Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

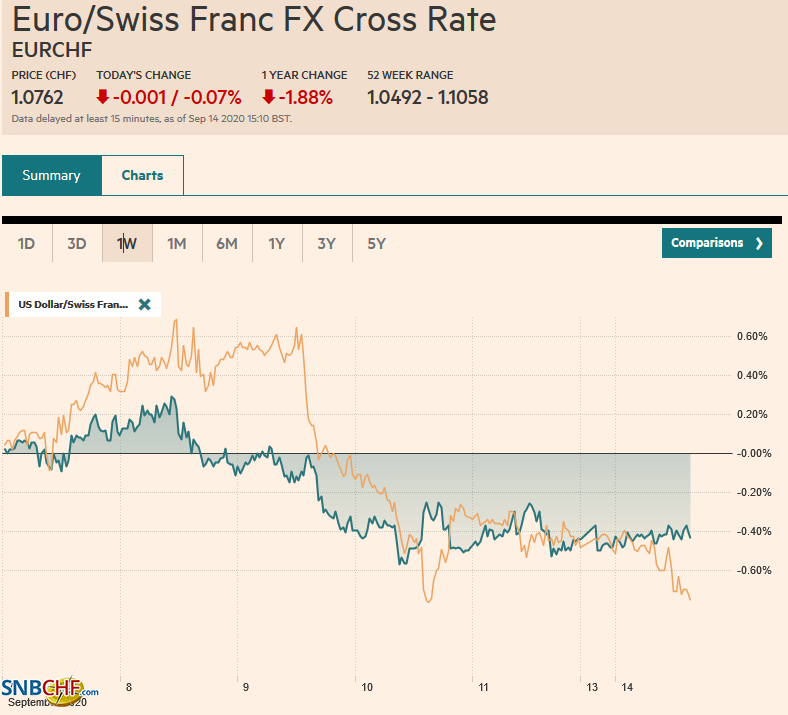

Swiss FrancThe Euro has fallen by 0.07% to 1.0762 |

EUR/CHF and USD/CHF, September 14(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: A flurry of deals, including the still-evolving Oracle-TikTok tie-up, helped lift equity markets in the Asia Pacific region. South Korea’s Kospi, and Indonesia, which had been battered last week, led the advance. The MSCI Asia Pacific Index rose for the third consecutive sessions. European bourses are little changed while US stocks are firmer. The S&P 500 could gap higher at the open. Benchmark bond yields are 1-3 bp lower in Europe, and the periphery is doing better than the core. The US 10-year yield is near 66 bp. The dollar is mostly lower, though the Australian is an exception, and is slightly lower. Among the emerging market currencies, the Turkish lira is the outlier. It was trading heavily in the aftermath of Moody’s unexpected downgrade ahead of the weekend (B2) and maintained a negative outlook. Gold is firm but in the middle of the $1900–$2000 range, and October WTI is narrow range but looking heavy despite Tropical Storm Sandy threatening Gulf oil platforms. The busy week that features OPEC’s meeting and three major central banks (Fed, BOJ, and BOE) is off to a slow start. |

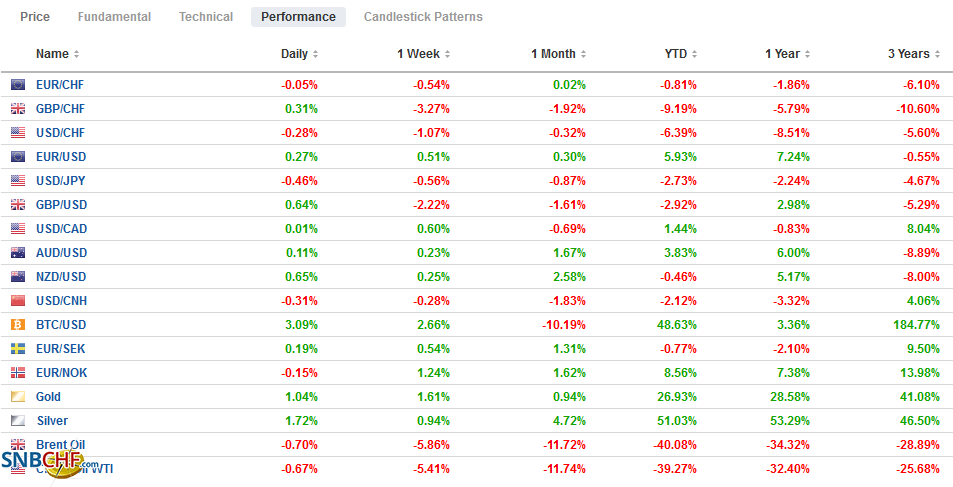

FX Performance, September 14 - Click to enlarge |

Asia PacificWithin 48 hours or so of China’s Xi virtual meeting with Merkel, Michel, and von der Leyden, Beijing announced a complete ban on German pork and related products. A case of African swine flu was detected in Germany, but rather than reject pork from that area, like the EU has, China as banned all of German pork. Germany was China’s third-largest pork supplier behind the US and Spain. Many suspect that what looks like an overreaction is designed to send a signal to Berlin, the largest country in the EU. The EU has threatened new restrictions on Chinese investment as due primarily to its heavy use of state aid. Separately, the EU imposed anti-dumping duties (50.3%-66.4%) on Chinese steel road wheels for five years in March and followed that up with tariffs (17.2%-27.9%) on corrosion-resistant steel imports were some Chinese producers work around the initial tariffs. Ostensibly, the ban on German pork could boost China’s imports of US pork, which would be helpful for the Phase 1 trade agreement. However, it would serve China’s purposes better if it blamed a reduction of German pork imports on the American’s who insist on bypassing the marketplace and securing a fixed dollar share of China’s market. |

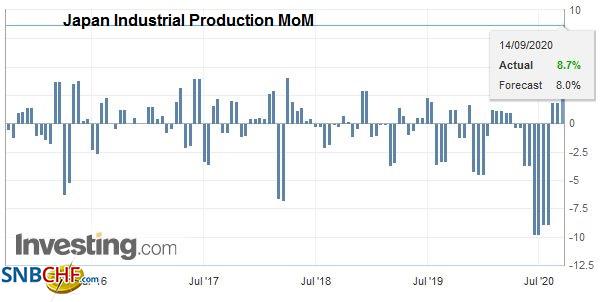

Japan Industrial Production MoM, July 2020(see more posts on Japan Industrial Production, ) Source: investing.com - Click to enlarge |

The LDP has selected Suga as Abe’s replacement as head of the LDP. On Wednesday, the Diet will choose him as the new Prime Minister. Suga had initially hinted that another rise in the controversial sales tax might be needed but has now pushed it out at least a decade. The BOJ meets later this week, but the focus is on the trajectory of fiscal policy. Suga seemed sympathetic to another budget (it would be the second extra budget this year) and suggested (along the lines of MMT) that there was no limit on bond issuance. The Japanese economy contracted for the past three quarters, and the recovery here in Q3 appears restrained. Earlier today, Japan reported its tertiary index in July fell by 0.5%. The median forecast in the Bloomberg survey was for an increase of the same magnitude. The June series was revised to a 9% gain from 7.9% initially. On the other hand, the July industrial production figures were revised higher to show an 8.7% gains instead of 8.05.

The dollar is straddling the JPY106.00 level. It is trading within last week’s relatively narrow range (~JPY105.80-JPY106.40). A nearly two-week downtrend line is near JPY106.20 today. A break of last week’s lows opens the door to JPY105, the lower end of the trading range since the end of July. The Australian dollar is in around a 20-tick range above $0.7270. It looks poised to move higher in the North American session, but the market does not appear to ready to challenge the month’s high a little above $0.7400. Nearby resistance is seen in the $0.7310-$0.7330 area. The Chinese yuan has strengthened against the US dollar for the past seven weeks and is off to another strong start. The greenback has fallen through last week’s lows (~CNY6.8265) and looks set to challenge the September 1 low (~CNY6.8125). The critical question is, what interest does a strong yuan serve? One thing it does is ostensibly make imports cheaper, and China appears to be stepping up imports to meet the Phase 1 US trade commitment, and more broadly, appears to be stockpiling commodities as its relationships with others fray.

EuropeThe nearly universal criticism of the move by the UK government to abrogate the Withdrawal Agreement and Northern Ireland Protocol is not preventing Prime Minister Johnson from moving forward. The second reading of the Internal Market Bill will be held today. The government’s Justice Secretary has threatened to resign. Three former Prime Minister has cautioned against this action. The move is the equivalent to throwing one’s steering wheel out the window n a game of chicken, demonstrating its resolve to seek its own way if the EU does not compromise more on trade issues (fisheries, state-aid, among others). Separately, other reports suggest the UK will soon announce at least a partial pull out of the EU human rights law). |

Eurozone Industrial Production YoY, July 2020(see more posts on Eurozone Industrial Production, ) Source: investing.com - Click to enlarge |

The aggressiveness of the move caught many officials, let alone investors, off-guard. Recall the tortured history of the Withdrawal Bill. Johnson resigned from May’s government over it. Her version was widely disliked, but it did not create a border between the UK and Northern Ireland. Johnson later negotiated a different Withdrawal Agreement and threatened to expel any Tory MP that did not support it. Johnson led the Tories to a parliamentary majority in part based on Withdrawal Agreement. Now he proposes reneging on key elements. The EU is threatening a legal response and may not wait for the bill to be approved. It would seem that the European Court of Justice would hear such a case until the official Withdrawal Agreement arbitration panel is in place in early 2021.

Adding insult to injury, the UK made a concession to Japan in the free-trade agreement struck in principle at the end of last week that it refuses to make to the EU. In essence, Japan simply rolled over the deal struck with the EU that was implemented in 2019 that includes some broad limits on state aid. In negotiations with the EU, the UK has insisted on absolute freedom within the framework of the WTO. This may prove problematic to sustain the cognitive dissonance under closer scrutiny.

Many observers disapproved of ECB President Lagarde’s comments about the euro’s exchange rate. They wish that she had echoed the concern of other members, including the Chief Economist Lane. In its editorial, the Financial Times was critical of what it called “lukewarm euro intervention.” That there is a wider range of opinions at the ECB than say at the Federal Reserve or the Bank of Japan is not new news, but there can be no mistake that what Lagarde says, what Powell says, or Kuroda carries more weight than any individual member. They speak for the institution. Of course, sometimes they are off message, but Lagarde was not. She acknowledged both at the meeting and subsequently that the ECB was carefully monitoring the euro and that its strength adversely impacts the inflation and blunts the economic stimulus.

It was only “lukewarm intervention” if one thinks it ought to have a stronger reaction. Otherwise, it was balanced comments, with an indication that it will be “closely monitored.” Many want to measure the euro’s appreciation from its pandemic-panic low, but that is not fair. Nor is accepting the August’s low inflation as a meaningful indication of the euro’s appreciation in July (as it was flat net-net in the first half) compelling. The cut in the German VAT, shifting summer sales, depressed prices for summer holidays make for a high noise-to-signal ratio.

The euro’s gains stalled near the pre-weekend high that was set near $1.1875. There is a 1.2 bln euro option at $1.19 that expires today. Initial support is now around $1.1840. Tomorrow, an option for 2.2 bln euros at $1.1850 rolls off. The euro has ended a six-day slide with now a four-day advance. Despite the worries about the euro’s rise, it has been moving broadly sideways for six weeks. The weaker dollar has stalled sterling’s markdown. For the third session, it has found bids near $1.2765-$1.2775. Chart resistance is likely in the $1.2900 area. At the same time, the euro appears to have peaked in the GBP0.9270-GBP0.9300 area. Recall that the euro was trading below GBP0.8900 as recently as September 3.

America

With a new fiscal support package impossible to negotiate, President Trump took $44 bln of funds earmarked for disaster relief and shifted into unemployment compensation ($300 a week). The funds have been exhausted, but FEMA assures that there are funds for states still setting up their programs for six weeks back-dated to August 1. At least five states have already begun paying out. The payment to two million New Yorkers is to start this week.

Guarded optimism on a Covid vaccine is on the rise again. AstraZeneca/Oxford are set to resume their vaccine tests in the UK and Japan this week. Pfizer’s CEO said it was likely the US would begin rolling out a vaccine before year-end.

Tomorrow the US reports the September Empire State manufacturing survey and August industrial output figures. The Empire State survey disappointed in August but seemed to have been an outlier and, in any event, is expected to have ticked up. August industrial production is expected to have risen a solid 1% in the month after a 3% gain in July. Manufacturing is expected to be stronger still. August retail sales will be reported before the outcome of the FOMC meeting on September 16. The components that are used for GDP calculations are expected to have gained 0.3% after July’s 1.4% gain. The headline is projected to have increased by 1% (July 1.2%).

The economic highlight for Canada this week include CPI in the middle of the week, which should remain firm, and retail sales at the end of the week that should show a dramatic moderation after the heady 23.7% rise in July. Excluding autos, retail sales are expected to have increased by 0.5% (15.7% in July). Mexico has a light schedule. Brazil’s central bank meets on September 16, and after slashing the Selic rate to 2.0% from 4.5% at the end of last year, there is little room or appetite for additional cuts. The impact of currency depreciation is likely to begin lifting inflation readings.

The US dollar’s recovery from the dip below CAD1.30 at the start of the month stalled last week near CAD1.3260. The lower end of the near range is around CAD1.3120. North American operatives may a better greenback selling opportunity on a push above CAD1.3200. The US dollar has fallen against the Mexican peso for the past five weeks. It recorded new six-month lows today near MXN21.18. Immediate resistance is around MXN21.25 and MXN21.30. Provided that latter holds, the greenback is likely to continue the push toward MXN21.00.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,Brexit,China,COVID-19,Currency Movement,EUR/CHF,Featured,newsletter,Turkey,USD/CHF