Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

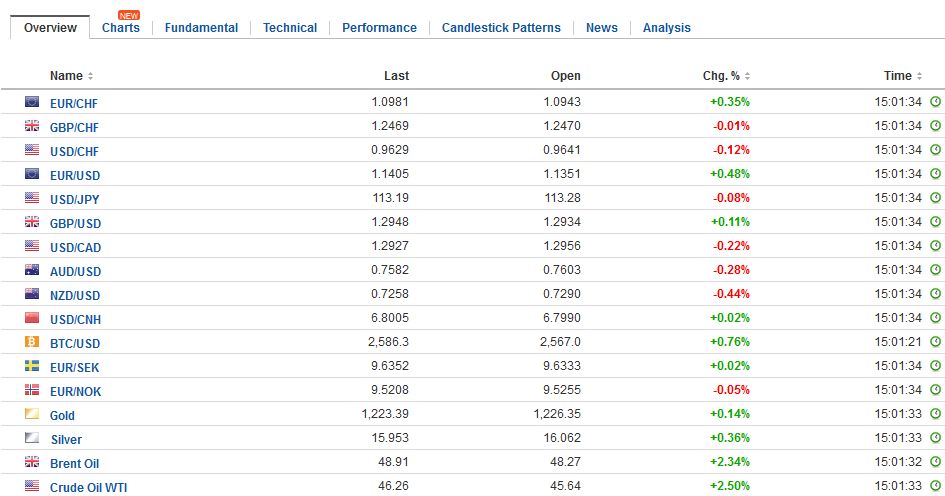

Swiss FrancThe Euro has risen by 0.35% to 1.0981 CHF. |

EUR/CHF - Euro Swiss Franc, July 06 - Click to enlarge |

GBP/CHFhe Pound has found some support over the past week, gaining almost two cents on the CHF at its high. GBP/CHF exchange rates are continuing to float around 1.25, following positive comments made last week by Bank of England (BoE) governor Mark Carney. Carney alluded to a prospective interest rate hike over the coming months, although with no timeline given on the prospective height, are we witnessing something of a false dawn for Sterling? The Franc has found support under 1.25, despite worse than expected inflation data released this morning and the markets focus will now switch to tomorrow, with a host of key economic data released for the UK. At 09.30 the latest Manufacturing & Industrial Production figures are released, alongside Trade Balance data. With an improvement on last month being anticipated by investors, it will be interesting to see whether any positive news has been factored into Sterling’s current value. Trade Balance figures, which indicates how much we spend on imports compared to the money we make on exports, is a key barometer for any economy. This will be monitored even closer the coming months as the UK separates itself from the EU and will be used to gauge how trade deals are faring. However, it will be the latest NIESR Gross Domestic Product (GDP) estimate alongside Carney’s speech, which could shape GBP/CHF rates for the subsequent days. Any further bullish comments regarding future rate hikes, or a positive reading from NIESR could help Sterling break the 1.25 levels against the CHF. Similarly, any negative reading or diluted comments by Carney could push the pound back down and the recent gains could be eliminated extremely quickly. The current market remains extremely volatile and unpredictable, which is why I have been advocating that my clients take advantage of any short-term gains and protect their positions where possible. |

GBP/CHF - British Pound Swiss Franc, July 06(see more posts on GBP/CHF, ) - Click to enlarge |

FX RatesThe US dollar is narrowly mixed against the major currencies after being confined to tight ranges through the Asian session and European morning. Equities are nursing small losses, and interest rates are pushing higher. The yield on the 10-year German Bund reached 50 bp for the first time since early 2016. Oil prices have steadied after yesterday’s slide. The FOMC minutes from last month’s meeting failed to shed fresh light onto the timing of the beginning of gradually reducing its balance sheet. However, it seems as if an agreement on it could be achieved before the next move on the Fed funds target. That said, the minutes were explicit: “most” thought that the recent softening of prices was due to “idiosyncratic” developments. In terms of Fed policy, the market’s attention now turns to Yellen’s semi-annual testimony to Congress next week, followed by the July 25-26 FOMC meeting. The Fed has yet to adopt the tactics under the otherwise plain-spoken Chair that would maximize the degrees of freedom in terms of meetings. Specifically, the Fed seems only comfortable to announce policy changes at meetings followed by press conferences. It could hold press conferences after every meeting, which is what the Bank of Japan and the European Central Bank do, for example. With around 200 countervailing tariffs or anti-dumping duties already “protecting” the US steel industry, domestic prices above world prices, and defense needs absorbing a small part of US capacity; additional unilateral action will likely be contested. In some ways, the US appears to be trying to decide if this is a good test case for its trade initiative. |

FX Daily Rates, July 06 - Click to enlarge |

| Although the minutes do not clarify the situation, we expect the Fed to be content monitoring the economy until the September FOMC meeting. It will have a better sense of the trajectory of prices, including wages. It can have a better sense of the true signal being generated by the broader financial conditions.

The EU and Japan reportedly have reached a political agreement on a free-trade pact ahead of the G20 meeting. It is important not just as a trade agreement between the two that account for a quarter of the world’s GDP. It is important because even though negotiations began several years ago (2013) that the potential defection of the US from the liberal trade regime that it was instrumental in creating, will not necessarily mean the end of that regime. The trade agreement will eventually eliminate 99% of the tariff barriers to trade, according to reports. At the heart of the agreement is a phasing out of the EU’s 10% duty on auto imports while Japan opens up its agricultural market. Japan’s Prime Minister Abe had seen in the TPP an opportunity to the agriculture coops which remain resistant to his reform agenda, and this agreement with the EU achieves perhaps on a smaller scale the same effect. The theme of the G20 summit in Hamburg is a free and fair trade. North Korea’s test of an intercontinental ballistic missile threatens to overtake the agenda. The US strategic goal of denying North Korea nuclear capability and a delivery mechanism appears to have largely failed. None of the key stakeholders have much an appetite for military action to remove that capability. Effectively tightening and enforcing sanctions requires cooperation for which the US does not appear inclined to offer fresh inducements. |

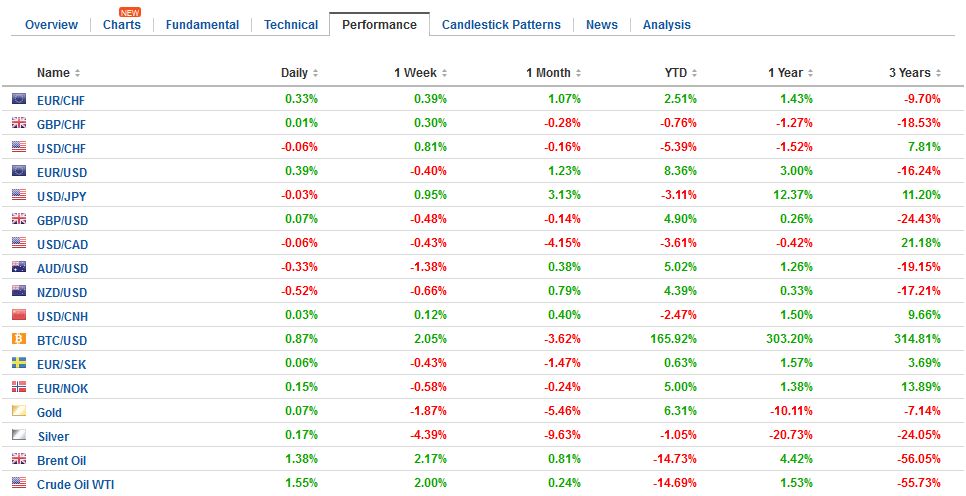

FX Performance, July 06 - Click to enlarge |

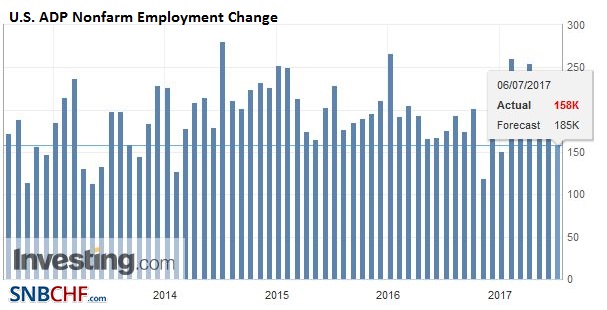

United StatesPrivate sector data in the US in the form of the ADP private sector jobs estimate and the ISM/PMI service sector readings dominate the US economic reports today. The ADP may catch the large trend of the BLS estimate, but on a month-to-month basis, large gaps do arise. |

U.S. ADP Nonfarm Employment Change, June 2017(see more posts on U.S. ADP Nonfarm Employment Change, ) Source: Investing.com - Click to enlarge |

| The employment and price components of the ISM/PMI will likely garner the most attention. |

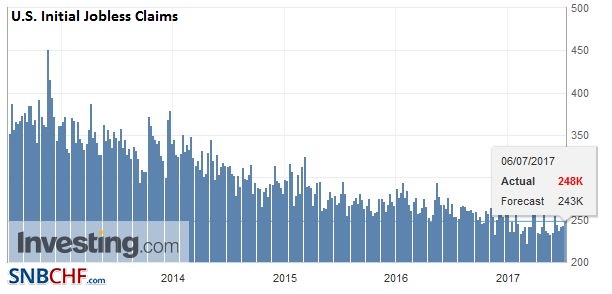

U.S. Initial Jobless Claims, June 2017(see more posts on U.S. Initial Jobless Claims, ) Source: Investing.com - Click to enlarge |

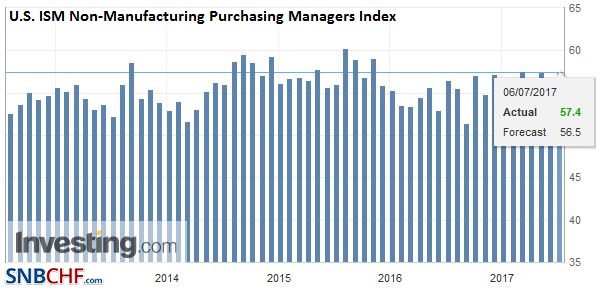

U.S. ISM Non-Manufacturing Purchasing Managers Index (PMI), June 2017(see more posts on U.S. ISM Non-Manufacturing PMI, ) Source: Investing.com - Click to enlarge |

|

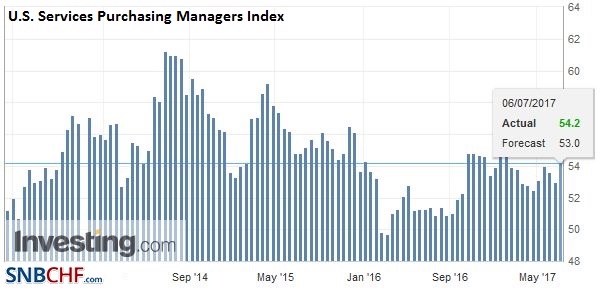

U.S. Services Purchasing Managers Index (PMI), June 2017(see more posts on U.S. Services PMI, ) Source: Investing.com - Click to enlarge |

|

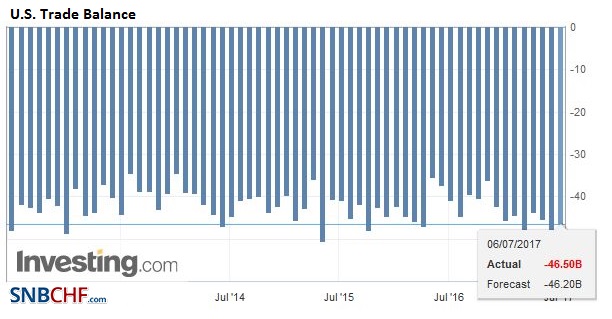

| Separately, the market will also get official data (the May trade balance and the DoE energy report). |

U.S. Trade Balance, May 2017(see more posts on U.S. Trade Balance, ) Source: Investing.com - Click to enlarge |

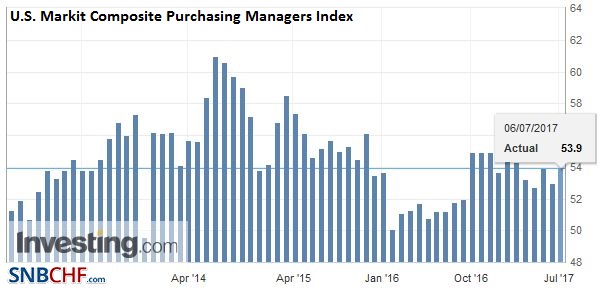

U.S. Markit Composite Purchasing Managers Index (PMI), June 2017(see more posts on U.S. Markit Composite PMI, ) Source: Investing.com - Click to enlarge |

|

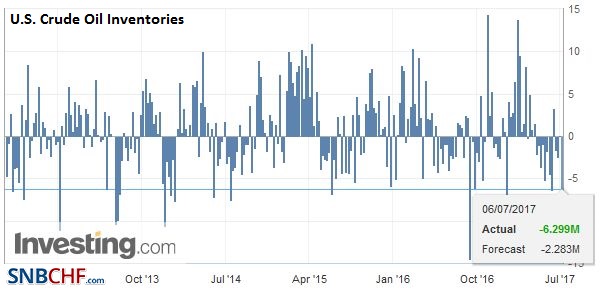

| News that API estimates that US oil stocks fell a sizable 5.8 mln barrels is helping prices stabilize today ahead of the DOE’s estimate later in the US morning. Support is seen near $44 a barrel and a break would re-target the low from late June near $42. |

U.S. Crude Oil Inventories, June 2017(see more posts on U.S. Crude Oil Inventories, ) Source: Investing.com - Click to enlarge |

US 10-year inflation expectations crept higher (breakeven) despite the 4.1% drop in August light sweet crude oil prices, which ended an eight-day, nearly 13% rally with an exclamation point. The ostensible trigger was a report suggesting Russia had no appetite to increase its efforts with OPEC to bolster the prices, while Libyan and Nigerian output, which is excluded from the output cuts, have boosted OPEC’s output.

We expect the economy to evolve to allow the Fed, which has put the market on notice that it will “relatively soon” begin not reinvesting all the maturing Treasuries and MBS, to carry through with this commitment at the September FOMC meeting. This will allow the balance sheet to shrink by what seems like an inconsequential $30 bln before the end of the year.

Separately, and looming over the G20 meeting is the US threat of imposing tariffs (and possibly quotas) on steel import on the grounds that they pose a national security risk. The investigation has reportedly been completed, and the debate has shifted to the precise policy response. There appears to be a small window of opportunity to persuade US President Trump to use the WTO’s conflict resolution mechanisms. It may take a bit longer, but the US does win the lion’s share of cases it brings.

There can be two outcomes. The WTO finds against the US, and the US chooses to ignore the ruling, which it has threatened to do. This could potentially spur a crisis of the multilateral institution. Alternatively, the WTO could grant a liberal interpretation to its national security exemptions, which would likely spur copycat behavior elsewhere, creating a new loophole for protectionism.

Canada

Canada reports building permits and trade ahead of tomorrow’s employment report. Which will be the last important data ahead of next week BoC meeting where a 25 bp rate hike is now widely anticipated.

Germany

Germany reported a smaller than expected recovery in factory orders. After a 2.2% slide in April, economists had expected nearly a full recovery in May. The actual increase of 1.0% was about half of the gain forecasts. Orders for basic and consumer goods fell, while foreign orders for investment goods rose 6.0%.

Despite the disappointment with today’s report, the strong manufacturing PMI for June blunts any negativity. Germany reports May industrial output figures tomorrow. The median guesstimate of a 0.2% rise, following a 0.8% increase in April, will suffice to lift the year-over-year, workday adjustment rate to 4%, the highest in three years.

Eurozone

The market awaits the record from the ECB meeting. It is keen for insight into the timing of the next policy step. We expect that at the September meeting, the ECB will announce it is extending its asset purchases into next year but at a slower pace than the current 60 bln euros a month. To make these purchases, the ECB appears to be deviating from the capital key, which is supposed to be one of the controlling rules shaping the sovereign bonds/agencies being purchased. Although some deviations have been sustained for several months (Finland and the Netherlands, for example), we are reluctant to read too much into it, and instead, view at as a minor technicality. The ECB can change and modify its rules as it sees fit, and although it is not likely, it can boost its purchases if needed.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,$EUR,$JPY,$TLT,EUR/CHF,Federal Reserve,FX Daily,gbp-chf,newslettersent,OIL,U.S. ADP Nonfarm Employment Change,U.S. Crude Oil Inventories,U.S. Initial Jobless Claims,U.S. ISM Non-Manufacturing PMI,U.S. Markit Composite PMI,U.S. Services PMI,U.S. Trade Balance