Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

The US dollar fell last month in response to the disappointing non-farm payroll report. However, in general, the jobs report is not the market mover that it was in the past. With unemployment is at cyclical lows of 4.1% and poised to fall further. Weekly jobless claims and continuing claims at or near lows in a generation, though over qualification is more difficult than previously.

The monthly net job creation is a volatile number, the underlying churn–people taking new jobs and leaving old jobs–is much larger. The focus in recent months has shifted from the understood to be healthy trend job growth to average hourly earnings. Many officials and economists believe that headline inflation converges to core inflation and core inflation converges to wage growth.

Average hourly earnings are one measure of labor income, and as the market has come to appreciate, it is a particularly slow-moving one. Over the last 12 and 24-months, it has averaged a year-over-year rate of 2.6%. It averaged 2.7% in Q1 18. A 0.2% rise in April is needed to keep the year-over-year pace steady. The FOMC statement recognized that inflation was near its target, but it was anticipating an acceleration. That is the view of wages as well.

Although the Fed recognized the fact that Q1 GDP did not match the pace in Q417, there was no indication that the Fed was not looking past it. Investors learned this week that economy appears not to have enjoyed much momentum at the start of Q2. The manufacturing ISM fell to its lowest level since last July, while non-manufacturing ISM is at the low of the year. The market continues to price in with nearly 100% confidence a June rate, and barring dramatic shock (which neither the weekly jobless claims nor the ADP signaled), it is unlikely to be swayed otherwise by the jobs data.

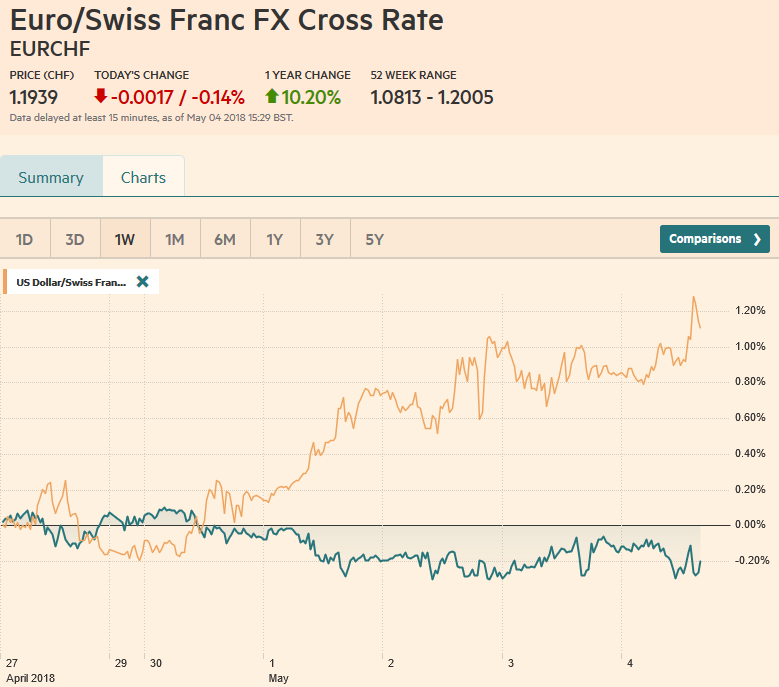

Swiss FrancThe Euro has fallen by 0.14% to 1.1939 CHF. |

EUR/CHF and USD/CHF, May 04(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesUK Prime Minister May is in a pickle. We had anticipated a political crisis around the time of the local elections. However, Labour does not appear to have scored the kind of victory that would have encouraged a leadership challenge. The precipitating factor of May’s woes, as they mostly have been since taking office is Brexit. Those forces that want to stay in a customs union with the EU have been making a stand in the House of Lords, including this week, adding an amendment to the Withdrawal Bill that rejects a hard border with Ireland. In the House of Commons, a rump of pro-Europe Tories could bolt, denying May of a majority when the bills return to it. If she was just pressed by the pro-EU forces that would not be much of an issue. What makes it particularly difficult is that what may be acceptable to the House of Commons may not be acceptable to May’s senior ministers. Several, including the newly appointed Javid as Home Secretary, reportedly rejected the Prime Minister’s compromise plan on the customs union. The Bank of England meets next week. Today’s news that UK auto registrations (proxy for sales) rose in March (10.4%) for the first time since last March is not sufficient to offset the string of disappointing data. The market has completely unwound the rate hike expectations, with the OIS currently implying less than a 10% chance. Sterling made its post-referendum high on April 17 near $1.4375. It reversed lower that and had tumbled about 8.3 cents through yesterday’s low just below $1.3540. This roughly 5.9% decline may exaggerate the economic impact. On a trade-weighted basis, sterling fell almost 2.7%. It is near the 100-day moving average as it returned to levels seen in mid-March. |

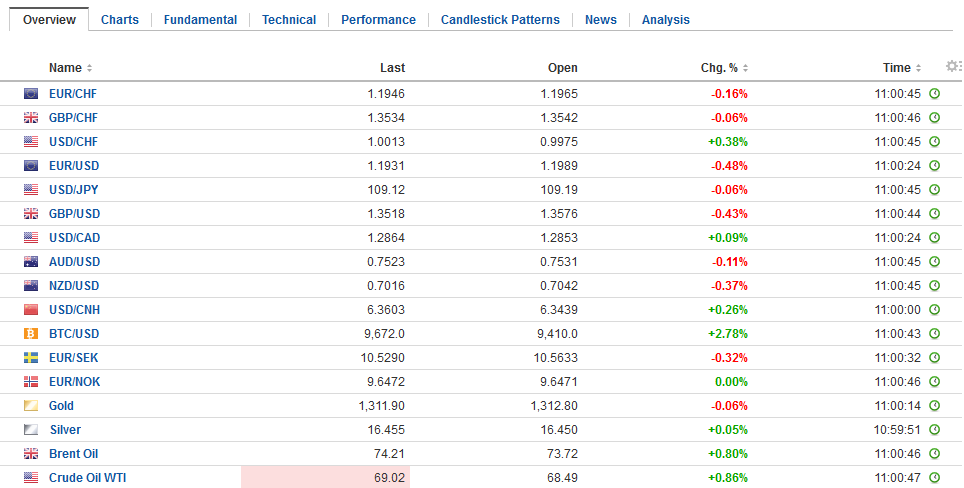

FX Daily Rates, May 04 - Click to enlarge |

| The Reserve Bank of Australia lifted its core inflation forecast and signaled that while rate would eventually need to increase, it did not anticipate doing so in the near-term, which the market suspects means late this year at the earliest, and more likely next year. The inflation forecast was lifted to 2.0%, the lower end of the central bank’s 2%-3% range, from 1.75%, and where core inflation stood in Q1. The RBA did not project another increase in core inflation until 2020, when it is seen at 2.25%.

The Australian dollar initially rallied on the news. It reached $0.7560, a four-day high but met a wall of sellers and fell back below $0.7520. Support is seen in the $0.7480-$0.7500 area. The dollar has risen broadly in recent weeks, and the Chinese yuan is no exception. This is the third consecutive week that yuan has fallen, and it has depreciated in four of the last five weeks. This puts the dollar at the upper end of a three-month trading range. Still, the yuan is among the strongest of the Asian currencies over the past month, off a little less than 1%, and stronger than all the majors, but the Canadian dollar. This means that the yuan has strengthened against its basket. Although the yuan has depreciated against the dollar, we do not see it as a sign that China is using the foreign exchange market to express its displeasure with the US provocations. |

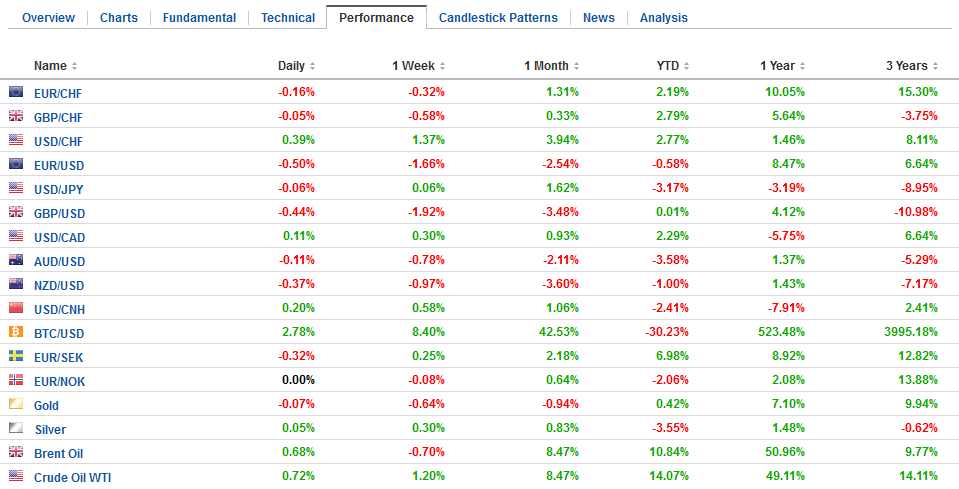

FX Performance, May 04 - Click to enlarge |

|

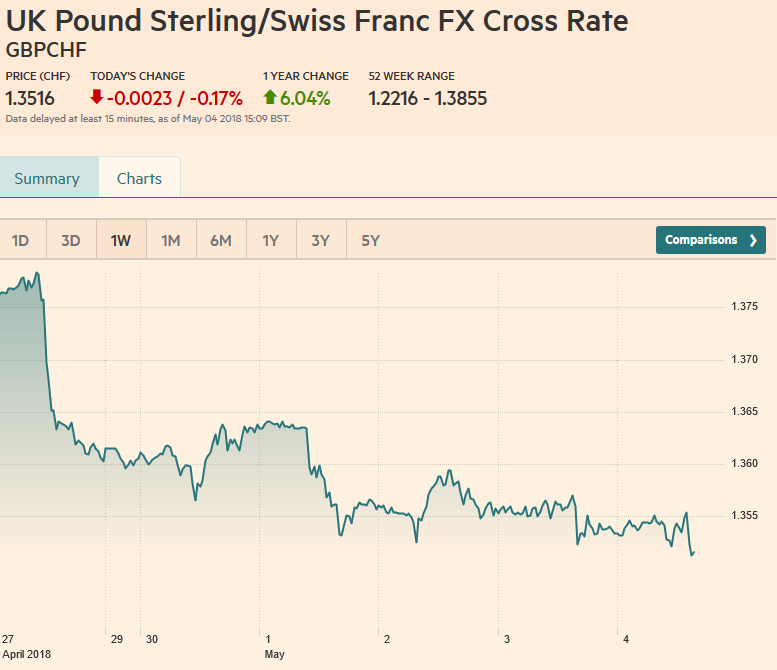

In recent weeks the Swiss Franc has been making up some of the losses witnessed against sterling over the last 12 months. CHFGBP 2 weeks ago was 0.7225 and currently sits at 0.7390. To put this into monetary terms a 200,000 Swiss Franc transfer into sterling generates clients an additional £3,300 and I expect this trend could continue in the weeks to come. For Swiss Franc sellers, I wouldn’t get to excited as I don’t believe we are experiencing Swiss Franc strength, in fact the improvement in exchange rates comes from the demise of sterling. Last month UK economic data disappointing which sent shock waves through the UK economy and the Bank of England cut the chances of an interest rate hike in May. Retail sales, inflation and GDP all took a tumble. Many forecasters are suggesting the bad weather has been a contributing factor, therefore if the weather picks up there is an argument this could be a blip and we have a strong month and the pound start to gain momentum. However with the Brexit negotiations on going and the all important custom union debate continues to drag on, I expect the pound is going to fall further, which is great news for Swiss franc sellers buying sterling. |

GBP/CHF, May 04(see more posts on gbp-chf, ) Source: markets.ft.com - Click to enlarge |

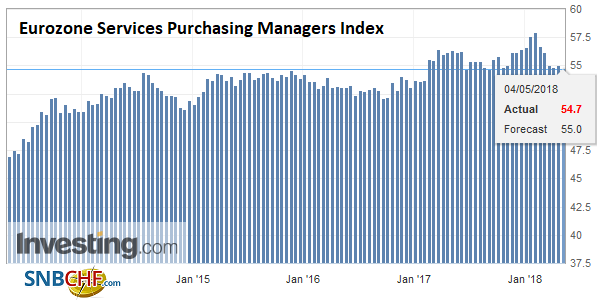

EurozoneThe eurozone disappointments continued to mount this week as we can only suspect it reinforces the cautiousness Draghi spoke of recently, while doing little to bolster confidence which was to temper the cautiousness. Yesterday we learned that while price pressures eased in April, core prices retreated to 0.7%, just above the cyclical low, prior to the asset purchases, of 0.6%. The negative news has continued as the flash service PMI, and composite readings were revised lower, and Germany, the region’s engine as part of the problem. The net result is that the EMU service PMI was revised to 54.7 from 55.0 seen in the flash report. |

Eurozone Services Purchasing Managers Index (PMI), May 2013 - 2018(see more posts on Eurozone Services PMI, ) Source: Investing.com - Click to enlarge |

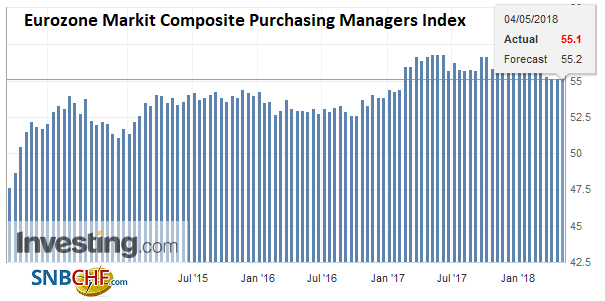

| The composite was shaved to 55.1 from 55.2, which is also where it stood in March. To put this in perspective, consider that the composite averaged 57.0 in Q1 18 and 57.2 in Q4 17. It is the lowest since January 2017. |

Eurozone Markit Composite Purchasing Managers Index (PMI), Jun 2013 - May 2018(see more posts on Eurozone Markit Composite PMI, ) Source: Investing.com - Click to enlarge |

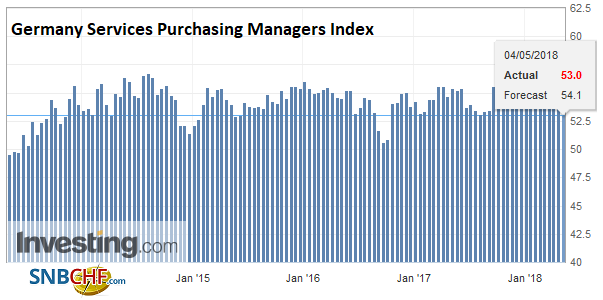

GermanyGermany’s flash PMI reading suggested the economic lull subsided, but the revisions show more work is needed. The service PMI was revised to 53.0 from 54.1 and 53.9 in March. |

Germany Services Purchasing Managers Index (PMI), May 2013 - 2018(see more posts on Germany Services PMI, ) Source: Investing.com - Click to enlarge |

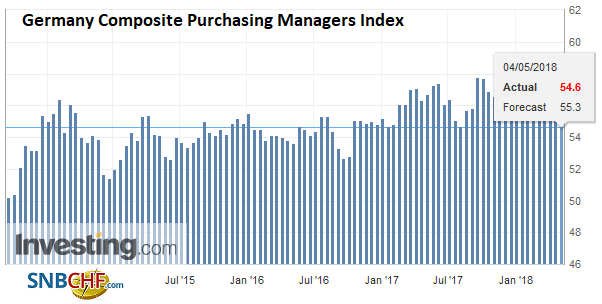

| This seems to be an unusually large revision. The composite was revised to 54.6 from 55.3 flash reading. It was 55.1 in March. France’s flash figures were unrevised, while both Italy and Spain service and composite reports were softer than March. |

Germany Composite Purchasing Managers Index (PMI), Jun 2013 - May 2018(see more posts on Germany Composite PMI, ) Source: Investing.com - Click to enlarge |

More broadly, the US dollar is firmer against all the major currencies, but the yen today. Japanese markets were closed. Three times this week, the market tried in vain to push the greenback above JPY110. It broke down a big figure yesterday, and it continued to find light demand around JPY109. The euro is consolidating its third consecutive weekly decline and has been confined to yesterday’s range. The break of the $1.1930-$1.2030 range will set the near-term tone. Sterling returned to yesterday’s low near $1.3540 where it seems to have found a bid in mid-morning in London, though a break could signal another cent decline

Asian equities remain heavy, and this is picking up the fact that emerging markets have fallen out of favor. The MSCI Asia Pacific Index, excluding Japan, was off for a fourth session, and its third consecutive weekly fall. It has now weakened in six of the last seven weeks, which is the same as the MSCI Emerging Markets Index. In stark contrast, the Dow Jones Stoxx 600 has been alternating between advancing and declining this week, but it is up about 0.2% to extend its streak to a sixth consecutive weekly advance, the longest run in three years.

The bond markets are quiet. The US 10-year yield is hovering around 2.95%, while European bond yields are mostly slightly firmer, though Gilts are following the US lead and yields are a little softer. For the week as a whole, benchmark yields were 2-4 bp lower.

Lastly, we note that the US-China trade talks have ended. Treasury Secretary Mnuchin had indicated that the talks were going “very good,” but in the end, no significant agreement was reached. Previously the Trump Administration signaled it wanted China to reduce its bilateral trade surplus with the US by $100 bln, which by the US reckoning was more than a 25% reduction. By China’s accounting, it was more than a third. Now press reports indicate during its visit, the US Administration sought a $200 bln reduction by 2020.

It is not clear what the next step will be, though we suspect the need to prepare for more trade conflict with China, will encourage the US to reach a deal on NAFTA soon. Talks will resume next week. Here the US demand linking pay (large parts of a car are to be made with labor costing at least $16 an hour) and domestic content will need a long time to be implemented or it may decimate auto production in Mexico. Mexican figures show auto production workers earning about $6 an hour and parts markers, half as much.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$AUD,$CNY,$EUR,$JPY,$TLT,EUR/CHF,Eurozone Markit Composite PMI,Eurozone Services PMI,gbp-chf,Germany Composite PMI,Germany Services PMI,jobs,newslettersent,SPY,USD/CHF