Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

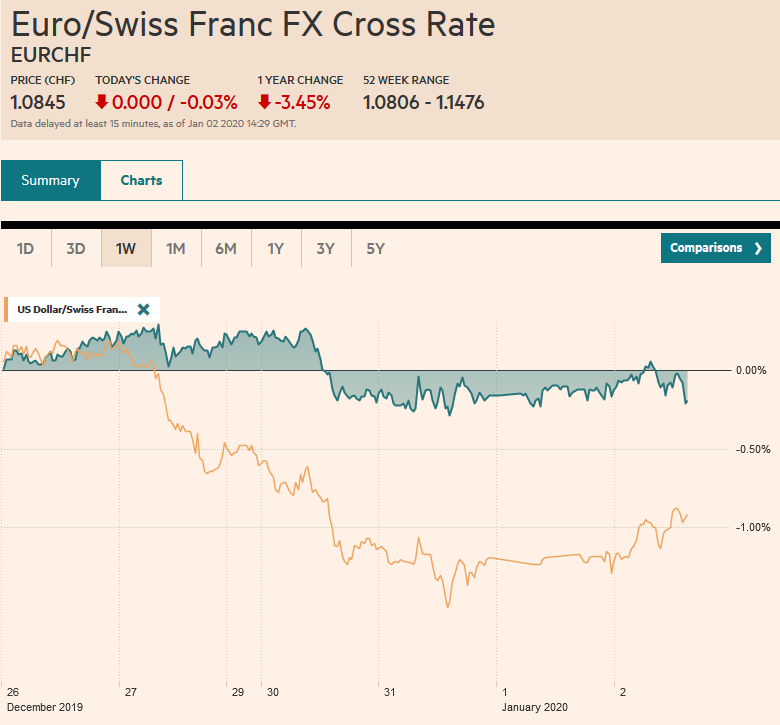

Swiss FrancThe Euro has fallen by 0.03% to 1.0845 |

EUR/CHF and USD/CHF, January 2(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

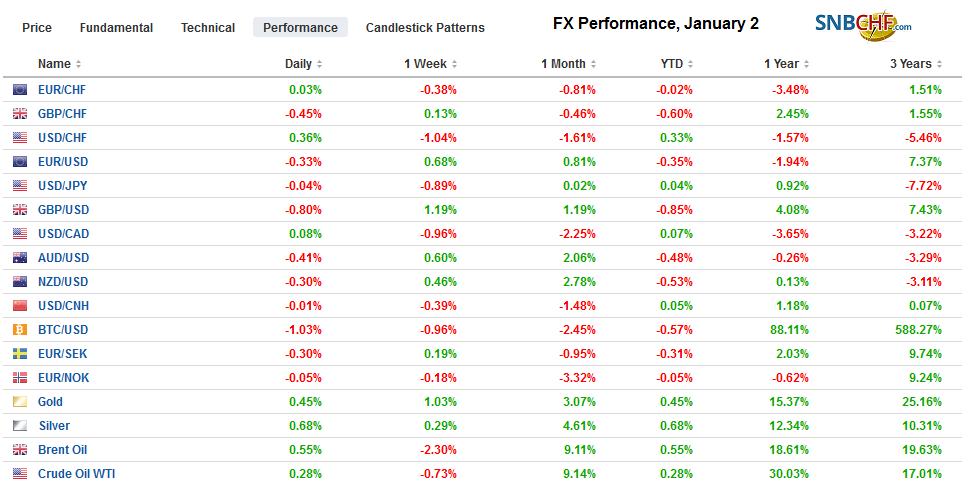

FX RatesOverview: Equities have begun New Year like, well, last year, with most Asia Pacific markets advancing, led by more than 1% gains in China, Hong Kong, and Thailand. Only South Korea and Indonesian markets fell. In Europe, the Dow Jones Stoxx 600 is up almost 1% in late morning turnover. US shares are trading higher as well, and the S&P 500 is up nearly 0.6%. Core benchmark 10-year yields are up 1-2 basis points, but the periphery and UK yields are up 3-5 bp. The dollar is firm against most of the major currencies, with the Antipodean and sterling leading the losses as the pre-holiday gains are pared. The JP Morgan Emerging Market Currency Index continues to edge higher. It has not fallen since December 20. Gold is in a tight range around $1520, and February WTI is flattish near $61.25. |

FX Performance, January 2 - Click to enlarge |

Asia PacificYesterday the PBOC announced a 50 bp cut in the required reserve ratio for bank effective Monday, January 6. The move had been hinted at in the Chinese media and by Premier Li Keqiang recently. The move will free up an estimated CNY800 bln (~$114.5 bln) and reduce banks’ funding costs, which in turn is expected to be passed on to corporate borrowers. This suggests the benchmark one-year Loan Prime Rate will likely fall when it is set later this month (January 20). The required reserves ratios are set currently at 13% for large banks and 11% for smaller banks, which remains among the highest in the world. There is scope for additional reductions in the coming year. Observers and investors debate over the reason that the PBOC is easing policy. Some argue it is due to the weakening economy, and others see a preemptive move ahead of the significant liquidity needs around the Lunar New Year (January). It does not have to be an either/or proposition. Chinese actions often appear designed to meet more than one policy objective. China’s Caixin manufacturing PMI slipped to 51.5 from 51.8 in November. It was a touch lower than expected. Recall that the official PMI was unchanged at 50.2. Other manufacturing PMIs in the region appear consistent with a gradual recovery in the area. South Korea’s manufacturing PMI improved for the third consecutive month and moved back above the 50 boom/bust level. So did Thailand and Taiwan. Malaysia made it back to 50, while India rose to 52.7 from 51.2. Indonesia was a notable disappointment, rising to 49.5 from 48.2, but Australia stands out for its decline to a new cyclical low of 49.2 from 49.9 |

China Caixin Manufacturing Purchasing Managers Index (PMI), December 2019(see more posts on China Caixin Manufacturing PMI, ) Source: Investing.com - Click to enlarge |

Japan’s markets remain closed for an extended holiday. The dollar remains within Tuesday’s range, roughly JPY108.50-JPY108.90. Rising equities and yields suggest the greenback can resurface above JPY109.00, but the participation remains light. Australia’s deadly wildfires and soft PMI may have encouraged some profit-taking after the run-up to around $0.7030, a five-month high on New Year’s Eve. Initial support is seen near $0.6980, while potential extends toward $0.6950. There was no evidence that the cut in requires reserves were part of an effort to weaken the yuan. The PBOC set the dollar’s reference rate at CNY6.9614, while the banks’ models projected an average CNY6.9622 fix. The price action of the Thai baht looks as if the central bank intervened to step its appreciation. It rose nearly 8% last year, with a particularly sharp gain at the start of the week, which it has not retraced.

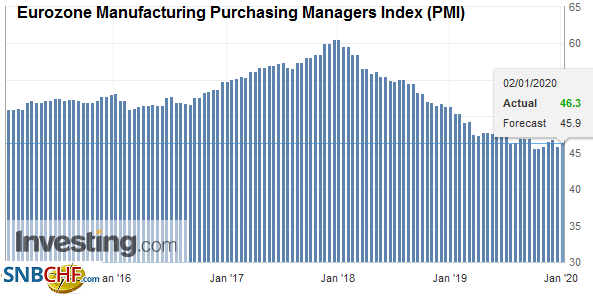

EuropeThe EMU manufacturing PMI was revised to 46.3 from 45.9 of the flash reading and 46.9 in November. This was the pattern for Germany and France. The final reading was not as poor as the flash, but it still showed weakness from November. The German report was revised to 43.7 form 43.4 flash and 44.1 in November. France edged up to 50.4 from the 50.3 flash estimate and 51.7 in November. Italy fell deeper into contraction territory at 46.2 from 47.6, and well below the 47.2 that was expected. The Dutch manufacturing PMI fell to 48.3 from 49.6, which was also weaker than expected. Spain, which could be on the verge of a new government, held in better at 47.4 from 47.5 in November. |

Eurozone Manufacturing Purchasing Managers Index (PMI), December 2019(see more posts on Eurozone Manufacturing PMI, ) Source: investing.com - Click to enlarge |

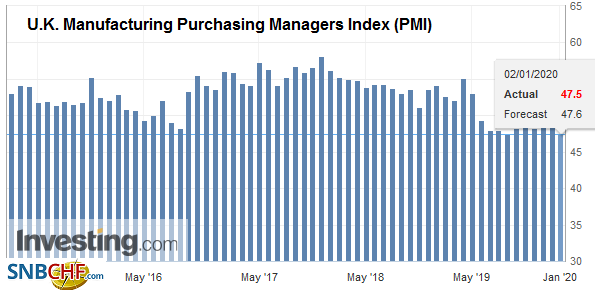

| The UK manufacturing PMI edged up to 47.5 from the initial estimate of 47.4, down from the November reading of 48.9. It has not been above 50 since April. Separately, reports suggest that China is temporarily blocking the planned London-Shanghai link for cross-listing shares in retaliation for some political offense, likely related to Hong Kong. Some accounts like it to comments over the detention of a former staff member of the consulate in Hong Kong. The details still appear murky. |

U.K. Manufacturing Purchasing Managers Index (PMI), December 2019(see more posts on U.K. Manufacturing PMI, ) Source: investing.com - Click to enlarge |

The euro reached almost $1.1240 on New Year’s Eve day and is pulling back today. It found a bid near $1.1190 in the European morning, though we would peg initial support closer to $1.1180. We suspect the risk extends toward $1.1150. Sterling made it to almost $1.3285 on the last day of 2019 trading and returned to nearly $1.3200 today. The first important retracement objective is not seen until closer to $1.3140.

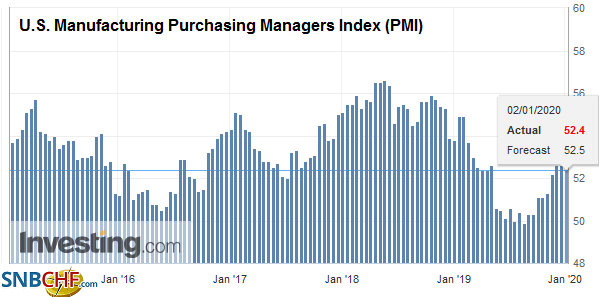

AmericaThe US reports the final manufacturing PMI for December. Recall that the initial estimate was at 52.5 from 52.6 in November. Weekly initial jobless claims are also on tap. Canada’s Markit manufacturing PMI will also be reported today. It has edged higher for three months through November after briefly dipping below 50 in August. Mexico reports its manufacturing and non-manufacturing PMIs today. They were both below 50 in November. |

U.S. Manufacturing Purchasing Managers Index (PMI), December 2019(see more posts on U.S. Manufacturing PMI, ) Source: investing.com - Click to enlarge |

President Trump announced on New Year’s Eve that the Phase One trade deal will be signed at a ceremony in the White House on January 15. Apparently, China’s Xi will not be attending but will send another senior official. Previously, the White House had indicated that Xi would probably attend and is not clear what has changed. Still, it would seem naive to think that it was a meaningless coincident or that the two schedules are so tight than a mutually agreed upon date was impossible to find. At some unspecified date in the future, Trump indicated he would go to Beijing to start Phase Two talks.

The Federal Reserve succeeded in dampening the year-end funding squeeze. The overnight repo rate rose to 1.88% on New Year’s Eve but fell back to 1.55% late in the session. Recall that end of 2018, it spiked to 6%. Banks took $25.6 bln in the Fed’s overnight repo operation on December 31 and coupled with $230 bln of term repo funding provided, there was $255.6 bln extra liquidity. The operation will be gradually unwinding in the coming weeks. At first, some observers thought the Fed would have to intensify its efforts, and possibly even purchases of long-term assets (rather than bills). However, now the debate has shifted toward how the Fed weens the market off its largesse.

The IMF’s Composition of Official Foreign Exchange Reserves (COFER) is the most authoritative source of international reserve data. It is reported at the end of every quarter with a quarter lag. The Q3 data were reported on December 31. The value of reserves is reported in US dollars, so exchange rates can and do influence the time series. In the third quarter, all the major currencies fell against the dollar, including nearly 4.2% decline by the euro and a 3.2% decline in sterling. The yen slipped by a minor 0.2%. Central banks hold roughly $11.66 trillion in currency reserves, of which the currency allocation of about $10.93 trillion is reported. And of those allocated reserves, $6.75 trillion are in USD-denominated investments. This is almost $27 bln less than at the end of Q2 19, but nonetheless, its share edged up to 61.78% from 61.49%. The dollar value of euro reserves fell by about $53.7 bln, and its share slipped to a little below 20.1%, its smallest share in a couple of years. The dollar value of yen holdings rose by $2 bln, and its share rose to 5.6%, its highest since 2000. The Chinese yuan depreciated by nearly 4% against the US dollar in the July-September, yet the dollar value of reserves increased by about $2.5 bln to $219.6 bln. Over the past year, its share of allocated reserves has edged higher to 1.8% to 2%.

The US dollar sold-off to record the lows for the year on New Year’s Day Eve against the Canadian dollar to almost CAD1.2950. It is consolidating today and holding below CAD1.30. The thin market conditions may have exaggerated the price action. The Mexican peso is firm near its best level since last April. The US dollar is trading between MXN18.85 and MXN18.95, essentially the range it was in before New Year’s. The Dollar Index is firm, but it remains near the five-month lows set earlier this week (~96.35).

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,$CNY,China,China Caixin Manufacturing PMI,COFER,Currency Movement,EUR/CHF,Eurozone Manufacturing PMI,newsletter,U.K. Manufacturing PMI,U.S. Manufacturing PMI,USD/CHF