Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

Swiss FrancThe Euro has fallen by 0.22% to 1.0951 |

EUR/CHF and USD/CHF, May 18(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: In Asia, equities markets rallied strongly, led by the more than 5% gain in Taiwan, the most in over a year as Monday’s 3% drop was more than overcome. The Nikkei gained more than 2% despite the deeper than expected contraction in Q1 GDP. Hong Kong, South Korea, and India also rose more than a 1% gain as tech came roaring back. In Europe, where equities have edged higher, the focus seemed to shift to the foreign exchange market, and the dollar was sold off, with the euro climbing above $1.22 and sterling pushing above $1.42. Only the Canadian dollar, Swedish krona, and Japanese yen rose less than 0.3%. Emerging market currencies, led by eastern and central Europe, are broadly higher, and the JP Morgan Emerging Market Index is up for the fourth consecutive session. The Turkish lira, a notable exception, is sporting a softer profile. US yields continue to deny the greenback much support. The 10-year benchmark is hovering around 1.65%, little changed on the day, while European yields are slightly softer. Gold traded at four-month highs today over $1870 and is consolidating in the European morning. Oil prices are also higher, with Brent testing $70 and July WTI probing $67. |

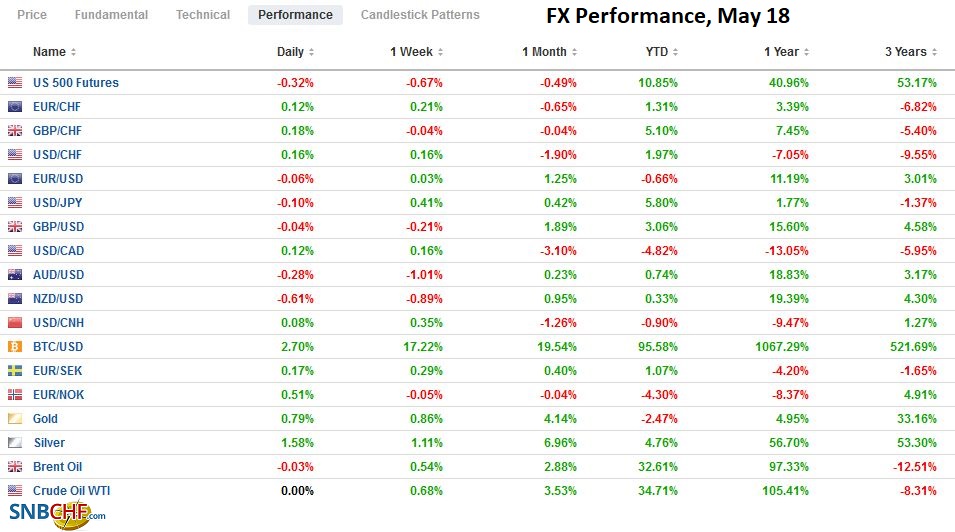

FX Performance, May 18 - Click to enlarge |

Asia Pacific

Japan’s economy contracted by 1.3% in Q1 quarter-over-quarter, which is a somewhat larger contraction than economists anticipated. As the recent retail sales report hinted, consumption held up better than feared, falling 1.4% instead of -1.9%. However, the big miss was on business spending. It was expected to rise by 0.8% and instead fell by 1.4%. The deflator was -0.2%, which was also deeper than expected. Inventory accumulation was a little stronger than expected. Net exports shaved 0.2% off GDP, in line with expectations, and a good reminder that Japan is not an export-driven economy. Net exports contributed an average of 0.1% to growth over the last four quarters and the last 20. With the third state of emergency covering 40% of the economy set to continue through the end of the month, the current quarter is challenging.

The minutes from the Reserve Bank of Australia’s meeting failed to shed fresh light on the policy outlook. Upcoming economic data and financial market developments are the keys to the next policy decision of whether to roll over the yield curve control target of the next three-year bond and extend QE. The RBA meets on June 1, but the officials have already pointed to the July 6 meeting as the timing of its decision. Meanwhile, the trade agreement with the UK, hoped to be concluded by the G7 meeting next month, is reportedly running into a debate in London over Australia’s agriculture imports.

The dollar is trading lower against the yen for the fourth consecutive session. It is testing the 20-day moving average near JPY108.85, after peaking in response to the jump in US rates after last week’s CPI report, around JPY109.80. Trendline support off the April and early May low comes in around JPY108.70 today, and a break signals a test on the recent lows by JPY108.35. The Australian dollar traded at a four-day high of almost $0.7815 after $0.7750 held, which is where a A$1 bln option is struck that expires today. Initial support now is around $0.7680, and the next upside target is the high from the middle of last week, just shy of $0.7850. Chinese officials may not like it, but the yuan is back to almost last week’s highs, which had seemed to elicit a signal from officials to go slowly. The dollar dipped below CNY6.42 for the first time since the low for the year was set on May 10 near CNY6.41. The PBOC’s dollar fix at CNY6.4357 was a bit more than average away from the median bank model forecast in Bloomberg’s survey (CNY6.4369). However, officials cannot lean too hard against the broad pressure for fear of not only antagonizing the US but also potentially spurring discontent among foreign portfolio managers who anticipate yuan gains in their investment in Chinese bonds, where premium over US Treasuries remains below 150 bp after having begun the year around 220 bp.

Europe

The UK data showed that after a poor January and February, the British economy’s rebound began in earnest in March. Today’s employment data provide more evidence of that pattern. The claimant count fell by 15.1k in April, and March’s increase of 10.1k was revised to show a decline of 19.4k. Employment rose by 84k in March (three months over three months), well above the median forecast in Bloomberg’s survey for a 50k increase and February’s 73k drop. April’s CPI will be reported tomorrow, and the base effect is expected to drive the year-over-year rate higher. The BOE, except for the outgoing chief economist, has argued, like the Fed and ECB officials, that the rise in price pressures is most likely to prove temporary.

The eurozone’s March trade surplus of 13 bln euros was a third smaller than expected, but this was offset by the upward revision of the February surplus to 23.1 bln euros from 18.4 bln. This left Q1 GDP unchanged at -0.6% from the preliminary estimate. Separately, the German constitutional court rejected an attempt to re-visit last year’s decision that did not block the Bundesbank’s participation in the ECB bond-buying program. Last year, it required that the German parliament and central bank review the impact of the bond purchases.

The euro stalled around $1.2180 last week, backed off to almost $1.2050. From there, it had a running start at $1.2200, which it has pushed above in the European morning to reach nearly $1.2225 today. This was its best level since late February, when it traded to almost $1.2245. Above there, little resistance is seen ahead of the year’s high set in early January, near $1.2350. The note of caution for North American traders is that the euro is above its upper Bollinger Band (two standard deviations above the 20-day moving average). The intraday momentum indicators are over-extended. Initial support is now seeing in the $1.2180-$1.2200 area. Sterling has poked above $1.42 for the first time since it recorded three-year highs in late February around $1.4235, which is the next immediate target. It, too, has pushed through the upper Bollinger Band (~$1.4205), and intraday momentum studies are stretched. Rather than chase it higher, look for a pullback toward $1.4170.

America

The three-month dollar LIBOR was fixed at a record low of a little less than 15 bp yesterday, and the downside pressure does not appear exhausted. The driving force is the reduction of T-bills, which force participants to other short-term instruments, including commercial paper. The abundance of short-term funds looking for a home also explains the heavy use of the Fed reverse repo facility. The T-bill paydown is a function of two chief considerations. First, parts of the stimulus were funded initially with T-bills and now is being rolled out. Second, and arguably more important, the Treasury is reducing its cash position ahead of the end of the debt ceiling waiver. When will the Fed raise the rate of interest on reserves (pays on all reserves, not just excess) or the rate on the reverse repos? In the past, the Fed has acted when the Fed funds slip to five basis points above the floor, in this case, zero. Fed funds began the year around 9 bp and fell to 8 basis points around mid-February, but by the end of the month, it was trading at 7 bp. Since late April, the effective average has been six basis points.

As there is a shortage of bills, there may be a shortage of 10-year TIPS. This shortage relative to demand is one of the distortions of the break-evens. More than that, the shortage facilitates a vicious cycle. The shortage drives prices higher and breakevens wider, and the wider breakevens, in turn, fuel more concern about inflation and increases the demand for TIPS. On Thursday, US Treasury will sell $13 bln 10-year TIPS. Tomorrow, Treasury sells $27 bln 20-year bonds. It is the 20-year bond that seems to be more volatile of the longer-term yields for more than a month and the most challenging auctions. The head of the Fed’s System Open Market Account, Logan, had suggested in early April that the Fed could adjust its purchases to reflect issuance in the coming months. In this context, the market thought it meant more buying of the 20-year, but it has not materialized, and the market grows impatient.

The US reports April housing starts and permits today. The expected small decline is hardly a sense of weakness or loss of economic momentum. Activity is still around its best level since 2006. That is the takeaway: the US housing market is strong and residential investment remains robust. We note that yesterday’s March TIC data showed foreign investors bought a record amount of long-term US securities (~$262 bln), though, given the shape of the curve and relative rates, the cost of hedging out the dollar’s currency risk is sufficiently low as to mean that the demand for long-term US assets is not equivalent to the demand for dollars. Only the Fed’s Kaplan is scheduled to speak today among Fed officials, while Treasury Secretary Yellen addresses the Chamber of Commerce. Canada and Mexico have light economic calendars today.

The US dollar drew closer to key support near CAD1.20 today to set a new six-year low (~CAD1.2015). The lower Bollinger Band is close to CAD1.1960. Initial resistance is seen in the CAD1.2030-CAD1.2040 area. Since the Bank of Canada announced its tapering and brought forward to H2 22, when the economic slack would be absorbed on April 21, the US dollar has fallen by about 5% against the Canadian dollar. The dollar has edged lower against the Mexican peso, and near MXN19.72 is at its lowest level since the second half of January. The year’s low was recorded then by MXN19.55, which is the next important target. Initial resistance is seen by MXN19.80.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,Currency Movement,EUR/CHF,Featured,federal-reserve,Japan,newsletter,RBA,T-Bills,U.K.,USD/CHF