Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

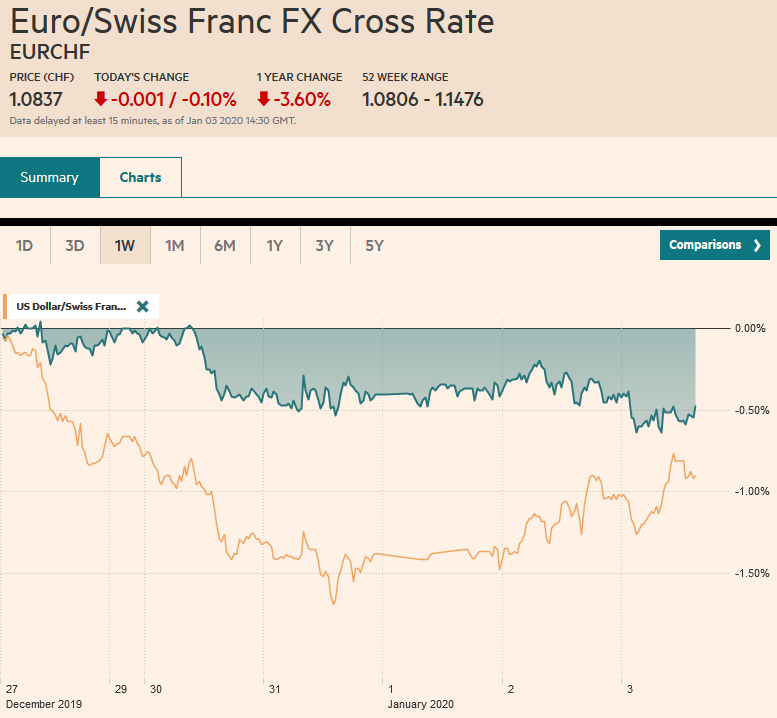

Swiss FrancThe Euro has fallen by 0.10% to 1.0837 |

EUR/CHF and USD/CHF, January 3(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: Iran’s Ayatollah Ali Khamenei has threatened “severe retaliation” for the US attacked that killed an important head of a force within the Islamic Revolutionary Guard. At the same time, reports indicate that North Korea’s Kim Jong Un is no longer pledging to halt its nuclear weapons testing and has threatened to unveil a new weapon. Meanwhile, Turkish forces have reportedly entered Libya. The geopolitical tensions are the key development that is hitting thin holiday markets and sapping the risk appetite that led to new record highs in the US equities yesterday. Asia Pacific equities were narrowly mixed, while Europe’s Dow Jones Stoxx 600 is giving back yesterday’s gain, and the US shares are trading heavily, with the S&P 500 looking around 1.5% lower. The US 10-year yield eased four basis points yesterday and is off another six today to 1.81%. European benchmarks are off 5-7 basis points. The US dollar has extended its recovery against most of the major currencies. The yen is a notable exception that the absence of local markets may have exaggerated the saw the dollar slip below JPY108 for the first time in two months. After rallying for eight consecutive sessions, the JP Morgan Emerging Market Currency Index fell yesterday and is extending its pullback today. It is at one and half week lows today. Oil shot up as investors fear disruptions. February WTI surged 3.5% to almost $64 a barrel where it peaked last April. Gold also approached last year’s high (~$1550). It has risen every session this week. |

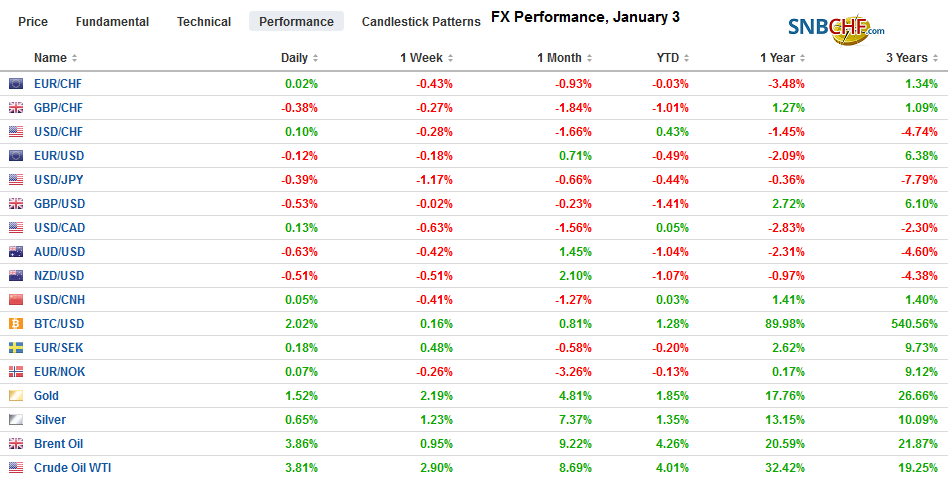

FX Performance, January 3 - Click to enlarge |

Asia Pacific

The PBOC set the dollar’s reference rate at CNY6.9681 today. The bank models average was about CNY6.9668. There does not appear to be any signal of a policy change following the announced cut in reserve requirements that go into effect on Monday and amid expectations for further easing of financial conditions ahead of the Lunar New Year toward the end of the month. Separately, but not unrelated, China has rebased the basket its uses (CFETS, the China Foreign Exchange Trade System) to monitor the yuan from 2015 trade flows to 2018. The net effect is to reduce the dollar’s weight to 21.59% to 22.40%. The euro’s share rose to 17.40% from 16.34%, and the Hong Kong dollar’s share was shaved to 3.57% from 4.28%. Given the HK dollar’s peg to the US dollar, reducing its share is also reducing the greenback’s impact. The CFETS weightings are used by economists to estimate where the dollar reference rate will be set. The effect is seen as minor.

The thin market conditions (remember last year’s flash crash?) and the geopolitical news gave the yen a shove higher. The dollar found support in late Asia/early Europe near JPY107.90. It briefly traded a bit lower in early November. The markets frequently seem to exaggerate geopolitical risks. Initial resistance is seen near JPY108.20. There are nearly $1.8 bln in options struck in the JPY108.50-JPY108.56 area that expire today. The Australian dollar peaked on New Year’s Eve near $0.7030 and has been beaten back to about $0.6935 today. The $0.6925 area corresponds to a (38.2%) retracement of last month’s gains, and the 20-day moving average is a bit lower (~$0.6915). The disastrous wildfires are thought to bring forward fiscal support, but the economic consequences are still be worked through.

Europe

Next week, the EMU’s first estimate of December CPI will be reported. We see the base effect and higher oil prices as spurring an inflation scare, and we suspect it has already begun and will continue through February. The November 2018 CPI fell 0.6% while the November 2019 report eased 0.3%. In December 2019, eurozone’s CPI was flat, and a small increase will boost the year-over-year reading its highest level since last April (1.7%).

France reported December’s CPI today. It rose 0.5% for a 1.6% year-over-year pace. This followed a 0.1% increase in November and a 1.2% year-over-year rate. German states are reporting, and shortly, the national estimate will be available. The EMU harmonized calculation may see a 0.5-0.6%% increase that would lift the year-over-year reading to 1.4%-1.5% after 1.2% in November.

Turkey’s CPI bottomed in October, near 8.55%. It rose to 10.56% in November, and today it reported December’s rate at 11.84%. The median forecast in the Bloomberg survey forecast was 11.5%. Its key one-week repo rate is at 12.00, which implies practically zero real rates, and in turn, limits further rates cuts by the central bank without putting at risk the currency and future inflation. The US dollar extended its recent gains against the lira, and near TRY5.97, it is at its best level in several months.

The euro reached almost $1.1240 on New Year’s Eve. It fell about 4/10 of a cent yesterday and another 4/10 of a cent today to trade to almost $1.1130. The 200-day moving average and the (38.2%) retracement of last month’s gains is found around $1.1140. The next retracement objective is near $1.1110. Sterling’s New Year’s Eve peak was near $1.3285. Yesterday’s high was about $1.3265 before selling off to test the 20-day moving average near a little below $1.3120. Today it approached $1.3065 in the face of the dollar’s broad strength and the soft consumer credit and construction PMI. There is an option for about GBP400 mln at $1.30 that expires today. Ahead of there, we see chart support near $1.3050.

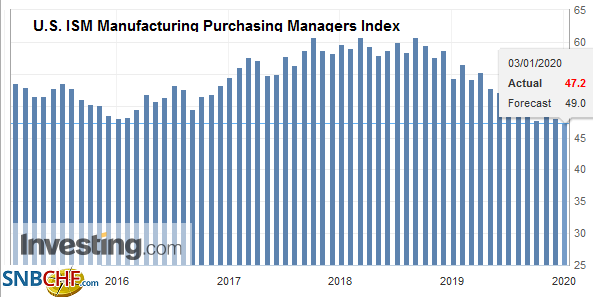

AmericaThe US calendar is packed today. Although many observers would suggest the December ISM is the most important of today’s reports, we’d like to make a case for the December auto sales, as the data point with the most significance. The manufacturing ISM covers a modest part of the economy. It has been below the 50 boom/bust level since the August report. It is likely to remain below there even if it creeps up. Moreover, Boeing’s production cuts in Q1 will take a toll going forward. The auto sales speak directly to the 70% of the economy driven by the consumer and may help set the tone for December retail sales. Through November, US auto sales have averaged 16.93 mln vehicles at a seasonally adjusted annual rate. In the first 11 months of 2018, the average was 17.12 mln. Separately, construction spending is expected to have bounced back in November after falling 0.8% in October. |

U.S. ISM Manufacturing Purchasing Managers Index (PMI), December 2019(see more posts on U.S. ISM Manufacturing PMI, ) Source: investing.com - Click to enlarge |

The FOMC minutes will attract attention. Investors know that 13 of the 17 Fed officials anticipate that no change is rates will be necessary this year. The real interest will be on color around the repo operations. There is hope that more details about how the Fed will approach the challenge. Is it close to establishing a permanent repo facility to match the reverse repos? What about the $60 bln a month of T-bill purchases that are to run into Q2? The answers may not be forthcoming in the minutes, primarily because the Fed itself probably does not have the answers yet. The playbook is still being written. Separately, five Fed officials speak today: Barkin, Daly, Evans, Kaplan, and Brainard. Only the latter two vote (The voting power rotates to Kaplan and Brainard is a Governor).

The Canadian dollar is pulled in both directions. The higher oil prices tug higher will the risk-off mood points lower. The net effect has been to sideline the Loonie. The greenback is consolidating the recent losses that drove it below CAD1.30. We like the dollar higher, but it needs to rise above CAD1.3010 and ideally CA1.3040 to be anything noteworthy. The risk-off mood dominates the trading of the Mexican peso today. The dollar was testing the MXN18.83 area yesterday, and today is pushing above MXN19.00. It has not closed above MXN19.00 since December 13. The technical indicators are bottoming, and the risk in the coming sessions may extend toward MXN19.20.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,$CNY,EUR/CHF,federal-reserve,Iran,Korea,newsletter,PBOC,Turkey,U.S. ISM Manufacturing PMI,USD/CHF