Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

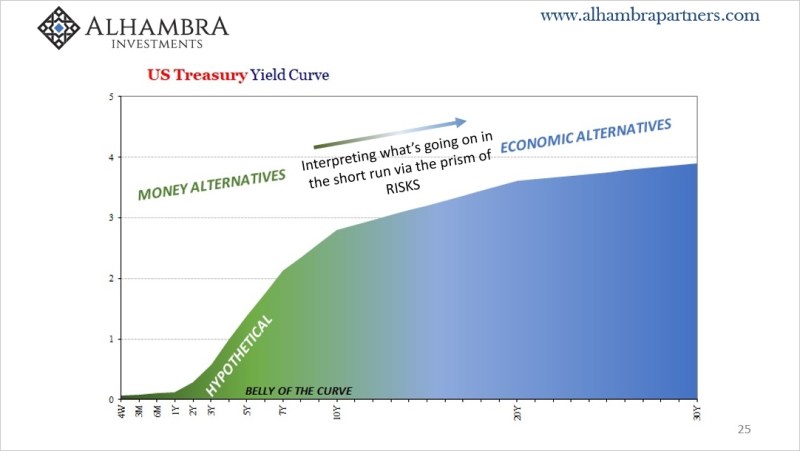

Ahead of the Week’s Central Bank Meetings, Risk Appetites Stoked

Ahead of the Week’s Central Bank Meetings, Risk Appetites Stoked12 Jun 2023

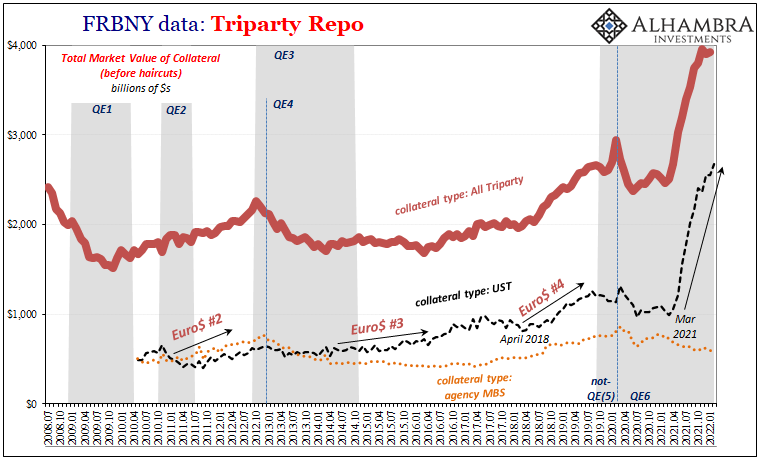

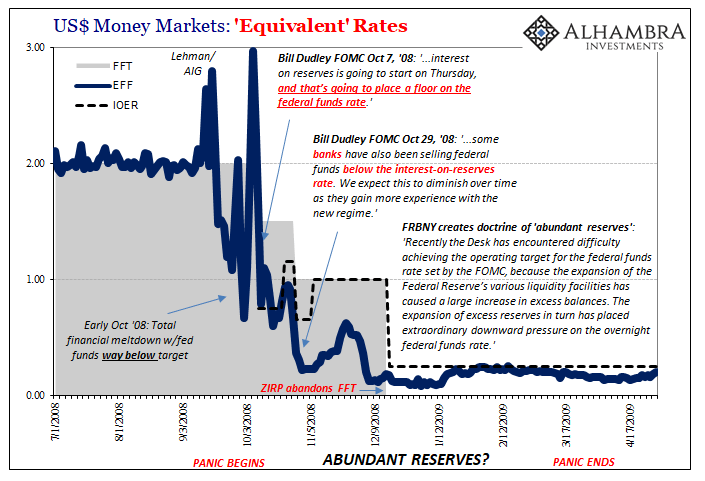

The Biggest Risk, No Surprise, Collateral28 Jun 2022

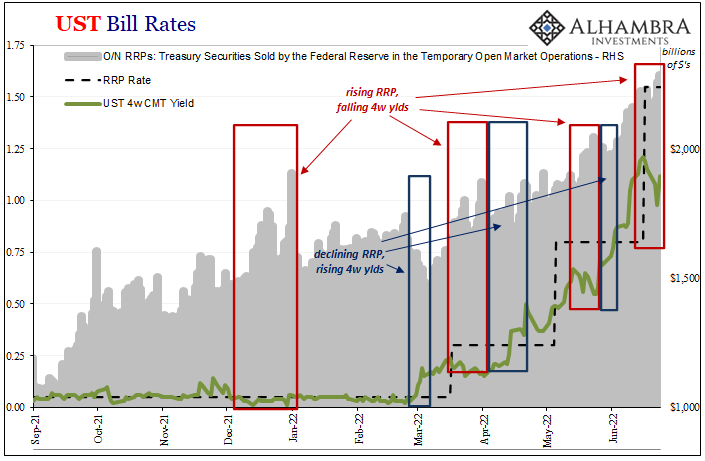

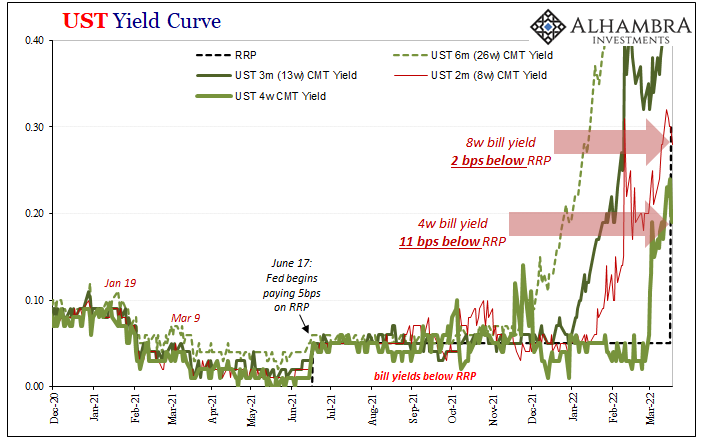

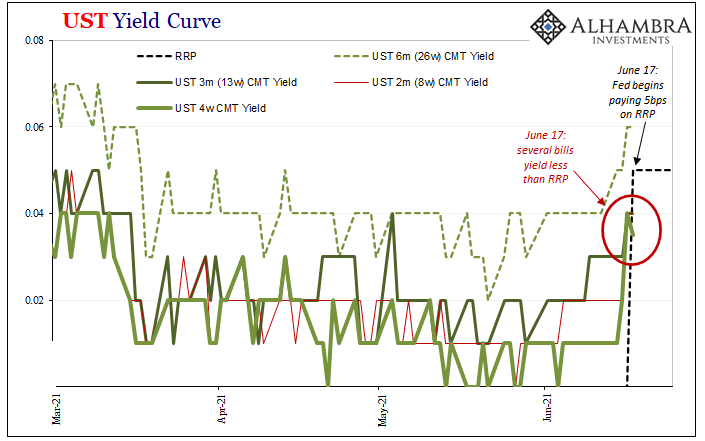

T-bills Targeted Target

T-bills Targeted Target20 May 2022

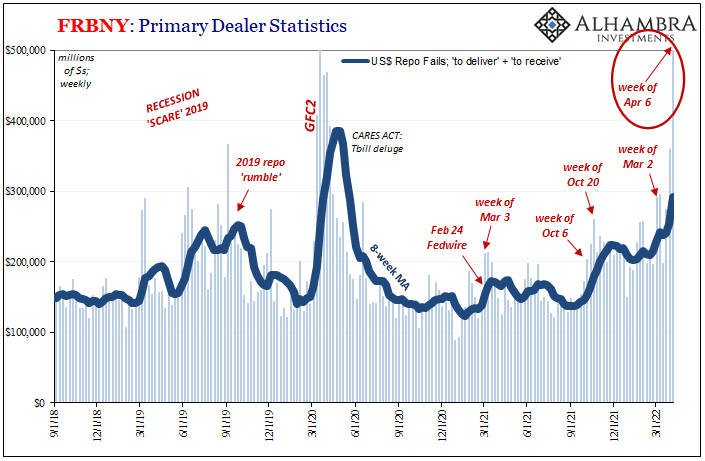

Collateral Shortage…From *A* Fed Perspective7 May 2022

What Really ‘Raises’ The Rising ‘Dollar’3 May 2022

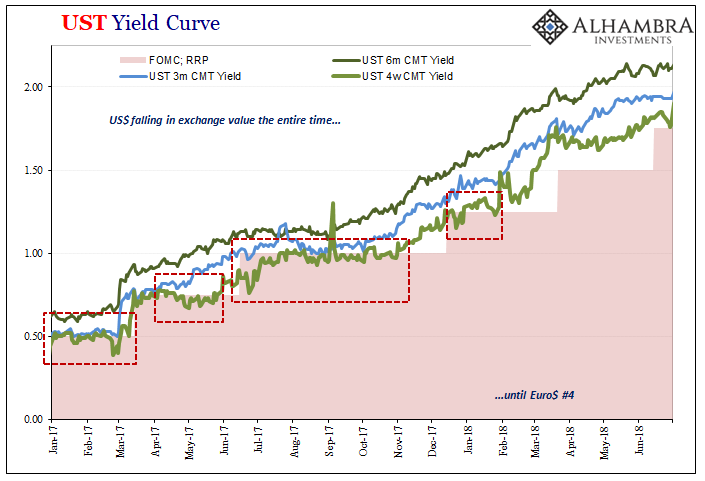

Yield Curve Inversion Was/Is Absolutely All About Collateral18 Apr 2022

The Fed Inadvertently Adds To Our Ironclad Collateral Case Which Does Seem To Have Already Included A ‘Collateral Day’ (or days)21 Mar 2022

There Is An Absolutely Solid Collateral Case For What’s Driving Curve Inversion(s) [Part 2]18 Mar 2022

Playing Dominoes19 Dec 2021

Bill Issuance Has Absolutely Surged, So Why *Haven’t* Yields, Reflation, And Other Good Things?2 Nov 2021

Short Run TIPS, LT Flat, Basically Awful Real(ity)28 Oct 2021

The Curve Is Missing Something Big21 Oct 2021

CPI’s At Fives Yet Treasury Auctions12 Aug 2021

Golden Collateral Checking27 Jul 2021

Lower Yields And (fewer) Bills21 Jul 2021

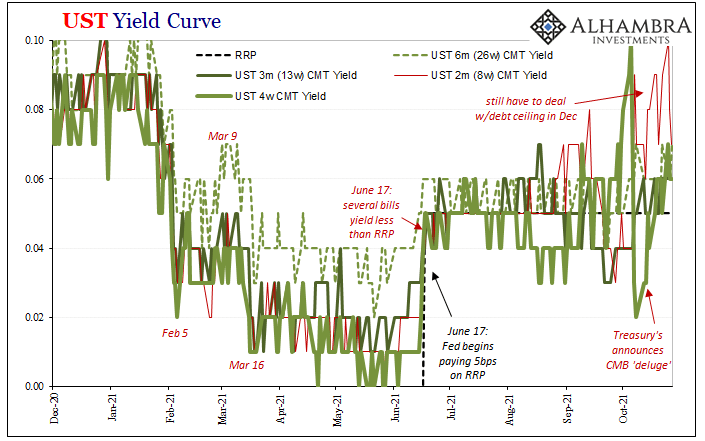

The FOMC Accidentally Exposes Itself (Reverse Repo-style)18 Jun 2021

FX Daily, May 18: Risk Appetites Return Bigly18 May 2021

What Might Be In *Another* Market-based Yield Curve Twist?23 Feb 2021

Two Seemingly Opposite Ends Of The Inflation Debate Come Together19 Feb 2021

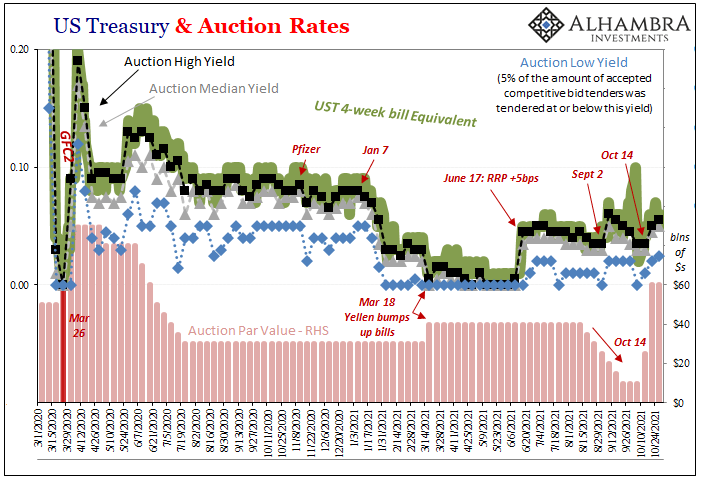

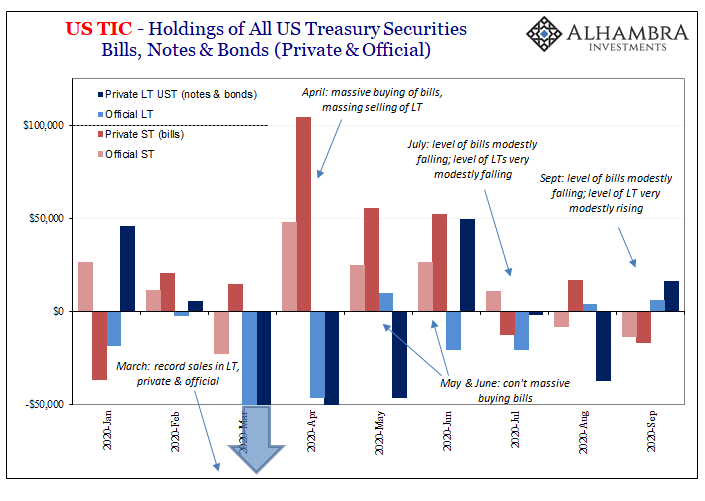

Just Who Is, And Who Is Not, Selling T-Bills29 Nov 2020