Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

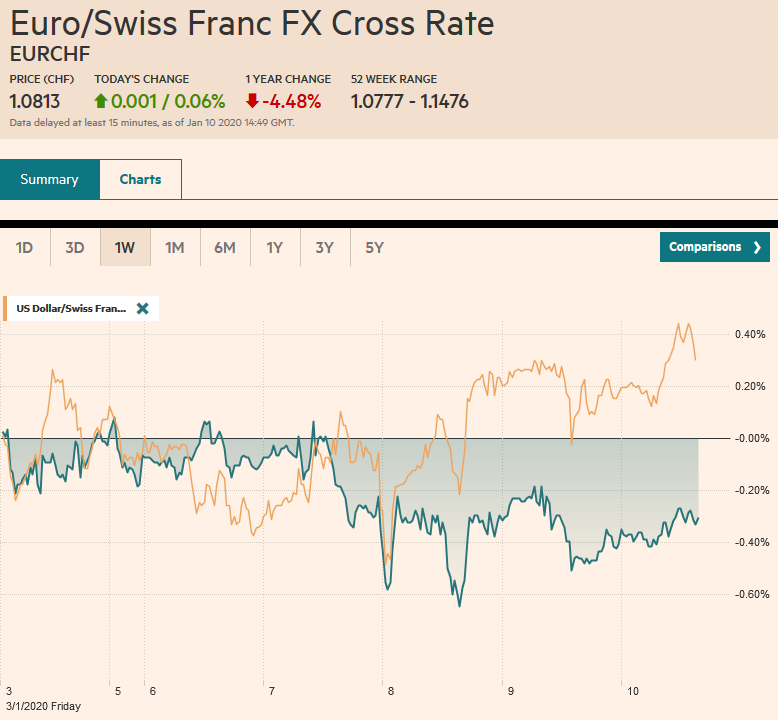

Swiss FrancThe Euro has risen by 0.06% to 1.0813 |

EUR/CHF and USD/CHF, January 10(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The first full week of 2020 is ending on a quiet note, pending the often volatile US jobs report. New record highs US equities on the back of easing geopolitical anxiety is a reflection of greater risk appetite that is evident across the capital markets. Asia Pacific equities mostly rose today, though Chinese shares and a few of the smaller markets saw small losses. The MSCI Asia Pacific Index rose about 0.2% on the week, the sixth consecutive weekly advance. European equities are up small for the fourth straight session. It is also the fourth weekly gain in the past five weeks and is sitting at new record highs. US shares are firm, and the Dow Jones Industrials are knocking on the 29000-level. Since the start of Q4 19, the S&P 500 has fallen in just three weeks. Benchmark 10-year yields are softer in Europe, with Italy’s six basis point decline leading the way. The US 10-year is little changed on the day near 1.85%, holding on to around a five basis point increase on the week. This week’s nine basis point rise in the German 10-year yield was the largest rise among the major bond markets. The dollar remains firm against nearly all the major currencies. Although the Australian dollar is showing some resiliency today, the greenback is having its best week in about two months. The JP Morgan Emerging Market Currency Index is a little heavier for the second consecutive session, but on the week, it is up by about 0.25% and is the fifth week in the past six that it has appreciated. Gold continues to unwind its recent gains. After reaching a high near $1611 on the Middle East developments, it is trading below $1550 and is snapping a four-week rally. Oil, too, is paring its gains and is lower for the fourth consecutive session. February WTI hit $65.65 before reversing lower. It fell to nearly $58.65 yesterday and is consolidating above $59 today. |

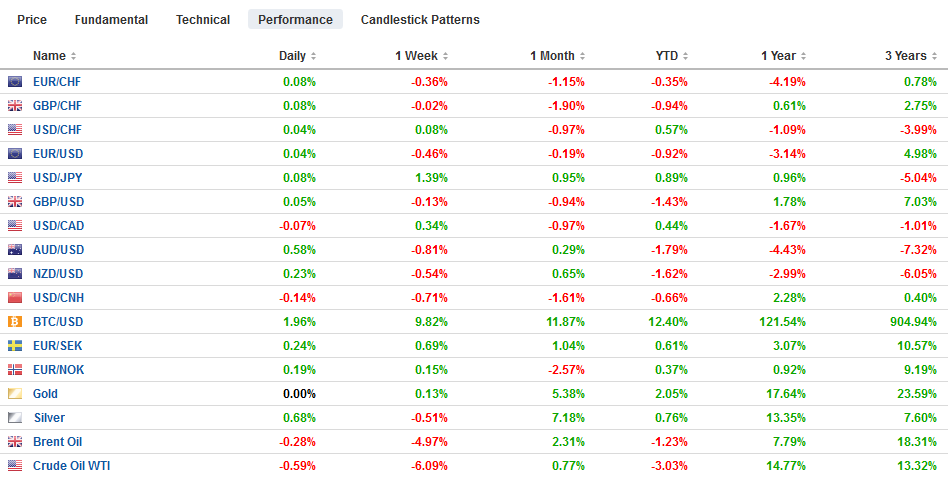

FX Performance, January 10 - Click to enlarge |

Asia Pacific

Japanese household spending fell 2% year-over-year in November. This was a little more than expected but showed what is likely to be a gradual recovery from the sales increase shock. Spending had collapsed by 5.1% in October. The government efforts to boost spending do appear to have mitigated the slump compared with the last time the sales tax was hiked (2014). Nevertheless, the Japanese economy seems to have contracted sharply in Q4 20, and the latest Bloomberg survey showed a median forecast of a 3.7% decline in overall output. Last month, the survey had a median forecast of a 2.6% contraction.

Australian retail sales in November rose by 0.9%, twice what economists had expected, and the October series was revised to 0.1% from flat. The November increase was the strongest in two years. The risk is that the “Black Friday” sales brought forward the holiday purchases, leaving December vulnerable to disappointment. Separately, the AiG Services Index fell to 48.7 from 53.7., the weakest since July. The market leans slightly toward a 25 bp cut when the Reserve Bank of Australia meets next on February 4.

The dollar has jumped from a nearly three-month low against the yen in the middle of the week (~JPY107.65) to test JPY109.65 in the European morning. So far today, it has been stuck in less than a 20-tick range. There are options for about $800 mln struck in the JPY109.40-JPY109.50 area that expire today and one at JPY110.20 for $1.2 bln. The dollar has not been above JPY110 since last May. Since the middle of the week, the Australian dollar has found a base near $0.6850, but it is showing little enthusiasm to the upside. The 200-day moving average is a little below $0.6900, and a close above it would lift the tone. The Chinese yuan is trading firmer and is near a five-month high, with the dollar just above CNY6.92.v Lastly, we note that the Indonesian rupiah is leading Asian and emerging market currencies today with around a 0.6% gain (~1.15% on the week) following comments by the central bank that seemed to signal acceptance of a stronger currency.

Europe

Following the better than expected German industrial production data yesterday, France, Italy, and Spain reported relatively good figures today, supporting ideas that the troubled sector is stabilizing. French industrial output rose 0.3%, a little more than expected. Manufacturing output slipped by 0.1%, but the October series was revised to 0.6% from 0.5%. Italian industrial production rose 0.1%, which was not only better than expected but was the first increase since August. Spain’s industrial output jumped by 1%, the most since April. Economists had forecast a 0.2% rise. Taken together, it appears to be upside risk to next week’s aggregate report where a 0.5% gain had been expected.

The Brexit bills passed the House of Commons yesterday, and the House of Lords will take the measures up next. However, this is largely a formality. Meanwhile, the Bank of England may be closer to cutting rates that the two dissents at the past two meetings would suggest. Governor Carney hinted as much yesterday, and MPC member Tenreyro suggested that she could be persuaded to cut rates if the economic data does not improve. This is slightly different than favoring a cut if conditions deteriorate.

The euro peaked near $1.1240 on New Year’s Eve and is testing the $1.1090 area today in Europe. The (61.8%) retracement of the rally since last November’s $1.0980 low is found near $1.1080 today. The technical condition is deteriorating, and a break of the shelf created in the second half of December near $1.1065 could see the single currency test $1.10 next week. The $1.1100 area that was support may now act as resistance, helped by an option for almost 840 mln euros. Sterling is consolidating within yesterday’s range and remains above $1.30. There is an option for nearly GBP600 mln at $1.3065 that expires today.

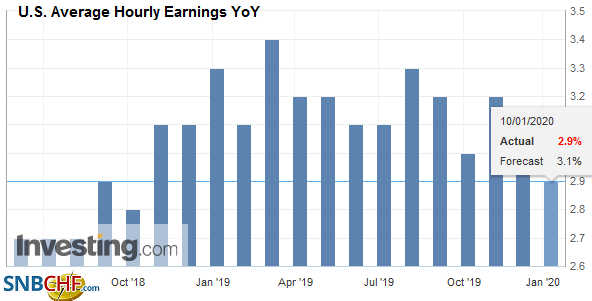

AmericaThe US and Canadian employment reports dominate the North American session. Although the Bloomberg survey shows a median forecast of 160k increase in US nonfarm payrolls after the 266k increase in November, the whisper number is higher, closer to 200k on the back of the strength of the service sector. |

U.S. Average Hourly Earnings YoY, December 2019(see more posts on U.S. Average Hourly Earnings, ) Source: investing.com - Click to enlarge |

| Market psychology is such that there may be an asymmetrical risk. The market is more likely to shrug off a soft report. This sense has been reinforced by the numerous Fed comments that suggest that officials will look past a disappointing report. |

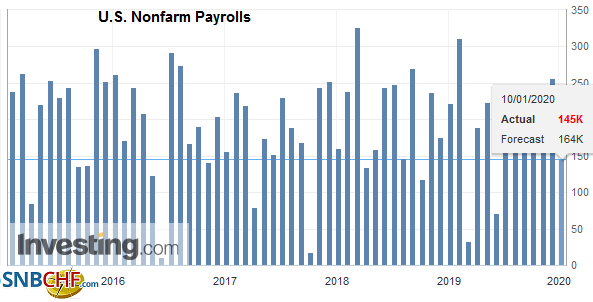

U.S. Nonfarm Payrolls, December 2019(see more posts on U.S. Nonfarm Payrolls, ) Source: investing.com - Click to enlarge |

| Canada’s real sector data has disappointed recently, and the streak may have begun with the November employment data that saw a heady 71.2k loss of jobs, which included nearly 38.5k full-time positions. Economists look for a bounce of about 25k jobs, but another loss of jobs would likely bring back talk of a rate cut. The Bank of Canada meets on January 22, and there is practically no chance of move then. However, as it did in Q4, it may soften its neutrality, but in addition to a soft employment report, weaker price pressures may be needed to stir the market. |

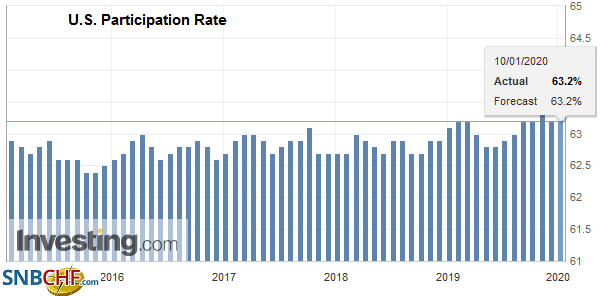

U.S. Participation Rate, December 2019(see more posts on U.S. Participation Rate, ) Source: investing.com - Click to enlarge |

Mexico reports November industrial output. It is expected to rise by 0.9%, which would snap a two-month contract. Such a rise would be the largest since January. Easing price pressures and the weak economy has the market expecting a rate cut when the central bank meets again near the middle of next month. Brazil reports its IPCA inflation, and unlike Mexico, price pressure appears to have bottomed, and this leaves the central bank little choice but to stand pat as the Selic rate is at a record low of 4.50%. The December IPCA measure may put the CPI at near 4.25%, leaving real rates just above zero, which does not appear sufficient to support the currency.

The US dollar spiked above CAD1.3100 yesterday after bottoming near CAD1.2950 earlier in the week. Initial support now is seen near CAD1.3050. Above CAD1.3100, the next technical target is near CAD1.3140 and then CAD1.3180. Meanwhile, the Mexican peso remains firm. The peso is one of the strongest emerging market currencies this week, gaining a little more than 0.5% against the dollar. It appears to be the fifth week in the past six that the greenback has weakened against the peso. The high real and nominal yields attract savings and carry trades.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,Canada,Currency Movement,EMU,EUR/CHF,Indonesia,jobs,newsletter,U.S. Average Hourly Earnings,U.S. Nonfarm Payrolls,U.S. Participation Rate,USD/CHF