Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

Swiss Franc |

EUR/CHF - Euro Swiss Franc, February 14(see more posts on EUR/CHF, ) - Click to enlarge |

|

The pound has seen a good start to the week making gains against all of the major currencies including the Swiss Franc. One of the reasons why the pound is supported appears to be the shift of attention from Brexit to other global changes to include the new Trump administration and the upcoming European elections. Greece is also another situation which has resurfaced again as another debt repayment nears. GBP CHF still remains weak historically with rates sitting at 1.26 for this pair. There is still an excellent opportunity for anyone selling Swiss Francs and with so many political developments things could change at a moments notice. Once there is more clarity over Brexit and also the European element then the Swiss Franc may not be so important in its role as a safe haven currency. If there are no major political upsets in France and the Netherlands then the Swiss Franc may lose some of its shine and the Swiss Franc may start to weaken. If however Marine Le Pen on the National Front wins the French election this would be particularly damaging for the Eurozone and funds would likely flood into the Swiss Franc. For those clients looking to push for even higher rates then this could present an excellent opportunity. The Dutch elections may be the precursor to this and should Geert Wilders party win in the Netherlands then again the Swiss Franc could start to strengthen again. |

GBP/CHF - British Pound Swiss Franc, February 14(see more posts on GBP/CHF, ) - Click to enlarge |

FX RatesCorrective pressures are gripping the major capital markets today.The Dollar Index’s nine-day advancing streak is being threatened by the position adjustment ahead of Yellen’s testimony later today. Despite record high closes in the main US equity markets yesterday, Asia could not follow suit. It tried to initially, and recorded new highs since July 2015, but sellers emerged and the MSCI Asia Pacific Index closed marginally lower on the lows of the day. European bourses are mixed in morning turnover, but the Dow Jones Stoxx 600 may snap a five-day advance. The US S&P 500’s five-day streak is also on the line. |

FX Daily Rates, February 14 - Click to enlarge |

| Sterling shed a cent on the news. It is the only major currency not to be stronger against the dollar today. In part, what seems to be an exaggerated response to the inflation figures may be a reflection of its recent strong gains on the crosses. The euro was fraying with a neckline of a topping pattern near GBP0.8470. Sterling rallied from near JPY138.55 to JPY142.60 over the past week.

Separately, reports suggest the Trump Administration, where Treasury Secretary Mnuchin was confirmed yesterday, is contemplating a change in the approach to currency manipulation. It may move away from the traditional language and regarded undervalued currencies as a subsidy, which would allow US business a quicker way to register a complaint and seek redress. The challenge with such an approach is that by many metrics, including the IMF, the yuan is not so much undervalued. The reason that this approach has been rejected by previous administrations is that it could open the US up to retaliation during a period of easing monetary policy and a falling dollar. Some countries, like Brazil, had argued that the US unorthodox monetary policy under Bernanke was equivalent to a shot in a currency war. |

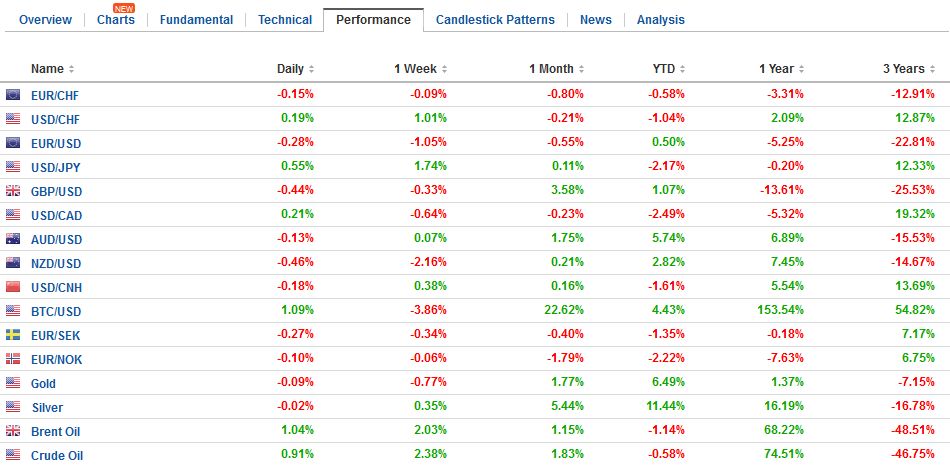

FX Performance, February 14 - Click to enlarge |

United StatesThe US Treasury market is flat, while European benchmark 10-year yields are mostly lower. Premiums over Germany continue to ease after the recent blowout. The French 10-year premium over Germany is slipping. Recall, the spread peaked at the start of last week near 76 bp. It is now at 68 bp. This is still elevated, but without the earlier momentum. At the same time, the US 2-year premium over Germany, which often tracks the euro-dollar exchange rate, is edging above 200 bp for the first time this year. It peaked at the end of last year near 206 bp, which was the widest since 2000. |

US Treasuries 10 Year Yield, Feb 2016 - 2017(see more posts on U.S. Treasuries, ) Source: Bloomberg.com - Click to enlarge |

| The highlight of the North American session is Yellen’s first leg of her Congressional testimony. We do not expect her prepared remarks to go much beyond the recent FOMC statement. The economy continues to evolve as the Fed expects, and full employment is being approached, while officials are more confident that its inflation target will be reached. We do not expect her to reveal anything about next month’s meeting, which may disappoint those who expect a hike. Bloomberg estimates that there is 30% chance of a March hike already discounted. Our work suggests the Fed funds strip implies less chance, but the point is that there could be some disappointment, which in the current context could be slightly dollar negative. |

U.S. Producer Price Index (PPI) YoY, January 2017(see more posts on U.S. Producer Price Index, ) Source: Investing.com - Click to enlarge |

| Yellen may be pressed on two other issues: The central bank’s response to the Administration’s fiscal policy and the Fed’s balance sheet. There is still not much clarity about fiscal policy. However, on February 28, Trump will address both houses of Congress (as Obama did in February 2009). It is expected that Trump will lay out some the main planks of his fiscal plans then. However, this still may not be sufficient to impact the Fed’s decision in March, though it could spur a change in the economic projections (dot plot).

Several regional Fed Presidents have expressed a desire to begin talking about the Fed’s balance sheet strategy. Yellen is likely to respond to questions by saying the Fed is looking at the issue, but stick to generalities, like the first step is to stop reinvesting maturing issues. Just as Bernanke set the table for the tapering under Yellen, so too may Yellen devise a strategy for gradual reduction of the Fed’s balance sheet for her successor. That said, given that Trump will appoint at least three governors this year, their participation in the discussions are critical. |

U.S. Core Producer Price Index (PPI) YoY, January 2017(see more posts on U.S. Core Producer Price Index, ) Source: Investing.com - Click to enlarge |

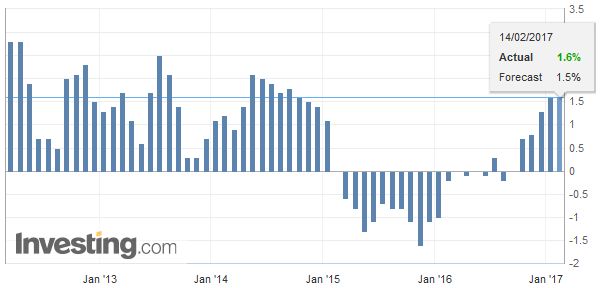

United KingdomThere has been a flurry of economic news. The report that appears to have had the largest impact was UK inflation. Headline CPI fell 0.5% as the median anticipated, but this did not lift the year-over-year pace as much as expected. The 1.8% year-over-year increase just missed the median by 0.1%, though it is still 0.2% higher than December. The core rate had been expected to tick higher, but it remained unchanged at 1.6%. Recall the UK’s core CPI rose 1.4% 2015.The headline rate was 0.2% in 2015 and 1.6% last year. The different performance of the two suggests that most the inflation the UK is experiencing is the result of higher energy (and food prices). While this force may ease later in the year, the impact of the past decline in sterling is expected to filter through. |

U.K. Consumer Price Index (CPI) YoY, January 2017(see more posts on U.K. Consumer Price Index, ) Source: Investing.com - Click to enlarge |

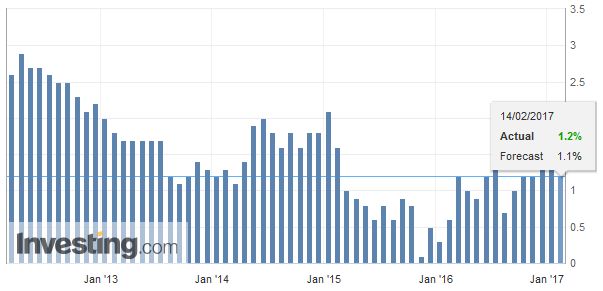

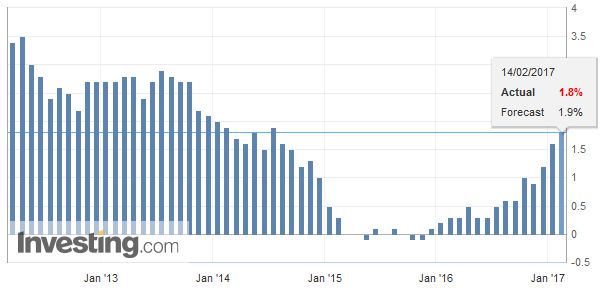

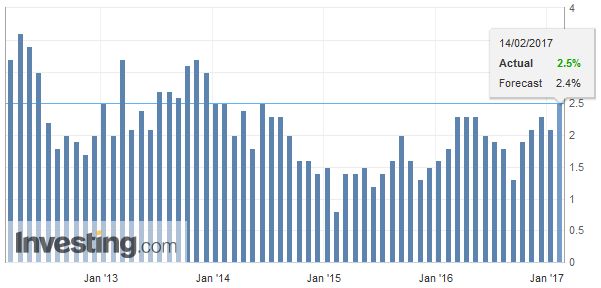

ChinaChina also reported January inflation figures. Both CPI and PPI were stronger than expected. The 2.5% rise in CPI follows a 2.1% pace in December. It matches the highs since November 2013. The median guesstimate was for a 2.4% gain. We had suggested upsides risks due to the Lunar New Year. |

China Consumer Price Index (CPI) YoY, January 2017(see more posts on China Consumer Price Index, ) Source: Investing.com - Click to enlarge |

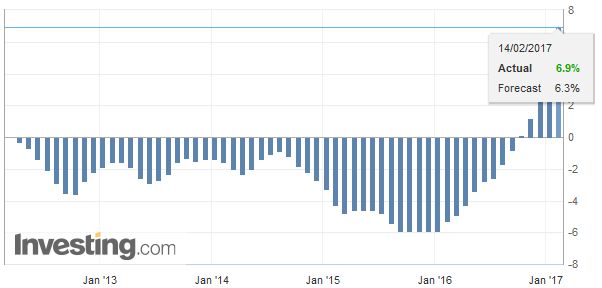

| Producer prices jumped 6.9% from 5.5% in December. This is the strongest past since 2011. The median guesstimate was 6.3%. This probably has less to do with the Lunar New Year and more to do with the strong rally in commodities. Raw materials rose 12.9% and mining 3.1%. |

China Producer Price Index (PPI) YoY, January 2017(see more posts on China Producer Price Index, ) Source: Investing.com - Click to enlarge |

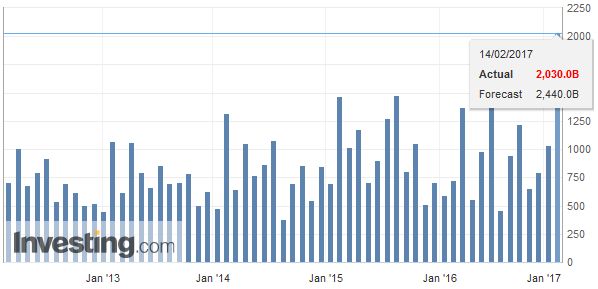

| With signs the economy has stabilized, officials may turn their attention to the rising inflation and accelerating credit growth. New yuan loans were less than expected at CNY2.03 trillion (Bloomberg median was for CNY2.44 trillion), though it is still nearly double December’s CNY1.04 trillion. This means that the surge in the aggregate financing of CNY3.74 trillion (median was CNY3.0 trillion after December’s CNY1.63 trillion) reflects a resurgence of shadow banking. Among shadow banking instruments, banker acceptances jumped four-fold. |

China New Loans, January 2017(see more posts on China New Loans, ) Source: Investing.com - Click to enlarge |

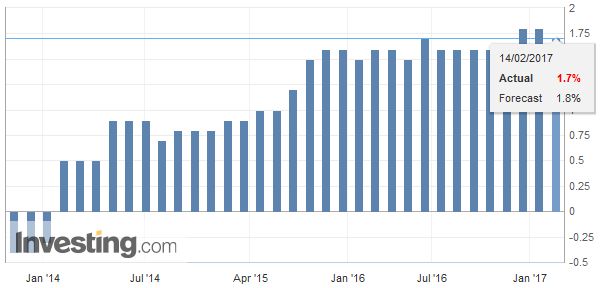

EurozoneIn the eurozone, German, Italian, and Dutch GDP estimates missed expectations by 0.1%. |

Eurozone Gross Domestic Product (GDP) YoY, January 2017(see more posts on Eurozone Gross Domestic Product, ) Source: Investing.com - Click to enlarge |

| This resulted in the eurozone Q4 16 GDP revised to 0.4% rather than 0.5% and puts the year-over-year pace at 1.7% rather than 1.8%. |

Eurozone Industrial Production YoY, January 2017(see more posts on Eurozone Industrial Production, ) Source: Investing.com - Click to enlarge |

ItalyDespite the minor disappointment, growth was fairly stable in 2016, and although it did not reach 2% as it recorded year-over-year in 2015, it is still regarded as above trend. This means that the output gap continued to close, even though unemployment remains stubbornly high. |

Italy Gross Domestic Product (GDP) YoY, January 2017 Source: Investing.com - Click to enlarge |

GermanyPerhaps the German news was most disturbing. Not only was a Q4 growth less than initially estimated (0.4% form 0.5%), but Q3 growth was shaved from 0.2% to 0.1%. Adding insult to injury, the ZEW survey showed a deterioration of both the current assessment (76.4 from 77.3) and expectations (10.4 from 16.6). Often we find that the investor sentiment in the ZEW survey is sensitive to how the DAX performs. In the first month and a half of 2017, the DAX is the second strongest G7 equity market, up 2.5% (the S&P 500 is the best with almost a 4% gain this year). |

Germany ZEW Economic Sentiment, January 2017(see more posts on Germany ZEW Economic Sentiment, ) Source: Investing.com - Click to enlarge |

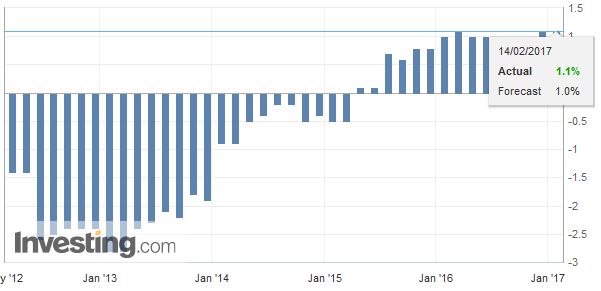

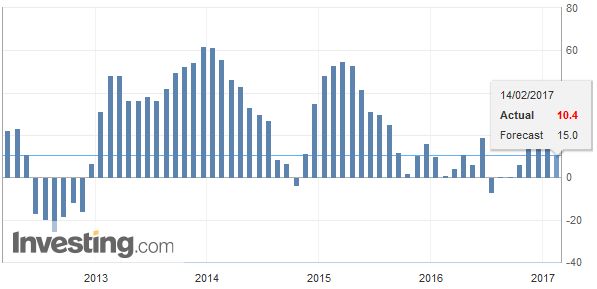

Switzerland |

Switzerland Consumer Price Index (CPI) YoY, January 2017(see more posts on Switzerland Consumer Price Index, ) Source: Investing.com - Click to enlarge |

Switzerland Producer Price Index (PPI) YoY, January 2017(see more posts on Switzerland Producer Price Index, ) Source: Investing.com - Click to enlarge |

Full story here Are you the author?

Tags: #GBP,#USD,$EUR,China,China Consumer Price Index,China New Loans,China Producer Price Index,EUR/CHF,Eurozone Gross Domestic Product,Eurozone Industrial Production,gbp-chf,Germany ZEW Economic Sentiment,Italy Gross Domestic Product,newslettersent,SPY,U.K. Consumer Price Index,U.S. Core Producer Price Index,U.S. Producer Price Index,U.S. Treasuries