Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

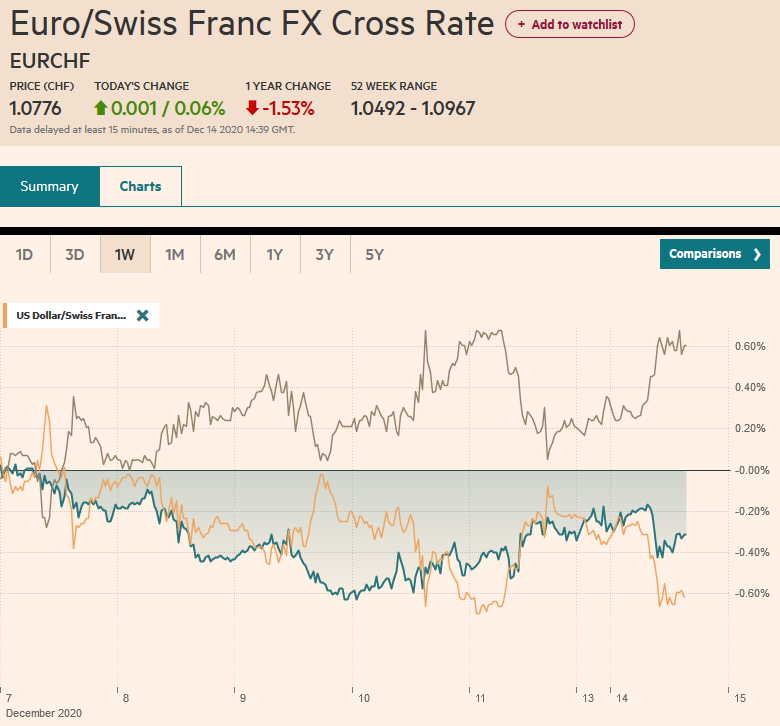

Swiss FrancThe Euro has risen by 0.06% to 1.0776 |

EUR/CHF and USD/CHF, December 14(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The fact that the UK and EU negotiators are still talking is seen as a constructive development and has spurred a sharp bounce in sterling. It traded below $1.3150 before the weekend and is pushing above $1.3400 in the European morning. It is part of the larger risk-on move lifting equities and weighing on the dollar more broadly. Equities in the Asia Pacific region were mixed, but Japan, China, India, and Australia rose. The Topix hit new two-year highs. European stocks are snapping a three-day decline by rising nearly 1% so far today. US shares are also trading with a firmer bias and the S&P 500 may gap higher. Recall that the S&P ended last week with a three-day downdraft, the longest in a couple of months. Peripheral European bond yields slipped to new lows, while core yields are a little firmer. The UK10-year Gilt yield is 6 bp higher to push back above 0.23%, while the US benchmark is firm at 0.92%. The dollar is lower against all the majors, and the Norwegian joins sterling with more than a 1% rise. The Canadian dollar and yen are laggards with 0.15%-0.25% gains. Most emerging market currencies are higher, with the Turkish lira and a few East Asian currencies notable exceptions. Gold is trapped in its recent trough that extends to around $1820 and the 200-day moving average near $1810. Oil is firm, with Brent trying to solidify its hold above $50 while January WTI is firm above $47 (last week’s high was around $47.75). |

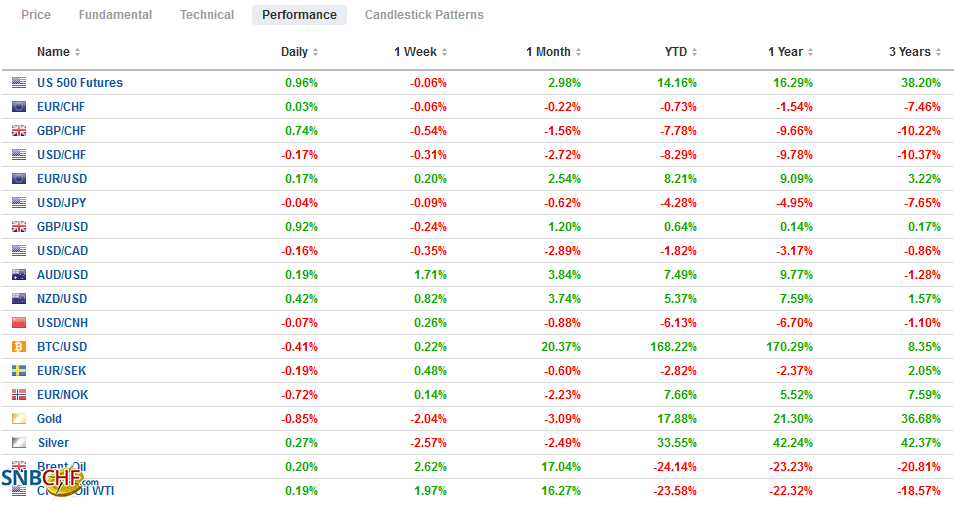

FX Performance, December 14 - Click to enlarge |

Asia PacificThe record trade surplus China reported last week means that efforts to contain China on trade have been unsuccessful. Yet, trade is one dimension of the multi-dimensional strategic rivalry that has some parallels with the Cold War. Capital is another dimension. China capital controls and limits on foreign investment, even if they are relaxing on the margins. However, they are part of the status quo ante. What is new are the US measures. By sanctioning a number of Chinese companies for ties to the Chinese military, it put the index providers in a difficult position. FTSE Russell and S&P Dow Jones Indices have dropped 8-10 Chinese companies cited by the US Department of Defense from their benchmarks. These steps were across the different ways investors can invest in China (mainland A-shares, H-shares in Hong Kong, GDR/ADRs. S&P Dow Jones will also be removing the respective corporate bonds from its indices before the start of the New Year. At the same time, President Trump is expected to sign the bill that has now passed both chambers that seek to de-list Chinese companies who refuse to allow US authorities to review their audits. |

China House Prices YoY, November 2020(see more posts on China House Prices, ) Source: investing.com - Click to enlarge |

Japan’s quarterly Tankan survey showed more improvement than expected, but the pessimism has not been shaken, and the outlook remains poor. The large manufacturer sentiment reading rose to -10 from -27, which is better than expected, but the outlook (-8) shows the pessimists outnumber the optimists. Large non-manufacturer sentiment rose to -5 from -12, and the outlook is for -6. The same pattern is repeated for smaller companies. Also disappointing was the decline in capex plans for large businesses (-1.2% vs. +1.4%). The dollar forecast was lowered to JPY106.70 from JPY107.11 and warns that Japanese companies may not be positioned for the yen strength. The dollar has averaged about JPY104.65 over the past 50 days and JPY105.20 over the past 100 sessions. Separately, Japan revised up October industrial output increase to 4.0% (month-over-month) from 3.8% initially and 3.9% in September. The tertiary industry index rose 1.0% in October, a little less than anticipated, while the September series was revised to 2.3% from 1.8%. The BOJ meets later this week and is expected to extend its emergency lending facilities.

The impact of these measures on slowing China’s integration in the global capital market is marginal at best. It may redirect investments to other Chinese companies. It could prompt Chinese companies to seek listing elsewhere, perhaps, on less transparent and less investor-friendly exchanges, and/or boost the rise of other financial centers that compete with the American exchanges. Like the tariffs imposed by President Trump, these measures are unlikely to be overturned quickly by the Biden administration. As we have noted, these post-election actions by Trump do achieve two things. First, they limit Biden’s options if not wanting to appear weak. Second, they give Biden additional chits that can be used in negotiations with Beijing.

The dollar has eased to the lower end of its recent range against the yen that extends to about JPY103.65. There is an option for around $610 mln at JPY103.55 that expires today. The intraday technicals are stretched in the European morning. Immediate resistance is seen in the JPY103.85-JPY103.95, with an expiring option for nearly $560 mln at JPY104.00. The Australian dollar made a marginal new high just below $0.7575. The high for the day does not appear in place yet. The next upside target is in the $0.7600-$0.7625 area. The PBOC set the dollar’s reference rate at CNY6.5361, a little weaker than expected. In money market operations, the PBOC drained about CNY30 bln (short-term reverse repos) but is expected to provide at least CNY300 bln tomorrow via its medium-term lending facility. Separately, note that the forex position on the PBOC balance sheet rose CNY5.93 bln in November to CNY21.2 bln, confirming little direct intervention.

Europe

During the Greek sovereign debt crisis a decade ago, Europe showed a remarkably disciplined and united stance. The same is true during the Brexit negotiations. European capitals recognize that this is not a one-off iteration but a game to be repeated endlessly. The UK is part of the western peninsula of the great Eurasian landmass. Its past and future are tied to it. Even if no deal is struck now, many may be surprised how soon talks resume in the New Year.

A little optimism has crept into the market compared with the pessimism that held sway at the end of last week. The fact that a new deadline for the talks has not been set was seen as a constructive development, and there is some speculation that talks could continue into next week. There does seem to be some softening of positions. The EU chief negotiator Barnier reportedly has briefed EU representatives and sketched out a couple of scenarios. The most optimistic was that a deal could be struck this week, while talks could run right up to the December 31 deadline, which appears to be the only deadline that matters.

There is a hope that the US election of Biden will restore US-EU relations. While a return to civility is likely, several key issues are pulling them apart that are unlikely to be resolved quickly. One of them is the Nord Stream 2 pipeline that would pump Russian gas directly to Germany, bypassing Ukraine. US sanctions forced a Swiss pipelaying company to pull out last year. However, a couple of Russian ships in the past week appear to be trying to finish the construction. The US action has deterred the most capable companies and ships, but the project is nearly completed. A small section near Germany and a somewhat larger section near Denmark is left.

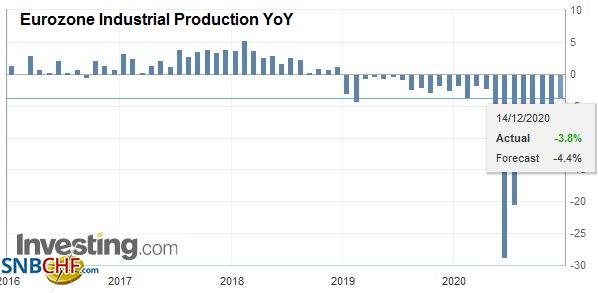

| Eurozone industrial output rose 2.1% in October, and the September series was revised to show a 0.1% gain instead of a 0.4% decline, as initially reported. All four of the largest members had reported stronger national figures. German output jumped 3.2%, twice what economists had forecast. French industrial production rose by 1.6%. Economists had forecast a 0.4% gain. Italy’s industrial output for 1.3%, compared to the forecast of 1.0%, while Spain’s increased by 0.6% while a flat report had been anticipated. The preliminary December PMI report is due Wednesday, and a rise in services is expected to lift the composite, which will likely remain below the 50 boom/bust level. |

Eurozone Industrial Production YoY, October 2020(see more posts on Eurozone Industrial Production, ) Source: investing.com - Click to enlarge |

The euro is firm near $1.2150 but remains within last Friday’s trading range (~$1.2105-$1.2165). After the disappointing US jobs data, the 2.5-year high set earlier this month was just shy of $1.2180. There is an expiring option for 860 mln euro at $1.2175 today. If the session high has not been recorded yet, the euro came pretty close, we suspect. A break of $1.2140 keeps the consolidative tone intact and suggests a retest on the $1.21-area. Sterling is having one of its best days in a couple of months, rising about 1.4% against the dollar (at about $1.3415). Last week’s high was near $1.3480, and the week before, with the help of the US employment data, it reached almost $1.3540. The euro spiked to GBP0.9230 amid pre-weekend pessimism and is now near GBP:0.9050. Last week’s lows were around GBP0.8980.

America

The US Supreme Court’s rejection of the case to overturn the election that had been endorsed by two-thirds of the Republican representatives in the House of Representatives an important step in putting the election behind us. Today marks another element of closure. The electors (of the Electoral College) will cast their votes today. Investors have looked beyond the political drama. This week’s focus is on the initial roll-out of the vaccine, Congress’s efforts to get an appropriations bill and stimulus bill by the new end of the week deadline, and the FOMC meeting. Some observers argue that the risk of more Fed action after the recent disappointing employment data (both the November national employment report and the rise in weekly jobless claims) may be keeping the bears at bay.

The bipartisan group of Senators will offer two proposals today. The first is for a $748 bln stimulus bills. The second is a compromise on state and local aid and limiting corporate liability for Covid-related issues for $160 bln. By separating the two, the hope is that by stripping the controversial parts, it boosts the chances of approval for at last the first part.

The economic calendar for North America is light today. US retail sales and industrial production figures are the data highlights this week, but the FOMC meeting is the main focus. Canada’s CPI and retail sales figures are the focus there, and Mexico’s central bank also meets this week. It is expected to wait for confirmation that inflation pressures have subsided before resuming its easing cycle. Note that the controversial bill that requires Banxico to buy dollars from banks was left off the congressional agenda today before the winter recess. The bill will likely return next year.

The US dollar is a little weaker against the Canadian dollar today but is within the pre-weekend range, which itself was inside the December 10th range (~CAD1.2707-CAD1.2830). Initial support today is seen in the CAD1.2720-CAD1.2740 band, while CAD1.2780 looks to offer initial resistance. Continued consolidation is the most likely scenario. The greenback is also consolidating against the Mexican peso. After falling to near MXN19.70 in the middle of last week, the US dollar recovered to close above MXN20.00 in the last two sessions and is mostly holding above it today. Dollar offers are thought to be in the MXN20.20-MXN20.21area. A break of MXN19.95 could be the first sign that a top is in place, which is out leaning, suspecting that it is an attractive place to park funds over the holidays.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,$CNY,Brexit,China,Currency Movement,Featured,newsletter