Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

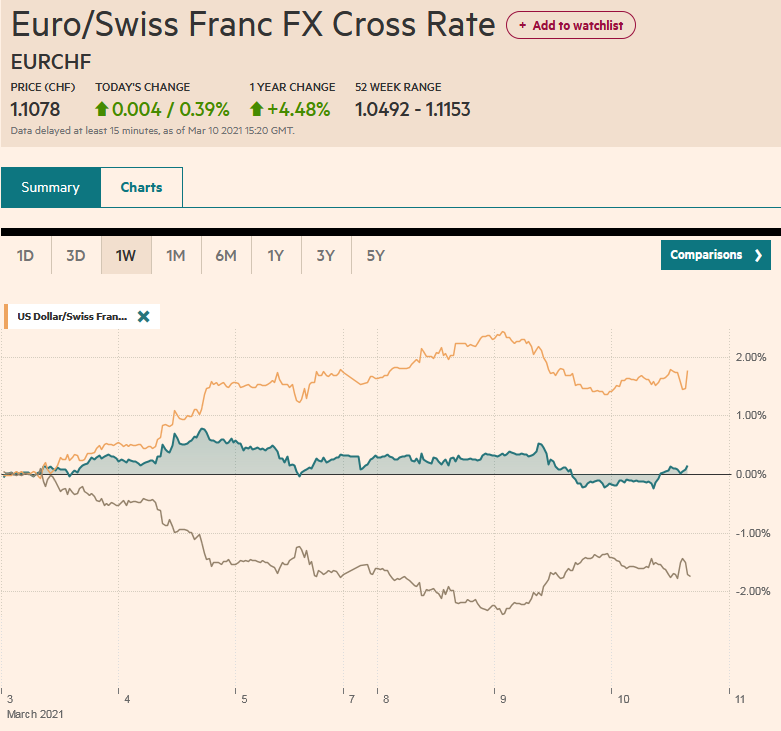

Swiss FrancThe Euro has risen by 0.39% to 1.1078 |

EUR/CHF and USD/CHF, March 10(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: Fear that yesterday’s reversals represent little more than one-day wonders is contributing to the overall consolidative tone today. Most equity markets in the Asia Pacific region and Europe edged higher. China’s stocks tumbled yesterday, despite reports of official assistance, were mixed with the Shanghai Composite posting small gain and Shenzhen a small loss. South Korea and Australia’s benchmarks slipped lower. Europe’s Dow Jones Stoxx 600 is extending its gains for a third session, while US futures indices are narrowly mixed. The US 10-year yield is a few basis points higher at 1.55%, and most European benchmark yields are slightly firmer. Australian and New Zealand bonds rallied, and yields fell around seven basis points. The US dollar is mostly a little higher against the majors and mixed against the emerging market currencies. The yen and Swiss franc are the laggards, nursing around a 0.2% loss near midday in Europe. The JP Morgan Emerging Market Currency Index rose by 0.7% yesterday, the most in two months, and has edged a little higher so far today. After rallying almost 2% yesterday, gold is consolidating in a narrow range, mostly between $1710 and $1720. April WTI initially slipped to a four-day low near $63.15 and recovered, rising to $64.35 in the European morning before the buying appears to dry-up. |

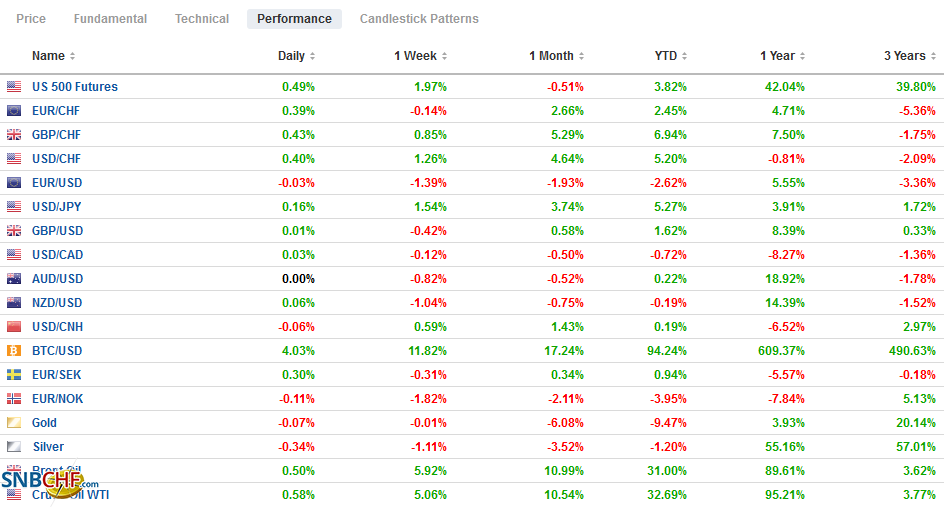

FX Performance, March 10 - Click to enlarge |

Asia PacificChina reported February inflation gauges and lending figures. Consumer price inflation remains below zero. The CPI rose to -0.2% from -0.3% and on a year-over-year basis. The 0.6% rise on the most is the least in three months. Consumer goods prices are off by 0.3% year-over-year, showing continued deterioration. However, prices of consumer services fell 0.1% after a 0.7% year-over-year plunge in January. The decline in pork prices accelerated. The fading base effect will likely allow CPI to turn positive shortly. Producers prices jumped 1.7% year-over-year after a 0.3% rise in January. Rising commodity prices and the favorable base effect were the key drivers. China’s lending figures slowed from the hectic pace in January but were stronger than expected. New yuan loans rose by CNY1.36 trillion after a CNY3.58 trillion surge in January when new lending quotas were available. Aggregate financing, which adds the shadow banking activity to traditional lending, rose by CNY1.71 trillion, nearly twice what was expected, but still a dramatic slowdown from the CNY5.17 trillion. |

China Consumer Price Index (CPI) YoY, February 2021(see more posts on China Consumer Price Index, ) Source: investing.com - Click to enlarge |

RBA Governor Lowe pushed against market expectations and appeared successful as the yield on the three-year note (targeted at 10 bp) slipped for the second day. It is the first back-to-back yield decline in more than a month, and the three-year benchmark yield eased below the target for the first time this year. Lowe warned the market was getting ahead of itself in pricing in a rate hike. He continued to signal that rates were unlikely to rise until at least 2024. Lowe dismissed the increase in inflation expectations priced in as not exceptionally high or above the central bank’s target. He reiterated the evolution of its forward guidance, which emphasizes actual inflation over inflation forecasts, and continued to pin the outlook on wage growth. Wage growth, he says, needs to be above 3% or more than double the current record low of 1.4%.

The dollar is consolidating within yesterday’s range against the Japanese yen and has been mostly confined to a JPY108.50-JPY18.90 range. Yesterday’s high was almost JPY109.25. The greenback had finished the North American session near its lows against the yen but was bought in early Asia. With firm US yields, it would not be surprising to see the dollar probe higher in the North American morning./European afternoon. The Australian dollar is moving sideways in the roughly one-cent range established at the end of last week (~$0.7620-$0.7730). The upper end was rejected in North America yesterday. After pulling back in early Asia Pacific turnover, it recovered, only to find more sellers in Europe above $0.7715. After falling by about 0.3% against the Chinese yuan yesterday, the dollar edged slightly higher today. The greenback has risen in four of the past five sessions and remained above CNY6.50 today. The PBOC set the dollar’s reference rate at CNY6.5106, which was a bit more than usual away from the Bloomberg bank survey that found a median of CNY6.5127.

Europe

French industrial output surged in January. The 3.3% jumped compared contrasted with a median forecast in the Bloomberg survey for a 0.5% gain. It was driven by coke and refinery and mining sector. Auto output and transportation material fell. France is the last of the big four EMU economies to report. Recall Germany’s industrial output unexpectedly fell by 2.5%, but the December gain was revised to 1.9% from zero. Italy’s 1.0% gain was a surprise in the opposite direction, and the December series was revised to show a 0.2% gain (initially a 0.2% decline). Spain’s was a little weaker than expected at -0.7%, and adding insult to injury, December’s 1.1% gain was shaved to 0.8%. The aggregate figure for the eurozone is set for release on Friday.

The ECB begins its two-day meeting, and tomorrow’s announcement will be followed by the press conference. The ECB will be updating its forecasts, and near-term growth projections will likely be shaved while this year’s inflation forecast may edge higher. The focus is not on exchange rates but yields. Officials seem to have signaled a desire to look past the near-term volatility. There is much expectation that it could increase its bond purchases, but to commit it would seem to remove an important element of flexibility. The Fed commits to buying $120 bln of long-term assets a month. The ECB does not commit to any size, and it will likely keep it this way.

The euro approached its 200-day moving average yesterday (~$1.1830) and rebounded smartly to about $1.1915. Although it finished the North American session near its highs, there has been no follow-through buying today, and the euro had found new sellers when it poked above $1.1900 in early European turnover. Initial support may be seen in the $1.1870-$1.1880 area. The market appears to see asymmetrical risk from the ECB, and short-term participants may be reluctant to be long euros ahead of Lagarde’s press conference tomorrow. Sterling is also trading within yesterday’s range and is a little changed a little below $1.3900. Initial support is found around $1.3880 and then $1.3845. The market seems content to consolidate and await fresh directional cues ahead of tomorrow’s data dump that includes January’s monthly GDP figures, where a large contraction is expected.

AmericaThere are two highlights for the US markets today aside from the formality of the House of Representatives approving the new stimulus package. First, the US reports February CPI. It is the last before the base effect surge that will extend through most of the spring. Last month, food and energy prices rose, which will lift the headline pace to around 1.7% from 1.4%. |

U.S. Consumer Price Index (CPI) YoY, February 2021(see more posts on U.S. Consumer Price Index, ) Source: investing.com - Click to enlarge |

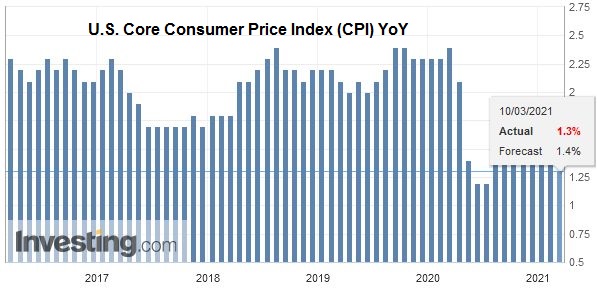

| The core rate was flat in January, and a 0.2% rise in February may keep the year-over-year rate steady around 1.4%. Barring a surprise, the market impact may be minimal, pending the second important event’s outcome. The US Treasury will sell $38 bln 10-year notes. Yesterday’s 3-year note sales was well received, with the highest bid-cover (2.69x) since mid-2018. However, the real test is with the longer-dated paper, including tomorrow’s $24 bln 30-year bonds sale. |

U.S. Core Consumer Price Index (CPI) YoY, February 2021(see more posts on U.S. Core Consumer Price Index, ) Source: investing.com - Click to enlarge |

Expectations for today’s Bank of Canada meeting are low. No policy change is expected, and the rhetoric has been rehearsed. The central bank is committed to maintaining the monetary stimulus for some time and well-beyond the immediate economic pick-up. Governor Macklem sees a role for monetary policy in helping to facilitate structural economic changes, like digitalization, which seem to be accelerated by the pandemic. The large fiscal stimulus in the US, which the OECD estimates will add three percentage points to its growth, will have a spill-over effect and likely help Canada as well. That is to say that the US stimulus should make BoC officials more confident in the economic outlook. The Bank of Canada will provide a broader assessment in April, but some expect a hint that more tapering of its bond-buying is likely in the coming months. Canada’s 10-year bond yield has more doubled since the US election and vaccine announcement to almost 1.55% before pulling back. Yet, given that underlying core inflation was at 2% in January (February’s figures will be reported on March 17), rates are not high. The 10-year yield finished 2019 closer to 1.70%.

As North American markets are set to re-open, the US dollar is trading in the middle in the session’s range against the Canadian dollar (~CAD1.2630-CAD1.2685). It is within yesterday’s range. Indeed, the greenback has hardly traded outside of the range set during the last session of February (~CAD1.2585-CAD1.2750). The intraday technical readings may favor the greenback’s upside. The Mexican peso is holding yesterday’s gains but has been unable to extend them. The US dollar fell from above MXN21.50 yesterday to flirt with the 200-day moving average around MXN21.1560. A break of yesterday’s lows signals a test on the MXN21.00 area. Initial resistance may be near MXN21.30.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,Bank of Canada,China,Currency Movement,ECB,Featured,newsletter,RBA