Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

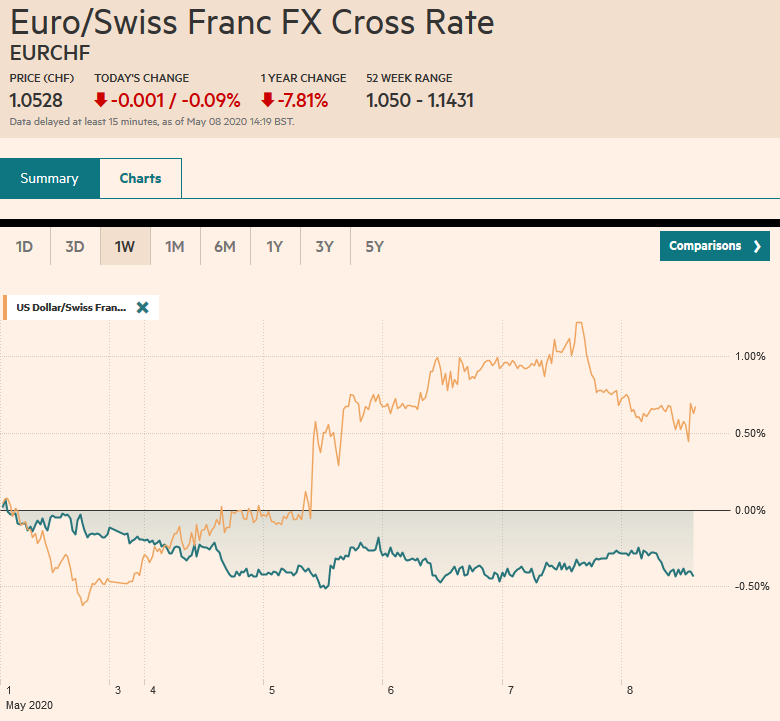

Swiss FrancThe Euro has fallen by 0.09% to 1.0528 |

EUR/CHF and USD/CHF, May 08(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The S&P 500 closed near its session lows for the third day running yesterday but failed to deter the bulls in Asia-Pacific, where most markets rose by more than 1%. Taiwan, Korea, and Australia lagged a bit though closed higher. Europe’s Dow Jones Stoxx 600 is firm, and the modest gains (~0.5%) would be enough to ensure a higher weekly close if it can be maintained. US shares are firm, and the S&P looks poised to probe the week’s high near 2900. Benchmark 10-year yields are mostly softer. Next week’s record quarterly refunding not weighed on the US 10-year, which is practically unchanged on the week near 63 bp. European peripheral yields are off today, led by Italy. Note that later today, Moody’s will update its assessment of Italian credit rating, which now is at the lowest investment grade of Baa3. The dollar is softer against most of the major currencies, though the yen is struggling around unchanged levels. On the week, the euro is the worst-performing major currency off about 1.3% (at ~$1.0840). The Australian dollar is the best, up around 1.5% (at ~$0.6515). Emerging market currencies are firm, but on the week, the JP Morgan Emerging Market Currency Index is slightly softer, coming into today’s session. Gold staged an impressive recovery yesterday, rallying from the week’s low (~$1676) to the week’s high (~$1722) and is consolidating near the highs today. June WTI is also consolidating. It has tried pushing higher in recent days above the $25-level with little success and has found support near $23. The 20% gain on May 5 lifted it to this new range. |

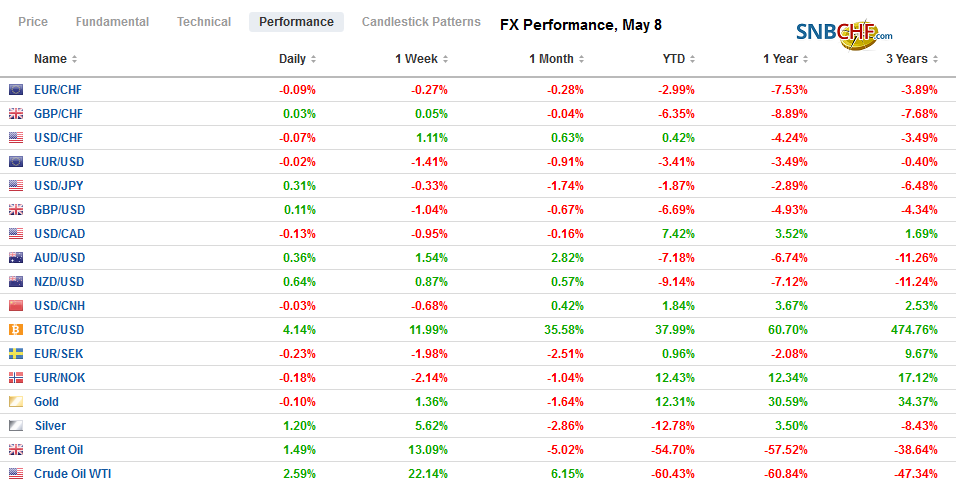

FX Performance, May 8 - Click to enlarge |

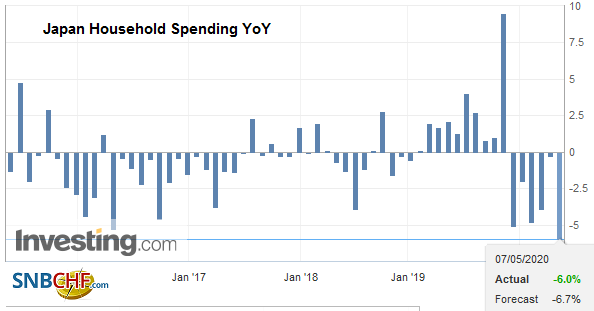

Asia PacificHousehold spending in Japan fell 6% in March from a year ago after a 0.3% decline in February. It was slightly better than expected. Meanwhile, cash wages in real terms fell 0.3% year-over-year after the February figures were revised to show a 0.2% gain instead of a 0.5% increase, which was initially reported. Separately, the final PMI readings for services and the composite were revised lower from the preliminary readings and stand at 21.5 and 25.8, respectively. In February, they were at 33.8 and 36.2. The LDP is proposing a new program to subsidize 2/3 of the rent for small businesses up to JPY500k (~$4.7k) a month for half a year. |

Japan Household Spending YoY, March 2020(see more posts on Japan Household Spending, ) Source: investing.com - Click to enlarge |

The US and Chinese top negotiators discussed the progress on the trade agreement and issued a boilerplate statement that said how both sides are working toward it. It was almost as if it was meant to blunt the threat by President Trump to walk away from the deal if China is not meeting its commitments. The fact of the matter, as we have maintained from day 1, it would be very difficult for the quantitative targets to be met even under the best of circumstances, which these sure aren’t. China agreed to boost imports from the US above 2017 levels, which were higher than 2019, and yet, through the first four months of 2020, China’s imports from the US are off almost 6% from last year’s levels. This is a sort of ticking political bomb, and the US election cycle, where rhetoric is typically escalated, provides a fertile context. We suspect things will come to a head as soon as next month.

The dollar has stabilized against the Japanese yen a little above JPY106, but it is not sufficient to avoid the extension of its loss for a fifth consecutive week. It matches the longest losing streak in a decade. A close above the JPY106.60 area would help stabilize the technical tone. The Australian dollar is building on yesterday’s outside up day and is set to challenge the recovery high set at the end of last month near $0.6570. It approached $0.6550 in Asia before backing off and looks to have another go at it ahead of the weekend. The Chinese yuan firmed for the second session, leaving the dollar well within the CNY7.05-CNY7.10 range that has dominated for more than a month.

Europe

German March trade figures showed a larger than expected decline in exports (-11.8%) and imports (-5.1%). The next result was a smaller trade surplus of 17.4 bln euros (vs. 20.6 bln euros in February). However, the current account surplus edged higher (24.4 bln euros from 23.7 bln).

Turkey tried intervening in the foreign exchange. It failed miserably, and the lira sank to new record lows and making it more costly to service the $168 bln of debt coming due over the next 12 months. In a form of capital control, yesterday, it barred local banks from trading with three large foreign banks (Citi, UBS, BNP). It also broadened the definition of manipulation, and the ambiguity itself may also deter some sellers. However, some of the selling pressure is coming from asset managers liquidating investments in Turkish stocks and bonds. Year-to-date, about $8 bln of such portfolio investment has been sold.

The euro approached $1.0765 yesterday before recovering to about $1.0840. It was bid to $1.0855 in Asia before slipping back to $1.0820. However, the intraday technicals suggest scope to retest the high and possibly a marginal new high. Still, the $1.0865-$1.0870, where the 20-day moving average and a retracement objective of the recent slide are found. Sterling recovered yesterday as well, but there has been no follow-through buying yet, and it is making a lower high for the sixth consecutive session. At the end of last week, it appeared to be establishing a foothold above $1.25 and probing the $1.26 area. This week, it has been struggling to remain above $1.24. The Queen will address the country tonight.

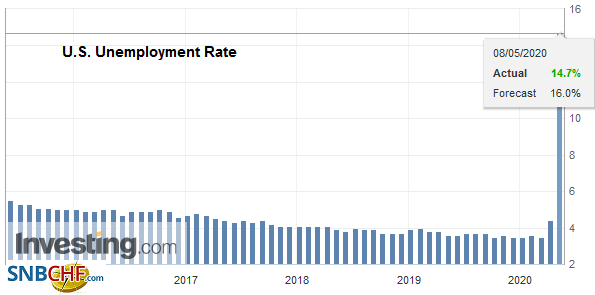

AmericaGiven the weekly jobless claims, the PMI and ISM, the ADP report, and a host of anecdotal evidence, a record loss of something around 22 mln jobs would not be surprising even if shocking. |

U.S. Unemployment Rate, April 2020 Source: investing.com - Click to enlarge |

| There is little doubt that the US is contracting sharply, and the labor market has collapsed. Nearly 33.5 mln Americans have filed initial unemployment claims over the past seven weeks. The unemployment rate itself, the result of a household survey, is expected to surge to at least 16%. |

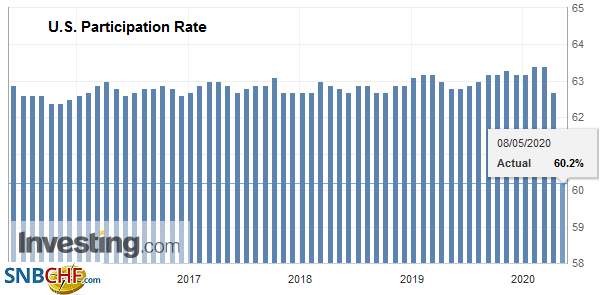

U.S. Participation Rate, April 2020(see more posts on U.S. Participation Rate, ) Source: investing.com - Click to enlarge |

| The average workweek is expected to have declined by more than half an hour. The decline in the index of hours worked also points to a sharp contraction in output. One reason that high-frequency data are important for investors is the implications for policy. However, the policy response has already been delivered. Sure, there is headline risk, but the important fact of the unprecedented economic shock is well-known and will not trigger a fresh policy response. |

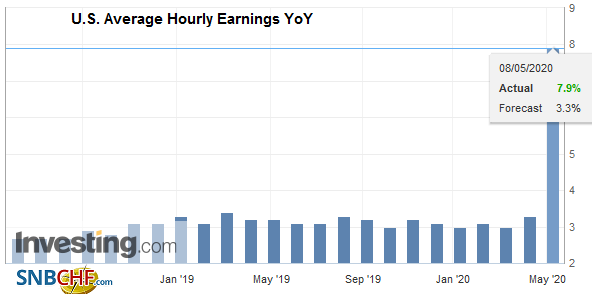

U.S. Average Hourly Earnings YoY, April 2020(see more posts on U.S. Average Hourly Earnings, ) Source: investing.com - Click to enlarge |

| The US 2-year yield fell to a record low of 12.5 bp. It is about a basis point higher now. What has really drawn attention, though, is the fact that starting with December 2020 fed funds futures contract and extending through January 2022, the implied yield is below zero. Although many Fe officials have indicated that they will do whatever it takes, nearly all have argued against negative interest rates. Richmond Fed President Barkin may have spoken for his colleagues yesterday when he said that negative rates have been tried elsewhere, and their experience gives him little reason to think that they are worth a try in the US. It would not be surprising if other Fed officials in the coming days also underscore the negative interest rates are not under consideration and provide some color of the disruption that could ensue. |

United States 2-Year Bond Yield Source: investing.com - Click to enlarge |

Canada reports its April employment data as well. Canada’s labor market is deteriorating faster than in the US. Although Canada is roughly one-tenth the size of the US, it lost a million jobs in March while the US lost 700k. The median in the Bloomberg survey was a loss of four million jobs in April. The average of the large Canadian banks that participated in the survey is closer to 4.2 mln. Canada’s unemployment rate finished last year at 5.6%. In March, it rose to 7.8%, and in April is expected to rise to 18%. We suspect the general risk appetite (S&P 500 proxy) and commodity prices (oil proxy) will point to the near-term direction of the Canadian dollar rather than the jobs data per see.

The US traded on both sides of Wednesday’s range against the Canadian dollar yesterday and settled below its low. The outside down day is seen as bearish price action, and follow-through dollar selling has pushed the greenback to about CAD1.3925 today, a new low for the week. For the past month, the US dollar has chopped in a range of roughly CAD1.3850 to CAD1.4260. A move back above CAD1.40 would help stabilize the US dollar’s technical tone. The US dollar is near the low for the week against the Mexican peso, which is found near MXN23.7850. The peso is the strongest of the emerging market currencies this week, with a gain of around 2.6% (with the US dollar near MXN23.95). The record worker remittances reported earlier this week, and the appetite for risk illustrated by the rally in equities, coupled with higher oil prices, helped fuel the peso’s recovery. It may be the first time since February that the peso will appreciate for two consecutive weeks.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,Canada,China,Currency Movement,EUR/CHF,Japan Household Spending,jobs,negative rates,newsletter,Turkey,U.S. Average Hourly Earnings,U.S. Nonfarm Payrolls,U.S. Participation Rate,U.S. Unemployment Rate,USD/CHF