Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

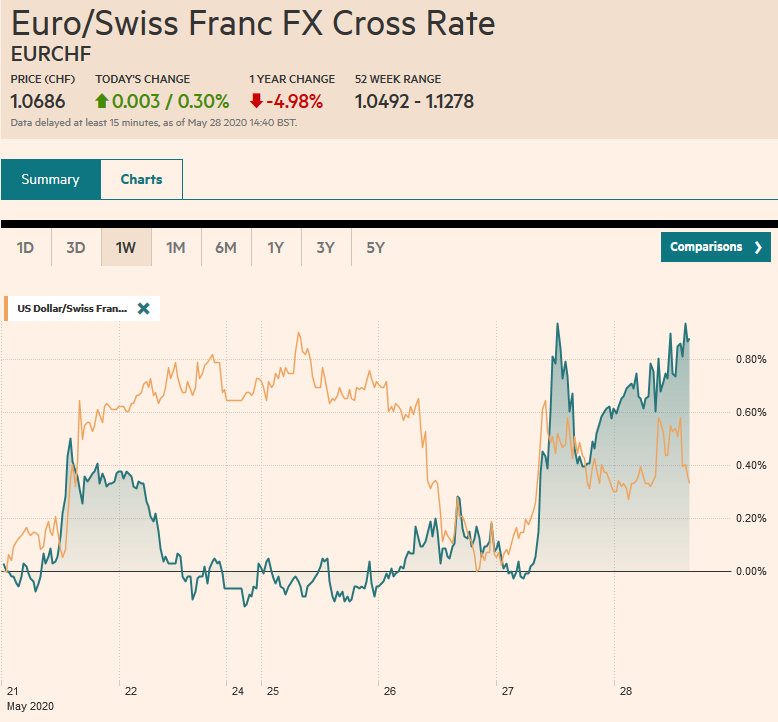

Swiss FrancThe Euro has risen by 0.30% to 1.0686 |

EUR/CHF and USD/CHF, May 28(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The US Secretary of State’s announcement that the autonomy of Hong Kong could no longer be affirmed did not derail the rally in US equities. However, the threat of an executive order against social media companies may be discouraging follow-through buying, leaving US equities little changed ahead of the open. In contrast, Asia Pacific and European equities are mostly higher. In the East, Hong Kong shares were heavy, and South Korea and Taiwan equities softened. However, the Nikkei rallied more than 2% (outstripping the Topix, whose ETFs the BOJ buys). Australia and India’s stocks also rallied. Europe’s Dow Jones Stoxx 600 edged higher to new highs since March 9. It has made higher highs each session this week. Benchmark 10-year yields are mostly 1-2 bp lower, leaving the US 10-year around 68 bp. The dollar is stronger against nearly the majors, with the Norwegian krone and the Canadian and Australian dollars bearing the brunt. Among emerging market currencies, the South Korean won, where stocks sold off despite the central bank halving the seven-day repo rate to 25 bp, is among the heaviest, alongside the Turkish lira. The Chinese yuan’s roughly 0.15% uptick makes it among the strongest currencies today. Gold extended its rebound after slipping to a two-and-a-half-week low yesterday near $1695 to trade around $1720. Oil prices are trading lower following the unexpected rise in US inventory and signals from Russia that it may balk at proposals to extend OPEC+ sharpest output cuts. |

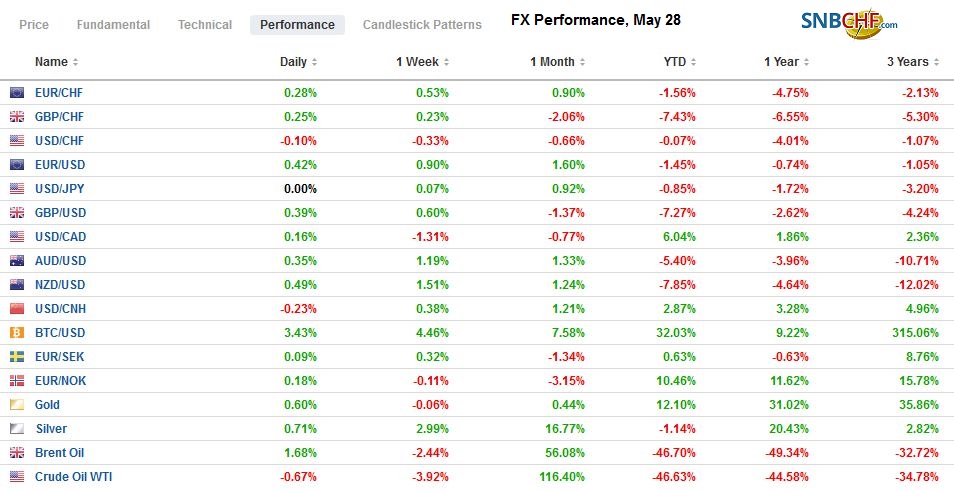

FX Performance, May 28 - Click to enlarge |

Asia Pacific

The PBOC set the dollar’s reference rate at CNY7.1277, which was a bit weaker than the CNY7.1322, the median of several bank models. The market does not seem to recognize the fix as a strong protest against the yuan’s weakness, and the dollar remained above CNY7.15. While the dollar traded within yesterday’s range against the offshore yuan, it remained firmer, and in late European morning turnover, the dollar was near CNH7.18 compared with CNH7.1660 late yesterday. In an interview on CNBC-Asia before the mainland open today, I suggested that while Chinese intentions are not clear, it is difficult to see how there can be de-escalation in the near-term, especially given the US political cycle. This may weigh on the yuan, and trying to provide some sense of the magnitude, I suggested the dollar could rise toward CNY7.40 in the period ahead.

While the escalation of US-China tensions makes for front page reading, China and India have already had a minor clash, and both sides have reinforced their positions near the Ladakh region. There was a war there in 1962, and there have been occasional flareups since then, most recently in 2017. Last summer, India changed the status of the region, bringing it more under the federal government’s control. Earlier this month, Chinese and Indian troops came to blows along the banks of the Pangong Tso. Inconclusive talks were held over the past couple of weeks. Now both countries have reinforced troops and apparently artillery.

Like many countries, Japan is going to dramatically increase its bond issuance this year to around JPY212 trillion (~$2 trillion). Many expect the BOJ to step up its purchases again after the yield curve control has seen it reduce its bond purchases. Meanwhile, for foreign investors, the new supply did not deter buying Japanese bonds on a hedged basis, which can generate better than Treasury yields. Last week, according to Ministry of Finance data, foreigners bought about JPY550 bln of Japanese bonds, the most in three months. For their part, Japanese investors stepped up their purchases of foreign stocks. The JPY813 bln purchases were the second-highest of the year and more than the past five weeks put together.

The dollar has been confined to a 10-tick range on either side of JPY107.80, seemingly sandwiched between the nearly $400 mln expiring option at JPY107.75 and the $1.8 bln option at JPY107.90. Near 5.1%, the implied three-month volatility is at its lowest level since late February. The Australian dollar is straddling the $0.6600 area. The upside momentum appears to have stalled. Its own tensions with China (barley and beef) appear to be also impacting thermal coal exports. As part of China’s “import substitution” strategy, Beijing wants the coastal utilities to buy domestic coal. We note that the forward points for the Hong Kong dollar slipped a little today but remain highly elevated.

EuropeGerman Chancellor Merkel warned that the fiscal initiative from the EU might not be agreed upon next month. Although Austria, one of the so-called Frugal Four, seemed open to the possibility of grants alongside loans, Denmark, another remember, insisted only loans. Also, Eastern and Central Europe are balking after not being consulted and again facing a Berlin-Paris fait accomplice. Both Czech and Estonia expressed opposition. |

Germany Consumer Price Index (CPI) YoY, May 2020(see more posts on Germany Consumer Price Index, ) Source: investing.com - Click to enlarge |

Many who embraced the Berlin-Paris proposal as the watershed seem to de-emphasize the German Constitutional Court ruling that questioned a very basic and essential legal principle of the European project, namely that EU law is primary (over state law). Compromises are still being sought that seem to uphold the German court ruling. The lower chamber of the German parliament suggested today that the ECB merge the Public Sector Purchase Program, which the court ruled on, with the Pandemic Emergency Purchase Plan that it did not reject.

The ECB is expected to boost its PEPP bond-buying as early as next week. Meanwhile, Spain reported a negative CPI for May for the second consecutive month on a year-over-year basis (-0.9% after -0.7% in April). The May CPI reading from German states suggests the country’s CPI may have been halved to about 0.4% in May. Separately, in an op-ed piece, Bank of England Governor Bailey discussed the possibility of taking “unprecedented” monetary measures.

The euro made a marginal new high for the move near $1.1035, but it is quiet in late morning dealings in Europe, just below the 200-day moving average near $1.1010. There are two sets of expiring options to note. The first is for a little more than 600 mln euros at $1.0995, and the other is for about 675 mln euros at $1.1020. The intraday technicals suggest upside potential in the North American morning. Sterling is consolidating in about a quarter-cent range on either side of $1.2260, roughly where it closed the North American session yesterday. Meanwhile, the euro continues to knock on the recent cap near GBP0.8900.

America

Trump is said to be considering a range of options now that it officially recognized that Hong Kong is not autonomous. There are many options, including taxing HK imports as it does with the mainland, limit the sales of advanced technological goods, and/or impose restrictions on investments. It could restrict visas, freeze assets, sanction individuals, or entities. At the same time, it does not want to punish the HK people themselves, but it may difficult to sustain the differentiation in practice. Separately, the Supreme Court of British Colombia ruled yesterday against the Huawei CFO Meng Wanzhou, and the extradition hearing will continue. Recall that over the past weekend, the UK confirmed what had been hinted, namely that the UK will gradually reduce the presence of Huawei in its 5G carve-out of the next few years. Also, by a nearly unanimous vote, the House of Representatives approved a bill that already passed the Senate without dissent that empowers the President to sanction Chinese officials for the treatment of Uighur Muslims, which also underscores the bipartisan US stance toward China.

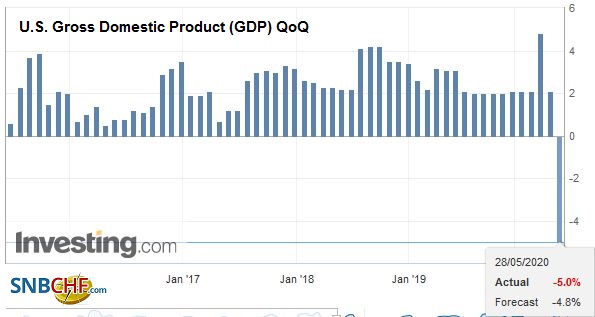

| The US reports April durable goods orders today, which are widely expected to be dreadful. On the other hand, the Kansas City Fed’s manufacturing survey for May is expected to show some moderation as have nearly every other survey for this month. Fed Presidents Williams and Bullard suggested the economy is near its low point. Weekly initial jobless claims remain elevated and likely were around two million last week. The peak was near 6.8 mln in late March. A revised Q1 GDP report is too historical to have much market impact. Canada reports its Q1 current account deficit, which is around C$10 bln. The 2019 quarterly average was about C$11 bln. It is not typically a market mover. |

U.S. Gross Domestic Product (GDP) QoQ, Q1 2020(see more posts on U.S. Gross Domestic Product, ) Source: investing.com - Click to enlarge |

The US dollar is finding support near CAD1.3730. Resistance is likely near previous support in the CAD1.3800-CAD1.3850 area. The broader risk environment continues to seem more important than the price of commodities, including oil. The US API surprised yesterday with an estimate showing an 8.7 mln barrel inventory build. The EIA estimate is seen as more authoritative. Economists forecast the third consecutive weekly decline (~2 mln barrels in the Bloomberg survey) prior to the API data. The Mexican peso is also consolidating its recent rise. Yesterday, Banxico warned the economy may decline by 4.6%-8.8% this year, but that core inflation may accelerate until Q4. Recall that the MXN22.15 area, which is proved sticky for the dollar in recent days, corresponds to the halfway mark of this year’s range.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,$CNY,Currency Movement,ECB,EUR/CHF,FX Daily,Germany Consumer Price Index,Hong Kong,newsletter,OIL,U.S. Gross Domestic Product,U.S. Gross Domestic Product QoQ,USD/CHF