Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

Summary:

Don’t expect a deal between Greece and its official creditors until late spring or early summer.

Grexit is still not a particularly likely scenario.

It was the European governments not Greece which put other taxpayers’ skin in the game.

Freud warned that unresolved psychological conflicts might be repressed but they keep returning. So too with Greece debt problems. A new crisis is at hand. Investor nervousness is evident in the surge in the two-year yield this week is up nearly 100 bp. The fact that the 10-year yield is up a more modest 10 bp and minor losses in Greek stocks this week suggest the investors may be more sanguine.

In 2010 and again in 2015 many thought Greece was going to be forced out of the monetary union, and both times the many observers and investors underestimated the political will to preserve the union. Some have begun talking about Grexit again, but this is very premature. The pressure now will likely ease, even without a near-term solution as Greece’s roughly seven bln euro payment is not due until July. Given the cast of characters and the political calendar, there is no reason to expect that this time will be different and it to go to the very brink.

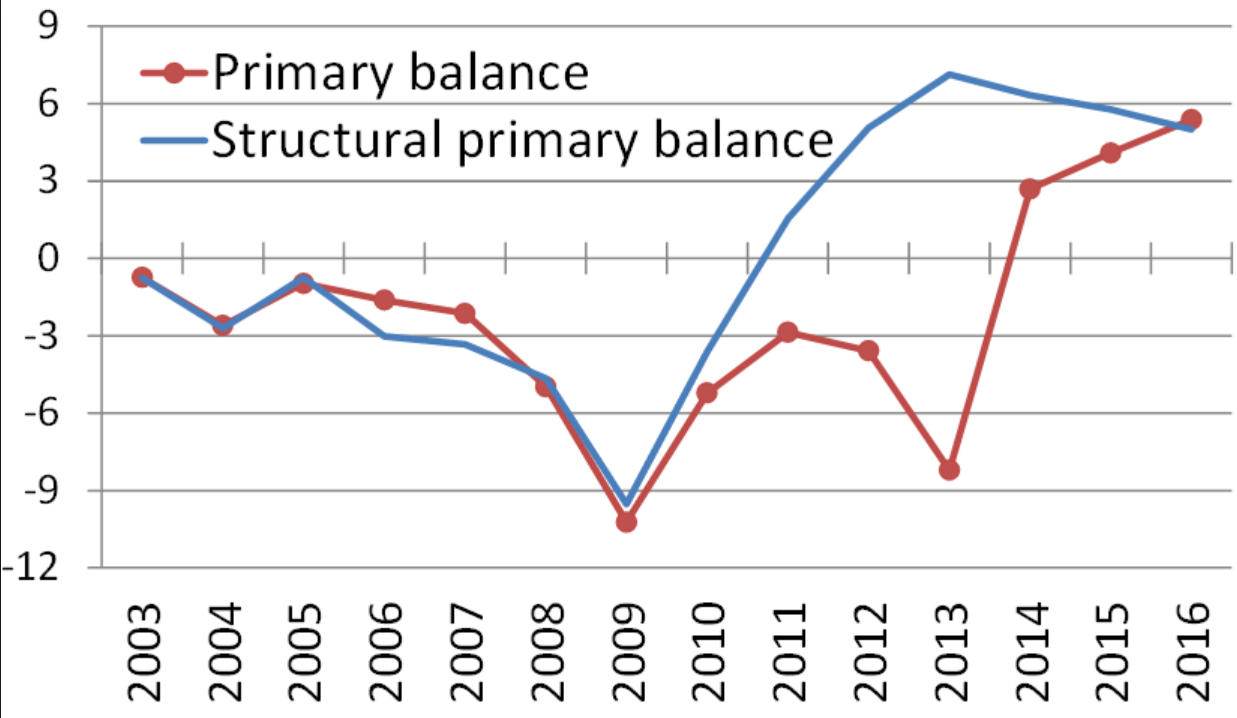

There are no reasons to expect an early resolution. The key issue is not about this year’s budget. It is about the commitment to a 3.5% primary budget surplus starting next year that was agreed upon in the 2015 deal. That agreement called for Greece to run a primary surplus of 3.5% for the medium term beginning in 2018. Germany argues that medium-term means a decade, while the European Commission says it mean 1-2 years.

| There are no reasons to expect an early resolution. The key issue is not about this year’s budget. It is about the commitment to a 3.5% primary budget surplus starting next year that was agreed upon in the 2015 deal. That agreement called for Greece to run a primary surplus of 3.5% for the medium term beginning in 2018. Germany argues that medium-term means a decade, while the European Commission says it mean 1-2 years. |

Greece Primary Surplus 2003 - 2016 - Click to enlarge |

| Last year Greece recorded a 2% primary budget surplus. The initial target was a deficit of 0.5%. The results gave the government the wherewithal to offer some tax relief for some of the islands and some pension relief to the dismay of the official creditors. The problem is that last year’s achievement is not a recurring process. The IMF says that the primary surplus was the result of one-off factors and that the Greece needs to take additional belt-tightening measures to the tune of about 2% of GDP.

The Greek government is reluctant to impose more any more austerity. The kind of fiscal adjustment that has been foisted on Greece, in part because the official sector refuses to accept debt relief, typically is counterproductive. Because of the impact on the denominator, debt-to-GDP ratios worsen. This was also the case in the large fiscal adjustments pre-2008 in Denmark, Sweden, and Finland, for example, and they had the benefit of currency depreciation and a domestically-run monetary policy. |

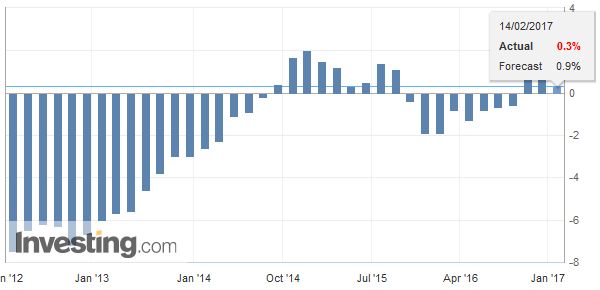

Greece Gross Domestic Product (GDP) YoY, Q4 2016 Source: Investing.com - Click to enlarge |

| The Greek economy is showing some green shoots. More austerity could easily kill the traumatized patient. The economy expanded by 0.4% in Q2 and 0.8% in Q3. The initial estimate for Q4 will be reported next week (February 14). A 0.4% expansion in Q4, would be the longest expansion streak in a decade. It would put 2016 year-over-year growth around 0.4% after a 0.2% contraction in 2015. |

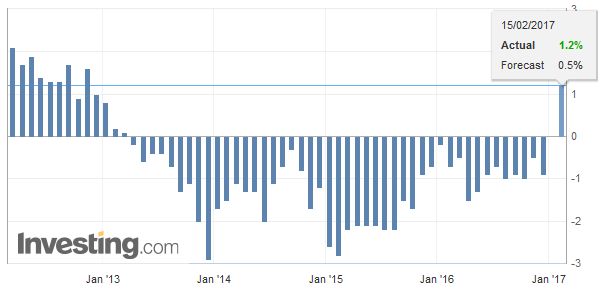

Greece Consumer Price Index (CPI) YoY, January 2017 Source: Investing.com - Click to enlarge |

There is a European finance ministers’ meeting on Feb 20. It was hoped an agreement would be reached by that meeting. Such an agreement would be new Greek austerity measures for payment from the 86 bln euro 2015 package to ensure that government can make the seven bln euro payment due in July. If the agreement is elusive, which seems highly probable, then the situation looks frozen for at least three months. The Dutch parliamentary approval is necessary, and it will be dissolved ahead of the March election. The French election in April (and a likely second round in May) will also likely deter an agreement.

The underlying issue is the sustainability of Greece’s debt. In an unusual development, the IMF executive board was split on the issue earlier this week. The European contingent argued that Greece’s debt is sustainable and that the European commitment to Greece is what makes it a unique case. Other board members, including the US, China, Brazil, India and South Africa questioned the sustainability of Greece’s debt and did not accept that a 3.5% primary budget surplus for years was realistic.

The IMF’s position is important even though when the crisis first broke the ECB and Germany were not particularly keen for the involvement of the multilateral lender. Now Germany (and the Netherlands) insist on the IMF’s participation as a condition for their continued support. At the same time, the IMF’s assessment has increasing diverged from Germany’s and the European Commission’s (self-serving) assessment more broadly.

The European creditors are expected to make a specific proposal for a contingency policies that will automatically kick in if the primary budget target is missed. Most likely, Greece’s Prime Minister Tsipras will reject the proposal. As we have seen, the more austerity, the weaker the economy. The economy shrinks faster that spending can be cut, which results in an increase in the debt-to-GDP ratios, which forces more austerity, and so on and so forth.

If pushed hard, Tsipras could call early elections. Syriza may not win the election, but imposing a new round of austerity would erode its support in any event. A new government, perhaps led by New Democracy might see the European creditors offer a slightly better deal. However, recall that Syriza came to power primarily because of the loss of credibility of the mainstream parties. Although Tsiprias equivocates and offers strong rhetoric, he has largely implemented demands of the creditors. Almost 99 years ago, Keynes warned, and history has shown, that there are indeed limits on a country’s willingness to service foreign creditors with current output. That means that nearly any elected government in Greece is going to resist the never-ending demands of the creditors.

It is the European countries, not Greece, that put other tax payers money on the line. How did the official sector become Greece’s largest creditor? Greek bonds were in the private sector hands, but the ECB (under Trichet, not Draghi) bought them from the banks. European governments wanted to avoid a Greed default, so they loaned the Greek government money so Greece can repay its lenders.

The IMF, seemingly belatedly, is pushing for debt relief. The previous US government argued for debt relief. Given Trump’s experience with renegotiating debt and bankruptcy, the US position may not change. However, given the elections in the Netherlands, France, and Germany this year, debt forgiveness of any kind will most likely not be agreed upon this year.

Investors should be prepared for new brinkmanship. A deal is not likely this month or much before the July. Talk of Grexit will increase again. However, the larger political context, including Brexit, Trump and a more aggressive Russia, the political will to keep Greece in the EU and EMU has likely strengthened rather than slackened. Still, until Greece’s debt is on a clearly sustainable path, it will be a recurring issue. Other countries with large debt-to-GDP burdens, like Japan and Italy, have greater capacity to service it than Greece.

Full story here Are you the author?

Tags: $EUR,Greece,IMF,newslettersent