Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

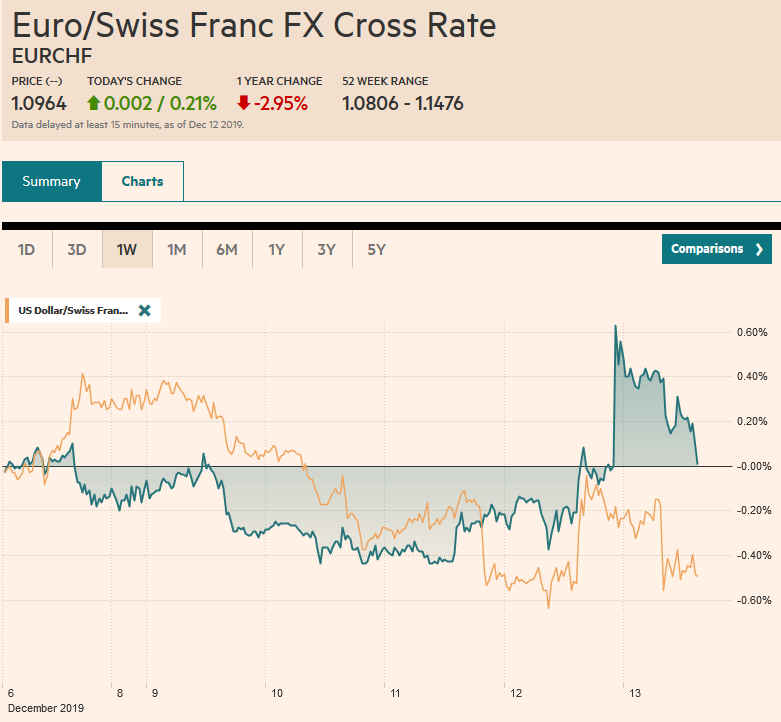

Swiss FrancThe Euro has risen by 0.21% to 1.0964 |

EUR/CHF and USD/CHF, December 13(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The combination of a US-China trade deal and exit polls showing the Tories securing a majority in the House of Commons boosted risk assets, sent sterling flying, and the euro sharply higher. Separately, the Fed stepped up its efforts to make as smooth as possible funding over the turn of the year. Led by more than 2% gains in Hong Kong and the Nikkei, and more than 1% rallies in China and South Korea, the MSCI Asia Pacific Index rose the most in six months today. Europe’s Dow Jones Stoxx 600 gapped higher and is up around 1.6%, the most in a couple of months in the European morning. US shares are trading firmer, and the S&P 500 is poised to gap higher as well. Benchmark 10-year yields in Asia played catch-up to the rise in the US yesterday. Core European bond yields are up 2-3 bp today, while the US 10 year is consolidating around 1.88%. Peripheral European bonds have been supported by the demand for risk assets, and yields are lower there, led by a 2 bp decline in Italy. The dollar is softer against nearly all the world’s currencies today. Sterling itself spiked to a little more than $1.35 on the immediate news and pushed back to about $1.3360 in the European morning, where new bids were found. Gold is firm but within well-worn ranges. January WTI is pushing toward $60 that capped it last week. |

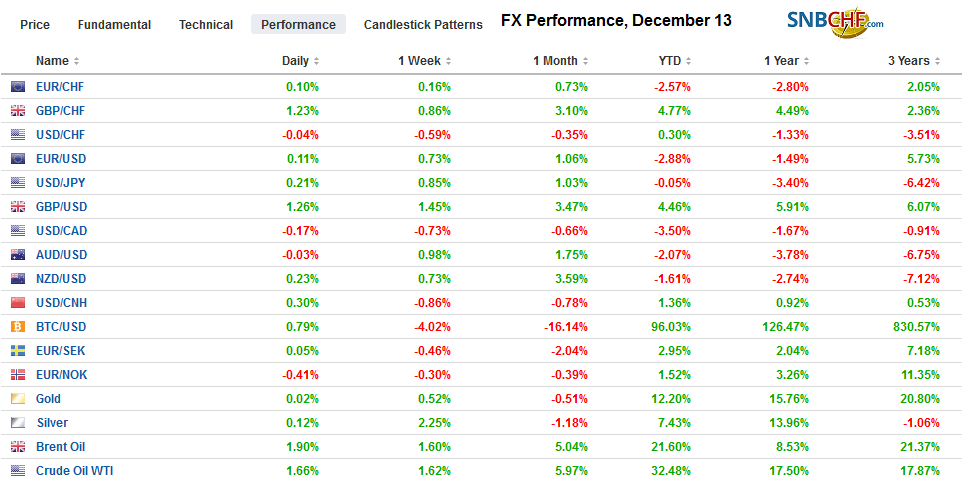

FX Performance, December 13 - Click to enlarge |

Asia Pacific

Details of the trade agreement that won the approval of President Trump are not known, but the simple fact that a deal was reached and that the tariffs that were threatened for December 15 would not be imposed helped spur a rally in risk assets in North America yesterday. The broad outlines include a commitment from China to buy much more US agriculture than ever before (~$50 bln) and step up protection of intellectual property in exchange for a 50% reduction in existing US tariffs and not implementing the December 15 levies. The offshore yuan (CNH) rallied by over 1%, and the dollar fell to around CNH6.9230, its lowest since August 1. Today, it has bounced back to about CNH6.9850-CNH6.9900. The dollar was bumping against the CNY7.0450 area most of the week but finished yesterday near CNY6.9850. It fell to CNY6.9600 today before recovering to little changed levels on the session.

Japan’s Tankan Survey showed a deterioration of sentiment among large and small manufacturers, while the non-manufacturing sector proved more resilient. The large manufacturer sentiment reading fell to 0 from 5. It is the lowest in six years, and the outlook for the next quarterly read also fell to 0. The large non-manufacturer results slipped to 20 from 21, which was better than expected. This pattern was repeated among small businesses. Manufacturing sentiment slumped more than expected, and small non-manufacturers saw a slight decline and fared better than economists forecast. The results reinforce expectations that the BOJ will reduce its economic assessment at next week’s meeting. A large supplemental budget is already in the works.

On Wednesday, the dollar settled near JPY108.55. Yesterday, it reached JPY109.45 and today, JPY109.65. The high earlier this month was seen around JPY109.75. The intraday technical readings have not matched the strength of spot move. Although it looks stretched, the daily technical readings are constructive, and the greenback appears poised to rise above JPY110 next week for the first time since May. The Australian dollar finished last week near $0.6840. After soft start to the week, with declines on Monday and Tuesday, the Aussie has rallied strongly and today, reached $0.6940 before consolidating. It rose above the 200-day moving average (~$0.6910) that has held back rallies since March 2018. There are options for nearly A$1.4 bln struck between $0.6885 and $0.6899 that expire today.

Europe

The Tories scored an impressive victory. A majority of about 47 seats was secured, and the Tories won seats that were strongholds of Labour for a couple generations. It is the biggest margin since Thatcher in the late 1980s. Labour leader Corbyn resigned, and Lib Dem leader Swinson lost her seat, and the party will also pick a new leader. The Scottish National Party also turned in a strong showing, and it may be difficult to resist a new referendum at some point. Brexit will take place by the end of January, and the focus will shift to three things: new negotiations with the EU over the future trade relationship, the state of the economy, with fiscal stimulus promised, and Carney’s replacement at the Bank of England. Carney is to step down at the end of January, and Shafik, the former deputy at the BOE, is seen to be a favorite.

Lagarde got glowing reviews for her debut press conference as President of the ECB. The market voted with their feet in the sense that she statement and answers did not spark much movement. There were some minor (0.1 percentage point adjustments to some near-term forecasts, but her assessment was consistent with the tone and path of the ECB. She demonstrated knowledge of a number of technical issues. Lagarde comporting herself well and left no doubt about her inclusive and collaborative style, which is likely to help ease some ruffled feathers. The strategic review, which has already begun, is projected to take more of next year to complete (a little longer perhaps than expected). She seemed enthusiastic and a little upbeat by suggesting that several economic measures appeared to have stopped worsening and that lending to non-financial businesses and households continued to grow. While there have been some press pieces suggesting officials are becoming increasingly skeptical of the merits of negative interest rates, Lagarde pushed back and argued that it has been an important tool.

The euro has not fallen this week. It is up about 0.5% today (at about $1.1185) to bring the week’s gain to about 1.1%. It has jumped above the 200-day moving average for the first time since July. The euro has taken out the October and November highs and is knocking on $1.1200, its best level in four months, where a roughly 610 mln euro option is set to expire today. The market appears a bit stretched, and the upper Bollinger Band (two standard deviations on top of the 20-day moving average) is by $1.1155. As we anticipated, sterling was subject to buy the rumor sell the fact. It spiked above $1.35 on the exit polls but drifted lower after early Asia and saw $1.3360 in the European morning. Stronger chart support is seen in the $1.3200-$.3230 area. Some chunky options expire today. At $1.34, there is are options for GBP1.4 bln, and at $1.3450, there are another GBP1 bln in expiring options. Lastly, there are options for about GBP450 mln at $1.35. Meanwhile, the euro has been sold to three-year lows against sterling near GBP0.8275. It, too, is consolidating now below GBP0.8350, where an option for roughly 500 mln euros will be cut today. There is another option for 425 mln euros at GBP0.8300 that also expires today.

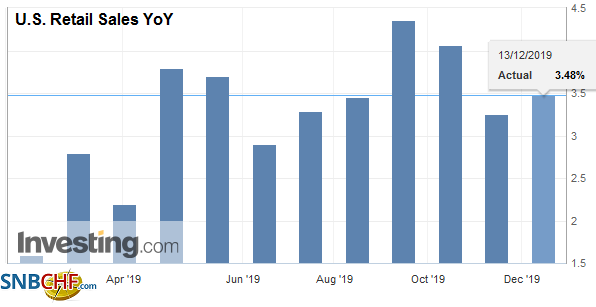

AmericaAlthough Powell gave no indication at the press conference that followed the FOMC meeting, the Fed announced yesterday that in addition to term repo operations that have already been announced, it would offer as much as $50 bln in a 32-day operation Monday. It also will offer forward settled overnight repo on December 30. That means that if all of the repos were fully subscribed, the Federal Reserve would be providing almost $500 bln over the turn of the year. The US reports import and export prices, but the interest is with the November retail sales report. A solid number is expected. The median forecast in the Bloomberg survey calls for a 0.5% gain in the headline figure after a 0.3% rise in October (following a 0.3% decline in September). A 0.5% gain would match the average through the first ten months of the year. The components that are used for GDP calculations rose by 0.3% in October (-0.1% in September) and are expected to match that in November. The average monthly gain this year is 0.7%. It was mostly front-loaded in Q1. Since March, only one month, July, was matched the 0.7% average. The quiet period around the FOMC meeting has ended, and the NY Fed’s Williams will be the first to speak. He gives a lecture to students late in the NY morning at the Borough of Manhattan Community College. |

U.S. Retail Sales YoY, November 2019(see more posts on U.S. Retail Sales, ) Source: investing.com - Click to enlarge |

The US dollar is testing support near CAD1.3150, where a $770 mln option is set to expire later today. That area, as we have noted, also corresponds to a (61.8%) retracement of the greenback’s rally since the end of October. A break signals potential toward CAD1.3100 next. The risk-off impulses have seen the US dollar extend its losses against the Mexican peso. Today’s loss is the eighth session of the past 10 that the dollar fell against the peso, and the decline has brought it back to MXN19.00, which it has not traded through since late July. It appears to have traded as low as MXN18.9960 in early Asia. The Dollar Index slumped to about 96.70 late yesterday. It was the lowest level since early July. It is consolidating in a narrow range now (~96.72-96.92). The October lows around 97.10-97.15 may offer initial resistance.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,$CNY,Brexit,EUR/CHF,federal-reserve,newsletter,Trade,U.K.,U.S. Retail Sales,USD/CHF