Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

Swiss Franc |

EUR/CHF - Euro Swiss Franc, November 14(see more posts on EUR/CHF, ) . - Click to enlarge |

FX RatesThe US dollar rally that moved into a higher gear in the second half of last week has begun the new week with a bang. It is up against nearly all the major and emerging market currencies. Even sterling, which last week, managed to eke out modest gains against the greenback is under pressure today. Of note, the US Dollar Index has made new highs for the year today edging briefly through 100.00. The last December high was set near 100.50. It had hit a low near 96.00 in the knee-jerk move when the election results had been clear. Today’s advance has lifted the intraday technicals stretched, and some consolidation is likely. Support is seen in the 99.15-99.50 band. |

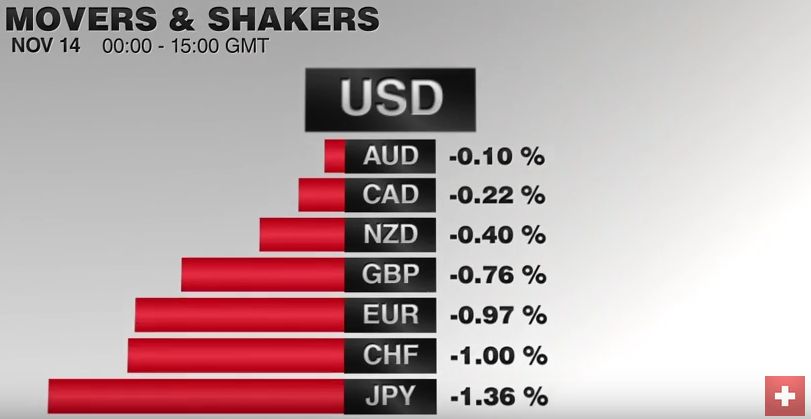

FX Performance, November 14 2016 Movers and Shakers . Source: Dukascopy - Click to enlarge |

| The euro dripped below $1.0730 in late-Asian turnover but is stabilizing in the European morning. Sterling slid to $1.2464, off more than 1.25 cents. The bounce in the European morning seemed to fizzle out ahead of $1.2550. The greenback traded at JPY108 for the first time since early June. The dollar was recording session highs against the yen in Europe. The Turkish lira and South African rand are the hardest high among emerging market currencies. The Mexican peso is off another 0.7% today.

The euro-sensitive US-Germany two-year interest rate differential is at 157 bp today, which is a new ten-year extreme. It began the month near 145 bp. The US 10-year premium has risen to 284 bp, the most since 2010. The spread has widened by nearly 40 bp so far this month. |

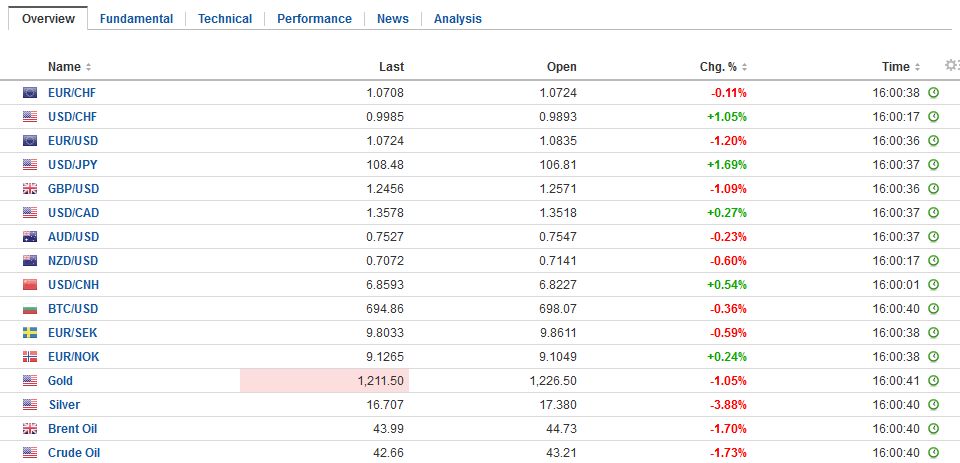

FX Daily Rates, November 14 (GMT 16:00) . - Click to enlarge |

| The driving force continues to be the anticipated shift toward the more fiscal stimulus, while confidence grows of Fed rates hikes, with the second in the cycle expected to be delivered next month. The magnitude of the US stimulus the investors seem to be assuming will pass a Republican-controlled Congress has spurred a shift out of bonds, emerging markets, and gold. These broad developments continue today.

The Chinese yuan is off about 0.5% against the dollar today. The dollar reached almost CNY6.85, the highest since 2008. It is more of a dollar story than a yuan story. Since the even of the US election, the yuan has fared better than most in the region, falling almost 1%. Only the pegged Hong Kong dollar and the Indian rupee has fared better (and Indian markets are closed today for a national holiday). The offshore yuan has not fallen as much as the onshore yuan. |

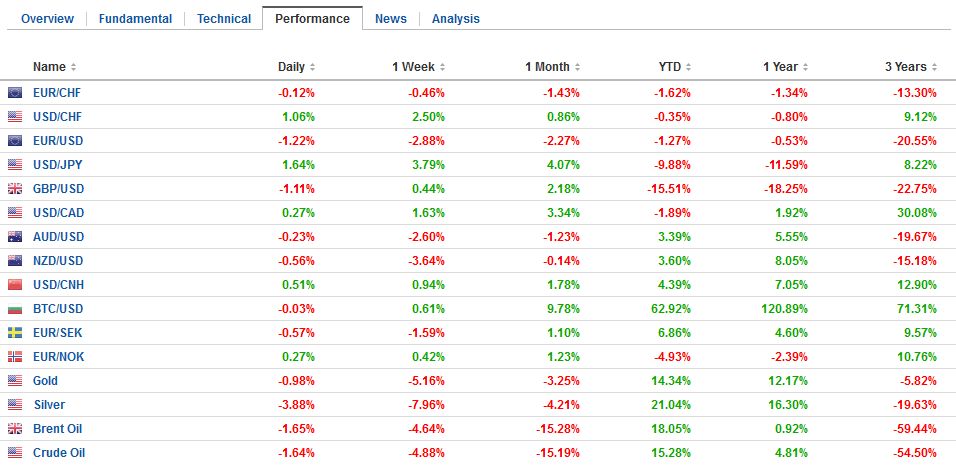

FX Performance, November 14 . - Click to enlarge |

EurozoneBonds continue to sell-off, and as European bonds sell-off the risk premium over Germany is widening, and this will be a source of strain if it persists. The 10-year Bund yield is up six bp, while the French yield is up nearly 10 bp, and the peripheral yields are up 13-14 bp. The US 10-year Treasury yield is up nine basis points to 2.24%, it highest since the start of the year. The 30-year bond yield is poking through 3.0% for the first time since January.

|

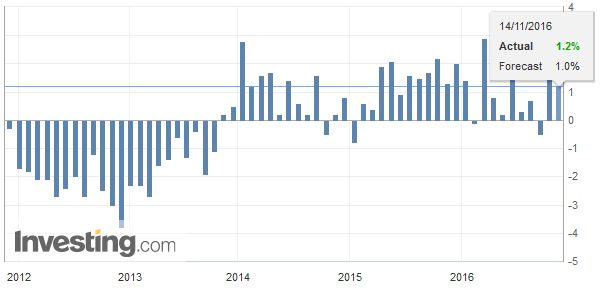

Eurozone Industrial Production YoY, October 2016(see more posts on Eurozone Industrial Production, ) . Source: Investing.com - Click to enlarge |

JapanThe same pattern is evident between the US and Japan. The US 10-year premium is at 275 bp. It is the most in nearly three years. It began the month a little below 190 bp. The two-year premium is near 120 bp, which is the highest since 2008. While Japanese and Chinese shares are advanced, the MSCI Asia-Pacific Index slipped 0.55%, as rest of the region lost ground. MSCI Emerging Market equity index is off 0.8% before South American markets open. It is the fourth day of declines. Since October 20, this benchmark has only risen in four sessions, and two of them were recorded at the start of last week. It stands at a four-month low today. In addition to the anticipated US fiscal stimulus, Japan and China reported constructive news today. Japan’s Q3 GDP rose 0.5% more than twice what the Bloomberg median forecast (0.2%). The details, however, were disappointing and did not seem to presage a stronger pick-up in the Japanese economy. Private consumption rose 0.1%, which is better the flat reading that was expected, but the Q2 figure was revised to 0.1% from 0.2%. Business spending was flat, which was disappointing. Government spending added 0.1 percentage points to GDP but was up 0.4% on the quarter. The main impetus came from next exports which rose 0.5%. The GDP deflator fell to -0.1% from 0.7% in Q2. It is the first negative reading since Q4 13. |

Japan Gross Domestic Product (GDP) YoY, October 2016(see more posts on Japan Gross Domestic Product, ) . Source: Investing.com - Click to enlarge |

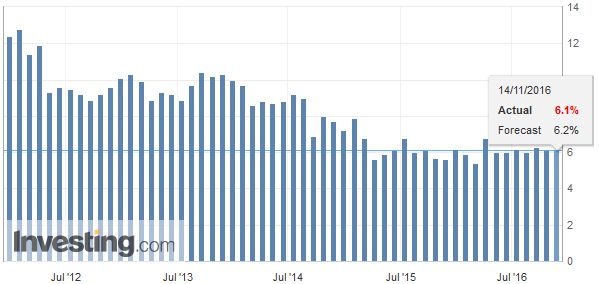

ChinaChina reported fairly stable industrial output, retail sales, and fixed-asset investment. Industrial output rose 6.1% year-over-year in October, matching the September pace. |

China Industrial Production YoY, October 2016(see more posts on China Industrial Production, ) . Source: Investing.com - Click to enlarge |

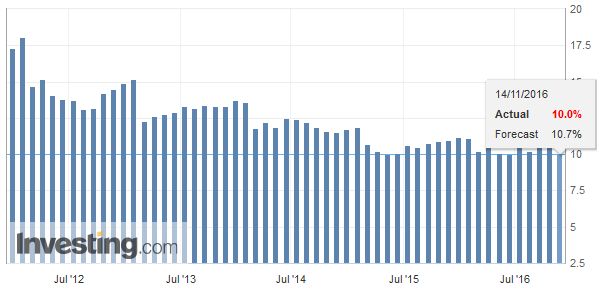

| Year-to-date retail sales rose 10.3% after a 10.4% pace in September. |

China Retail Sales YoY, October 2016(see more posts on China Retail Sales, ) . Source: Investing.com - Click to enlarge |

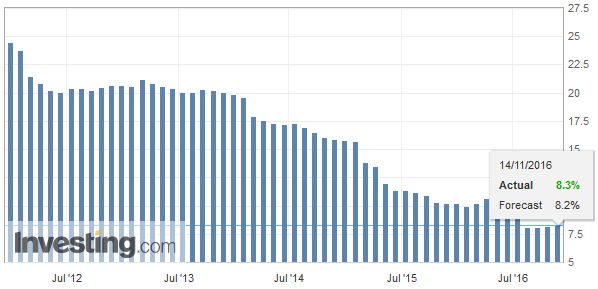

| Investment rose 8.3% after 8.2% year-over-year in September. |

China Fixed Asset Investment YoY, October 2016(see more posts on China Fixed Asset Investment, ) . Source: Investing.com - Click to enlarge |

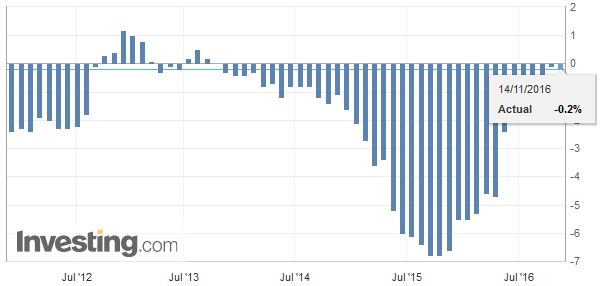

Switzerland |

Switzerland Producer Price Index (PPI) YoY, October 2016(see more posts on Switzerland Producer Price Index, ) . Source: Investing.com - Click to enlarge |

There is a light economic calendar in North America today. Three Fed officials speak, Kaplan, Lacker, and Williams, but the latter two are late in the session. The most important thing now for investors is the signals from President-elect Trump and potential cabinet members.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$EUR,$JPY,China Fixed Asset Investment,China Industrial Production,China Retail Sales,EUR/CHF,Eurozone Industrial Production,FX Daily,Japan Gross Domestic Product,newslettersent,Switzerland Producer Price Index