1.0775. Look for it to find support above CHF1.0760.

America

The US reports house prices, Conference Board consumer confidence, and the Richmond Fed’s July manufacturing survey. Even in the best of times, these are not the typical market movers. The focus instead is three-fold: corporate earnings (today’s highlights include McDonald’s, Pfizer, and 3M), the negotiation over the fiscal bill, and the start of the FOMC meeting. Canada has not economic reports, while Mexico’s weekly reserve figures are due. It continues to gradually accumulate reserves. They have risen by about 4.5% this year after a 3.5% increase last year.

The Economic Policy Institute estimates that a cut in the $600 a week extra unemployment insurance to $200 a week will reduce aggregate demand and cut the number of jobs that were projected to be created. It expects a loss of about 2.5% growth and 3.4 mln fewer jobs. After this week’s FOMC meeting and the first look at Q2 GDP, the US July employment report is due at the end of next week. It is one of the most difficult high-frequency economic reports to forecast. Still, the outlook darkened after last week’s increase in weekly initial jobless claims, which covered the week that the non-farm payrolls survey is conducted. Another increase, which is what the median forecast in the Bloomberg survey expects, is only momentarily going to get lost in the excitement around the GDP report.

The relatively light news day allows us to look a little closer at Mexico’s June trade data that was out yesterday. Mexico reported a record trade surplus of $5.5 bln. Yet, it is not good news. Mexico is hemorrhaging. The IGAE May economic activity index, reported at the end of last week, showed a larger than expected 22.73% year-over-year drop. The 2.62% decline in the month was nearly three times larger than economists forecast. With the virus still not under control, the government’s forecast for a 9.6% contraction this year is likely to be overshot. The record trade surplus was a function of a larger decline in imports (-23.2%) than exports (-12.8%). Auto exports are off more than a third (34.6%) this year, to $47.5 bln. Other manufactured exports are down 3.4% to $113.8 bln. Petroleum exports have fallen by nearly 42% in H1 to $8.0 bln. Agriculture exports edged up by 7.3% to $10.5 bln to surpass oil. The peso’s strength reflects not the macroeconomy but its high real and nominal interest rates in the current environment. Yesterday, the dollar fell below MXN22.00 for the first time this month. The June low was near MXN21.46.

The US dollar initially extended its losses against the Canadian dollar, slipping to CAD1.3330, just ahead of last month’s low (~CAD1.3315) before rebounding to almost CAD1.3400. The upside correction could run a bit further, but resistance in the CAD1.3420-CAD1.3440 area may offer a sufficient cap today. The greenback found support against the Mexican peso near MXN21.90 and bounced back to around MXN22.07. Resistance is seen near MXN22.20. The peso is up about 4.5% this month, but within the region has been bettered by Chile (~+6.75%) and Brazil (~+6.15%). The Colombian peso’s almost 2..2% gain puts it in the top 10 best performing emerging market currencies so far this month.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,$CNY,Currency Movement,Featured,HK,India,Mexico,newsletter