Read More »

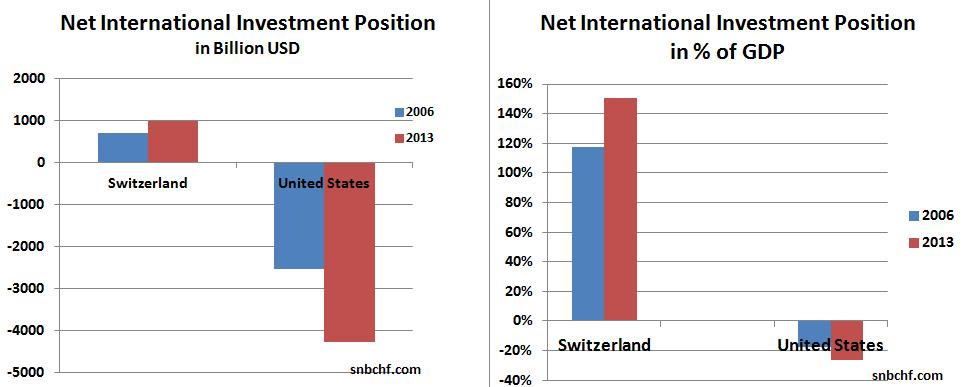

On Swiss National Bank Main SNB Background Info

On Swiss National Bank Main SNB Background Info

Das ändert sich im Mai! #finanzen #änderungen #mai

Das ändert sich im Mai! #finanzen #änderungen #mai2 May 2024

Saisonales Muster: JETZT alle Aktien verkaufen?

Saisonales Muster: JETZT alle Aktien verkaufen?2 May 2024

Gemeinschaftskonto mit Partner: Sinnvoll oder gefährlich?

Gemeinschaftskonto mit Partner: Sinnvoll oder gefährlich?2 May 2024

Ray Dalio on Pairing Gut Instinct & Logic

Ray Dalio on Pairing Gut Instinct & Logic2 May 2024

Ukraine: WARUM verschweigt man diesen Skandal?! (EILT)

Ukraine: WARUM verschweigt man diesen Skandal?! (EILT)2 May 2024

Horror: E-Auto Schock für SIXT!

Horror: E-Auto Schock für SIXT!2 May 2024

Wichtige Morning News mit Oliver Klemm #291

Wichtige Morning News mit Oliver Klemm #2912 May 2024

ALQUILERES DISPARADOS. FRACASO DE LA LEY DE VIVIENDA

ALQUILERES DISPARADOS. FRACASO DE LA LEY DE VIVIENDA2 May 2024

The technical roadmap for the EURUSD, USDJPY and GBPUSD through the FOMC rate decision

The technical roadmap for the EURUSD, USDJPY and GBPUSD through the FOMC rate decision1 May 2024

Thüringen: Völliges Wahl-Chaos!

Thüringen: Völliges Wahl-Chaos!1 May 2024

Why Financial Advice Fails & What to Do Instead – Robert Kiyosaki & Ron Willoughby

Why Financial Advice Fails & What to Do Instead – Robert Kiyosaki & Ron Willoughby1 May 2024

AUDUSD corrects higher and tests MA and retracement levels ahead of the FOMC decision.

AUDUSD corrects higher and tests MA and retracement levels ahead of the FOMC decision.1 May 2024

Bereithalten! Das wird eine Top Kauf-Chance!

Bereithalten! Das wird eine Top Kauf-Chance!1 May 2024

Gold vs Silver: Which Precious Metal Should You Invest In?

Gold vs Silver: Which Precious Metal Should You Invest In?1 May 2024

USDCAD modestly corrects lower after the break higher yesterday

USDCAD modestly corrects lower after the break higher yesterday1 May 2024

EL ENGAÑO DEL GRADUALISMO: El Fracaso del Keynesianismo

EL ENGAÑO DEL GRADUALISMO: El Fracaso del Keynesianismo1 May 2024

Washington – We Have a Problem!

Washington – We Have a Problem!1 May 2024

Darum werden 90% aller Bitcoin Händler Ihr Geld verlieren

Darum werden 90% aller Bitcoin Händler Ihr Geld verlieren1 May 2024

The USDCHF broke yesterday to the upside. What keeps the buyers in control?

The USDCHF broke yesterday to the upside. What keeps the buyers in control?1 May 2024

Wahnsinn: So werden die Bürger von Lindner geschröpft!

Wahnsinn: So werden die Bürger von Lindner geschröpft!1 May 2024