Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

Swiss FrancOnce again both EUR and USD broke down against the franc. The adverse effect of the Friday US jobs reports is visible again. |

|

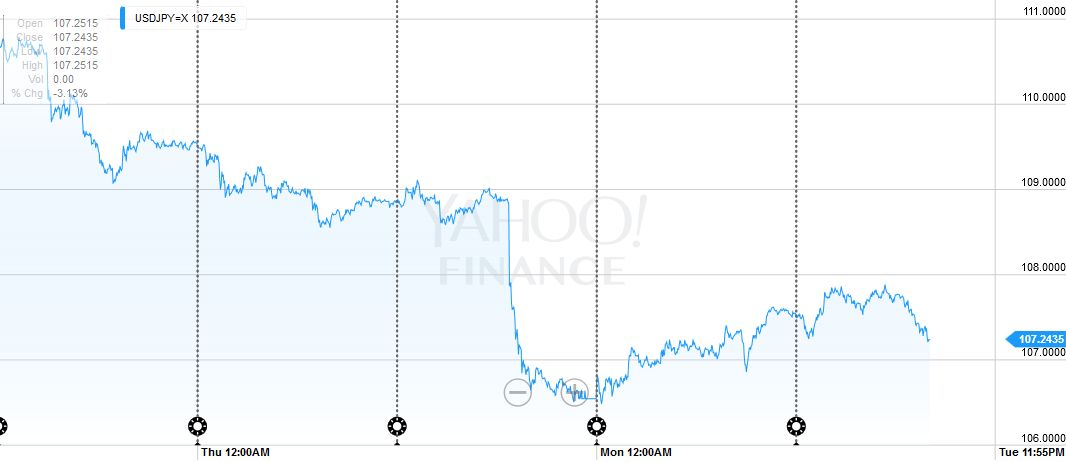

JapanThe Japanese yen is the major currency not to be gaining against the US dollar. Emerging market currencies, save the Chinese yuan, are also advancing against the greenback today. The yen rose 3.5% against the dollar last week, and rising equities and commodities are weighing on the yen. The dollar rose to almost JPY108 in Asian trading is consolidating in the European morning. The JPY108.30 area is the first retracement objective, which is a little above the five-day moving average (~JPY108.05).

|

USD/JPY – click to enlarge. |

United KingdomThe third development today is sterling’s strength. Sterling inexplicably shot up almost two cents in a matter of minutes in Asia (~$1.4475 to $1.4660). It quickly came off amid talk of a trading error. However, on the push back, it found support near $1.4500 and managed to trade back above $1.4600 in the European morning. One-month implied volatility is making new highs today above 22% (it was near 16.6% on May 27) and the put-call skew is at a new record extreme (~6.9%). UK stocks are underperforming, but the FTSE is the best performingG7 equity market over the past week. UK gilts are also underperforming, with 10-year yields three bp higher near 1.30%, while most eurozone benchmark yields are lower.

|

USD/GBP – click to enlarge. |

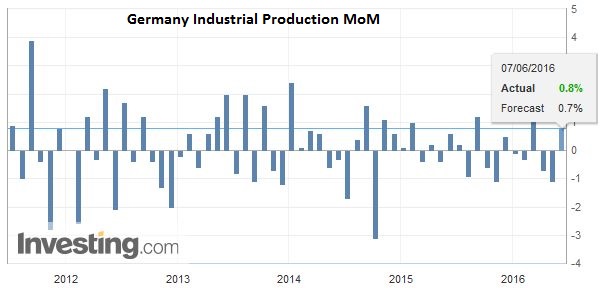

Euro zoneFourth, yesterday’s unexpectedly poor German factory orders (-2.0% vs. expectations for a 0.5% fall) left investors ill-prepared for the stronger than expected industrial production report today. The 0.8% gain follows a revised 1.1% decline in March (initially -1.3%) and February (-0.7%). Going back to through the second quarter last year, German industrial output has risen only one month every quarter. The weak orders data warn that although output began Q2 on a firm note, there may not be much follow-through.

|

Economic Events June 07, 2016  Click to enlarge. |

| If, as we have argued, the euro is correcting the slide from May 3 (~$1.1615) to May 30 (~$1.11), then at its current level (~$1.1370) is has retraced 50% of the move. The next retracement is found near $1.1420. |

Click to enlarge. |

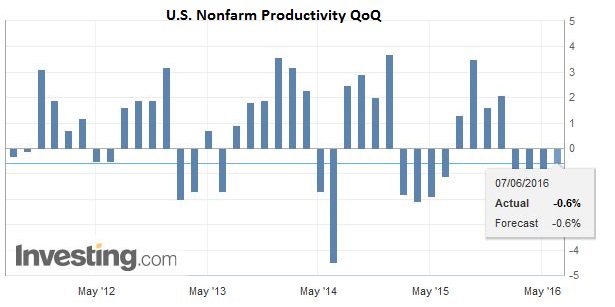

United StatesThe US economic data today is not the kind that moves the markets. Non-farm productivity is likely to be revised up following the upward revision to Q1 growth. However, it will likely remain negative, and the weak productivity growth remains an important economic puzzle. Unit labor costs may edge lower from the 4.1% initial estimate. Consumer credit is due out late in the session. After a record level (~$29.7 bln ) in March, a return to trend (six-month average is ~$18.4 bln) is expected. Canada reports the IVEY PMI. A softer number from April’s 53.1 reading is anticipated. The US dollar is approaching the CAD1.2740 area, which is the retracement of May’s run-up.

|

Major Economic Events Tuesday June 7 – Click to enlarge. |

| Unit labor costs may edge lower from the 4.1% initial estimate. Consumer credit is due out late in the session. After a record level (~$29.7 bln ) in March, a return to trend (six-month average is ~$18.4 bln) is expected. Canada reports the IVEY PMI. A softer number from April’s 53.1 reading is anticipated. The US dollar is approaching the CAD1.2740 area, which is the retracement of May’s run-up. |

Click to enlarge. |

Graphs and additional information on Swiss Franc by the snbchf team

Tags: Asian bloc,Barack Obama,Donald Trump,Eurozone Gross Domestic Product,FX Daily,Germany Factory Orders,Germany Industrial Production,Hillary Clinton,Japanese yen,newslettersent,U.S. Nonfarm Productivity,U.S. Unit Labor Costs,usd-jpy