Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

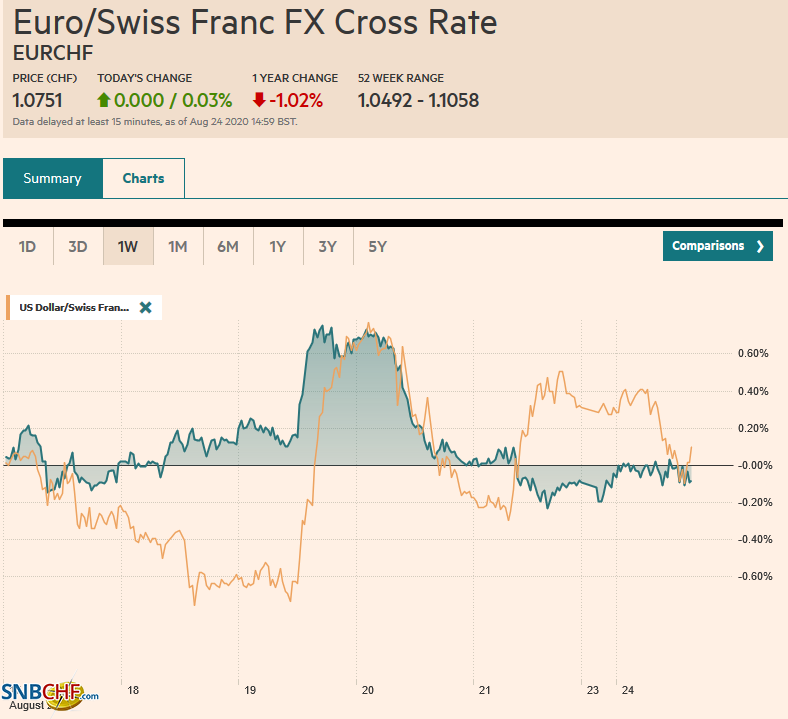

Swiss FrancThe Euro has risen by 0.03% to 1.0751 |

EUR/CHF and USD/CHF, August 24(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: New virus outbreaks in Europe and Asia are not adversely impacting the capital markets today. Global equities are firmer. Some reports suggesting the US ban on WeChat may not be as broad as initially signaled helped lift Hong Kong shares, but nearly all the markets in the region traded higher. Europe’s Dow Jones Stoxx 600 is following suit. Last week’s 0.8% loss if being offset with today 1.7% gain through the European morning. US shares are firmer, and after setting a new record ahead of the weekend, the S&P 500 is poised to gap higher. European and US benchmark yields are 1-2 bp higher, putting the 10-year Treasury yield near 64 bp. Yields in the Asia Pacific region eased, in line with US slippage before the weekend, and new that the Reserve Bank of New Zealand missed its bond purchases. The dollar is weaker across the board. The Turkish lira is a notable exception in the emerging market space. The JP Morgan Emerging Market Currency Index is about 0.3% higher to recoup most of its pre-weekend loss. Gold is firm but holding below the $1955 area that capped the yellow metal in the past two sessions. Two storms in the US Gulf that have shut down nearly half of the rigs in the regions have helped steady oil prices and snap a four-day decline in the October WTI contract. |

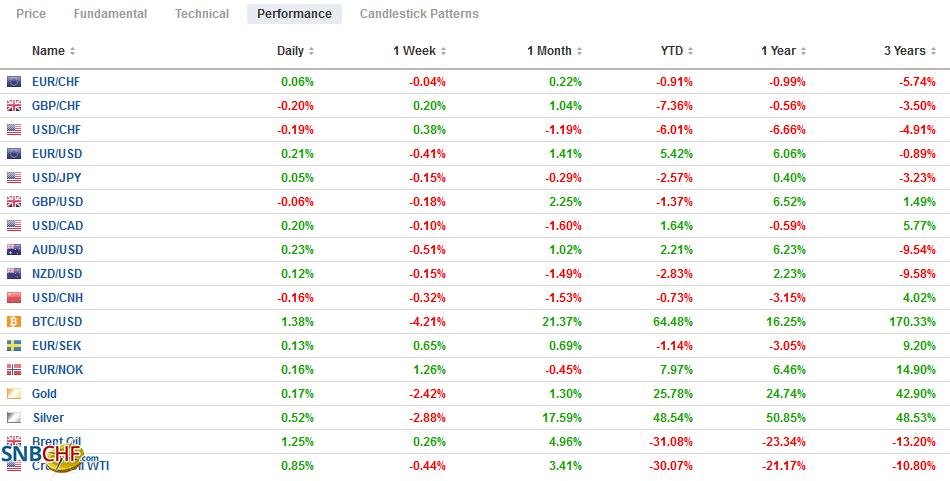

FX Performance, August 24 - Click to enlarge |

Asia Pacific

The discretionary authority of the US president on national security issues makes the situation less than transparent. However, reports suggest that President Trump has reassured US executives that the ban on WeChat will not be as extensive as initially feared. Meanwhile, TikTok is preparing to challenge the executive order that appears to be forcing a sale. It seems premature to draw any implications about the US-China relationship. The discretionary authority and fear of wider sanctions are prompting some fund managers to shift their holdings of Chinese companies to their Hong Kong listing from the US.

Rumors of Japan’s Prime Minister Abe’s health continue to swirl. Reports suggest he visited a hospital earlier today, for the second time in around a week. Abe claimed he was getting the results of last week’s tests, while other reports suggest he was getting treatment for a chronic condition.

The US dollar is in a narrow range against the Japanese yen and has largely been stuck in a 25 tick range above JPY105.70. There are options for about $885 mln struck between JPY106.00 and JPY106.07 that expire today. Last week’s high was around JPY106.20. The Australian dollar snapped an eight-week advance last week with a minor decline (~0.15%) but has begun the new week on a firm note, though within the pre-weekend range (~$0.7140-$0.7215). It set a two-year high near $0.7275 last week. The greenback has fallen against the Chinese yuan for the past four consecutive weeks. The PBOC set the dollar’s reference rate at CNY6.9194, while the bank models were closer to CNY6.9183 (median in the Bloomberg survey). It also injected CNY110 bln into the banking system, allowing the seven-day repo rate to ease nine basis points after rising in the second half of last week.

Europe

Last week’s trade talks between the UK and the EU failed to make much headway. Although the end of the standstill arrangement is not until the end of the year, it is recognized that an agreement by the mid-October EU summit is necessary to ensure the ratification process is completed. UK officials are reported stepping up efforts to prepare for no deal.

Speculators ended their six-week accumulating spree in the euro futures. The 6.8k liquidation of gross long positions was the first decline since late June, though, at more than 259k contracts (August 18), it is still for all practical purposes at a record high (~266.1k August 11). For the first time since mid-April, the net speculative position in sterling is now long. The bulls have been persistently adding to their long sterling position in the futures market. The gross long has grown in 13 of the past 16 weeks and finally outstrips the gross short speculative position. While the longs have increased over the past three weeks, the gross shorts have reduced. Around 47.8k contracts, the gross short position is the smallest in two months. Before this month, the gross speculative short sterling position in 13 of the previous 15 weeks.

The euro is trading well within the pre-weekend range (~$1.1755-$1.1885) and is poking around the $1.1835-area, session highs in late morning turnover in Europe. Intraday technical indicators are stretched, but new high toward $1.1860 can’t be ruled out. The euro has been consolidating this month above $1.17 and has only settled once above $1.19. Unable to push sterling below $1.3080, European participants have taken it higher to around $1.3130. Nearby resistance is seen near $1.3150. Sterling stalled last week after making new highs for the year (~$1.3265) and was sold to the week’s lows ahead of the weekend (~$1.3060). Fitch cut the outlook for Turkey’s credit rating to negative from stable at the end of last week. The lira is under pressure today, and the dollar approached TRY7.40.

America

President Trump has expedited the use of plasma from people with Covid antibodies, and some reports have been subsequently denied about allowing emergency use of the AstraZeneca/Oxford vaccine. Separately, one investment bank estimates that a quarter of the US temporary layoffs will be permanent. Calculation by the Economist estimated that an American wearing a mask for a day prevents a $56.14 fall in GDP.

The economic calendar is light to begin the week. The Chicago Fed’s National Activity report rarely draws much attention. After a big jump in May, it leveled off in June and may have slipped lower in July. The big event this week is the Jackson Hole symposium, at which Powell will speak Thursday. In terms of economic data, the July personal income and consumption reports may be the most impactful. The highlight from Canada will be the June GDP figures at the end of the week. Today’s bi-weekly CPI for Mexico is not typically a market mover. The central bank’s inflation report (August 26) and the minutes from the recent meeting (August 27) may shed light on the trajectory of monetary policy going forward. Many, including ourselves, see scope for another cut in Q4.

The Canadian dollar is the strongest currency in the world so far this month, appreciating about 1.8% against the greenback, ahead of second-place Norwegian krona’s 1.4% gain. However, speculators do not seem to be profiting much. As of August 18, they had the biggest net short position in two and a half months. The bulls added 2.2k contracts to their gross long position, but near 19.4k contracts, it is at the smaller-end of its positioning in the past decade. The bears added 6.3k contracts and 10k over the past two weeks to 53.1k contracts, the most since the end of April. Up nearly 1.6% this month, the Mexican peso is the best performing emerging market currency, a little ahead of the Malaysian ringgit (~1.5%). Speculators have a small net long position. Speculators had a large gross long position of over 200k contracts for most of the first six weeks of the before the Covid-crisis struck. The bulls did not regain their composure until mid-May when the gross longs had fallen to around 22.5k. It had recovered to nearly 60k contracts, but as of August 18 was back to nearly 42.5k contracts. The bears seem cautious, and the gross short position of 38.1k contracts is around half of the recent peak in mid-June.

Scandals in Canada and Mexico have not deterred their respective currency strength. The US dollar fell to a seven-month low against the Canadian dollar last week (~CAD1.3135) and looks poised to push through it, even if not today. Look for some consolidation in early North American turnover that could extend toward CAD1.3180. The greenback closed last week on a soft note against the Mexican peso, at its lowest level in two months. Follow-through dollar selling to start the week has pushed it toward MXN21.9155. Last month’s low was near MXN21.85, and the June low was closer to MXN21.46.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,Brexit,China,Commitment of Traders,Currency Movement,Featured,Japan,newsletter