Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

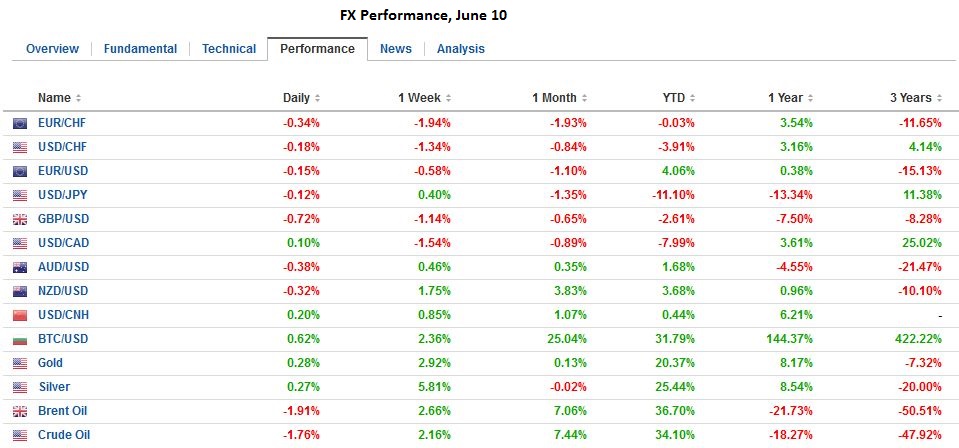

Swiss FrancOnce again, CHF is one of the strongest performers on the FX market. Next Monday we will report how much the Swiss National Bank had to intervene in our regular “Weekly SNB sight deposits” report.

|

See the Dukascopy Video |

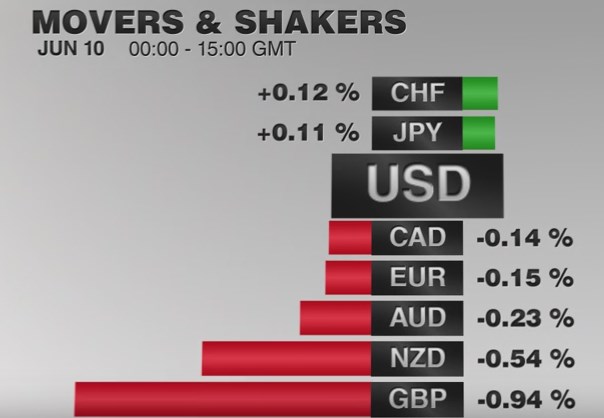

FX RatesThe US dollar weakened in the first half of the week as participants continued to react to the shockingly poor jobs report and shift in Fed expectations. However, it recovered smartly yesterday and is seeing some modest follow through buying today. |

Click to enlarge. |

| The main exceptions today are the Japanese yen and Swiss franc, the only major currencies besting the dollar today. For the week, it is the dollar-bloc and franc that have maintained weekly gains. And those dollar-bloc gains look vulnerable. The New Zealand dollar is the star. It is still up nearly 2% on the week, following the RBNZ’s decision to leave rates alone and issued less dovish statement than expected. Its small losses today appear simply consolidative in nature. |

Click to enlarge. |

The Australian dollar is a different kettle of fish. It staged a key reversal yesterday by making a new high for the move (poked briefly through the $0.7500 target) and then proceeded to sell-off through the previous day’s low. There has been follow through selling today which pressed the Aussie through $0.7400. If the bounce from late-May is being retraced, the initial target is near $0.7365 and then $0.7325.

The Canadian dollar’s performance puts it between the two Antipodean currencies. It is holding on to about a 1.5% gain this week coming into today’s North American session. Three considerations may see these gains pared. First, oil prices are easing and are already about 3% off yesterday’s highs. Second, in an otherwise light North American economic calendar today, Canada reports May jobs data. The median calls for a small gain in jobs after a small loss in April. We suspect the risk is on the downside. Also, the unemployment rate may tick up from 7.1%. Third, technical considerations suggest if the US dollar cannot be pushed back below CAD1.27, the risk is that corrective forces lift the greenback toward CAD1.2850 initially.

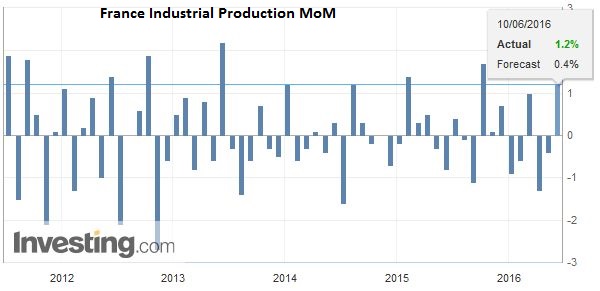

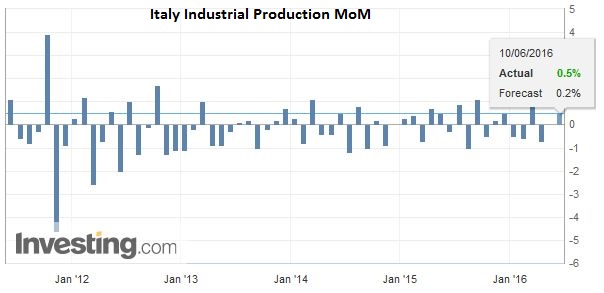

EurozoneIn Europe, the main economic data were French and Italian industrial output figures for April. Both beat expectations. This follows the slightly better than expected German report earlier in the week. Some observers see in the data the basis for an industrial recovery. While hopeful, we do not think that today’s reports are convincing, but another month’s would be and here is why. There has been a distinct pattern in French and Italian industrial production figures for the past several quarters. Every quarter, both countries see industrial output only rise in one month. The gains reported earlier today are consistent with this pattern. For Italy, the pattern goes back to Q1 15. For France, the pattern appears to have begun in Q2 15. |

Major Economic Events – click to enlarge. |

| This is not to deny the strength in the April figures. The 0.5% rise in Italian output is the first increase since January. The median estimate was for a 0.3% increase. The French surprise was larger. The median expected output to rise by 0.4% and instead it jumped 1.2%. Manufacturing production itself rose 1.3% compared with expectations for a 0.8% gain. The French report was particularly surprising given that the manufacturing PMI in April fell to 48.0 from 49.6.

The euro found little succor in the reports. The euro posted a key reversal yesterday, and there has been modest follow through selling today. At $1.1295, the euro retraced 38.2% of the gains since May 30. The intraday technicals warns that the 50% retracement (~$1.1260) can be approached before the weekend. |

Click to enlarge. |

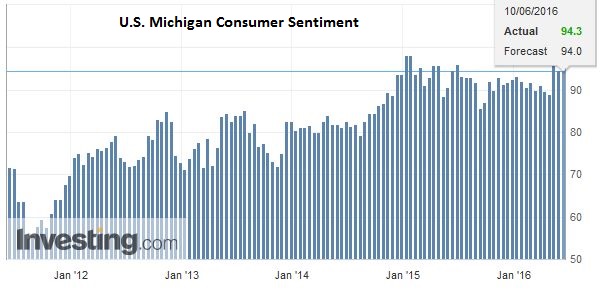

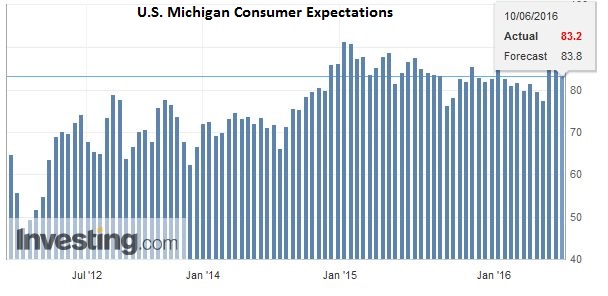

United StatesThe most important event is the Michigan consumer sentiment and expectations. The current sentiment was better than expected, |

Click to enlarge. |

| while future expectations where slightly under the market consent. |

Click to enlarge. |

Brexit

A combination of Brexit anxiety as the opinion polls suggest a tight contest and more signs that make last week’s US jobs report an outlier, including a larger than expected, fall in yesterday’s weekly jobless claims, appear to be weighing the on the euro against the dollar. Also, many expect the most Fed officials will likely keep their dot plots consistent with two rate hikes this year.

Brexit angst may also be a factor helping drive down interest rates in Germany and Japan, where new record low bond yields are being recorded. Sterling is trading a little heavier but found a bit in front of $1.44. It finished last week near $1.4520. The spot market is not showing the full strain of Brexit fears. One-month implied volatility is near 23.5% today. It finished last week just above 20% and was near 16.5% two weeks ago. Following Lehman’s demise, implied one-month sterling volatility reached 30%. Also, the premium of sterling puts over calls equidistant from the money (25 delta) continued to increase. Today, premium stands near 7.8%. At the end of last week, it was near 6.2% and the week before it was around 5.5%.

Equities and weak and bond yields are lower. These two considerations also support the yen. The dollar managed to bounce a full yen off the JPY106.25 low seen in Asia yesterday. While the greenback may head back towards that low, barring a large drop in US equities, it is unlikely to reach it in North America today. US participants may be reluctant to take the dollar lower than where Japanese money ostensibly took it yesterday, especially ahead of the weekend, and perhaps ahead of next week BOJ meeting. Most do not expect a change in the BOJ stance ahead of the July 10 upper house election, but given Governor Kuroda willingness to surprise the market, many are not ruling it out entirely.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: Canadian Dollar,France Industrial Production,FX Daily,Italy Industrial Production,Japanese yen,newslettersent,U.S. Consumer Confidence