Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

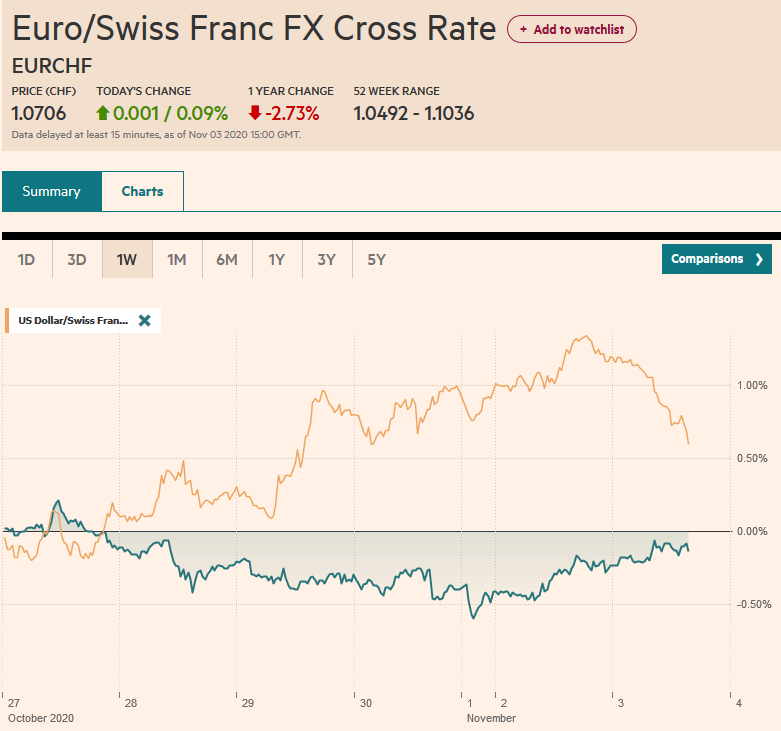

Swiss FrancThe Euro has risen by 0.09% to 1.0706 |

EUR/CHF and USD/CHF, November 3(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: More than 95 mln Americans voted before today, and many observers warn of a cliffhanger that could be decided in the courts. The polls sand surveys show strong odds in favor of a Democratic sweep. Looking at the capital markets, nothing looks amiss. The biggest rally in the S&P 500 in three weeks yesterday (1.2%) underpinned the recovery in global shares today. Although Tokyo markets were closed for a holiday, nearly every market in the Asia Pacific region rose by more than 1% as the regional benchmark rose for a second session. The Dow Jones Stoxx gapped higher today as its recovery enters the third day. The S&P is poised to gap higher at the open. Benchmark yields are mostly a little higher in Europe. Italy and Greece are faring better. The US, UK, and Swedish 10-year yields are 3-4 bp higher, while Australia’s 10-year yield is off five basis points following the RBA’s easing. The US dollar is heavier against the major currencies, even the Australian dollar. The euro looks to snap its six-day slide, as does the JP Morgan Emerging Market Currency Index. The Turkish lira remains under pressure despite its slightly less than expected rise in CPI. Gold is hovering around $1900, while oil is extending yesterday’s dramatic recovery. The December WTI contract posted a key outside reversal yesterday by falling to new lows (~$33.65) before rebounding over $37. It is trading above $38 now amid talk that OPEC+ will delay the planned output increase. |

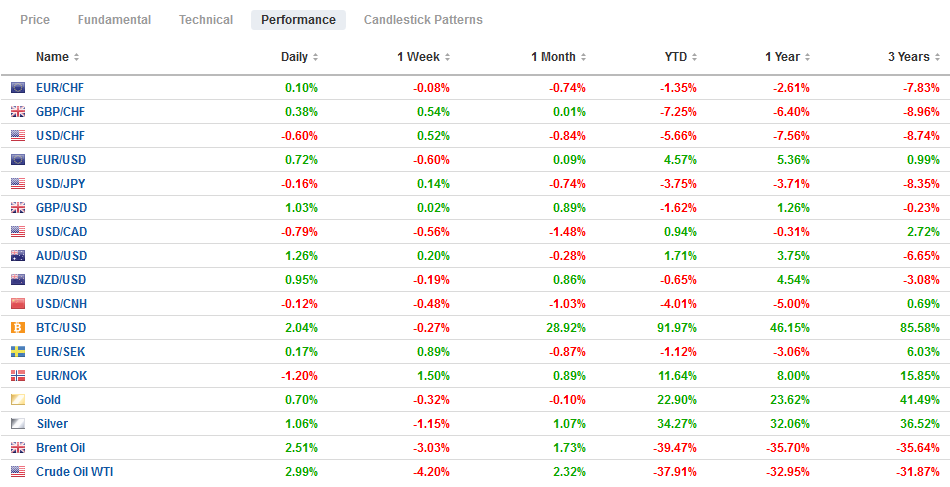

FX Performance, November 3 - Click to enlarge |

Asia PacificThe Reserve Bank of Australia did not surprise. It cut the cash and three-year target rates to 10 bp from 25 bp and announced an A$100 bln, the six-month bond-buying operation that will focus on the longer-end of the survey (5-10 years). The RBA’s central scenario now sees the economy expanding by 6% in the year to mid-2021 and 4% in 2022. Unemployment is now expected to peak a little below 8% rather than 10% as it previously feared. Underlying inflation is expected to be around 1% in 2021 and 1.5% in 2022. The RBA’s moves appear aimed at strengthening the recovery rather than improve market functioning or boosting inflation. It also appears to assume that other countries will ease as well. |

China Caixin Manufacturing Purchasing Managers Index (PMI), October 2020(see more posts on China Caixin Manufacturing PMI, ) Source: investing.com - Click to enlarge |

| Countries seeking to impose their will on others will use what levers that have. The US has used access to the dollar and to its technology to punish countries for policies for which it does not approve. China does a similar thing with the levers it has. It has used access to its domestic market to punish others for actions that go counter to its interests. Canada has felt its wrath, and now Beijing has turned its attention to Australia. Canberra has been vocally critical of China’s actions in Hong Kong, but more importantly, it has solidified its role in an emerging regional effort to counter China’s influence. China has banned timber from Queensland, identified a second barley producer it will ban. Rock lobster shipments have been subject to new inspections that seem part of Beijing’s campaign, which looks set to escalate to include sugar, copper ore, and copper concentrate. Australian wine and wheat are also in China’s cross-hairs, and a formal announcement is expected soon. |

Japan Manufacturing Purchasing Managers Index (PMI), October 2020(see more posts on Japan Manufacturing Purchasing Managers Index, ) Source: investing.com - Click to enlarge |

The US dollar trended gently lower against the yen after reaching six-day highs yesterday just shy of JPY105.00, where a $425 mln option expires today. Late in the Asian session today, the dollar dipped briefly below JPY104.50 but rebounded in Europe to almost JPY104.75 before encountering sellers again. The Australian dollar is extending yesterday’s recovery from the dip below $0.7000 (for the first time since July). It closed firmly yesterday at new session highs above $0.705,0 and today punched through $0.7130 in Europe before stalling. The downtrend line drawn off the September and October highs is a little above $0.7135 today. The PBOC set the dollar’s reference rate at CNY6.6957, which was stronger than expected. The yuan is firmer for the fourth consecutive session, and the dollar is at its lowest level (~CNY6.6810) since October 21. The month-end money market tightness is unwinding with the help of steady new cash injections by the PBOC. Officials will likely more offset the CNY400 bln maturing of a one-year medium-term lending facility loan on Thursday.

Europe

ECB data showed that the Eurosystem purchased of bonds in the last week of October fell to 11 bln euros, the least since the PEPP was introduced. It does not seem that favorable market conditions explain the tepid activity. Yet, it did reinvest about 37 bln of maturing proceeds. Separately, last month, the ECB’s corporate bond-buying seems fairly strong (second-most on record), even though the purchases in the primary market appear to have been limited by the smaller issuance.

The Bank of England meets on November 5, the same day that the partial lockdown starts. It seems less strict than in many other European centers and more lax than the UK’s previous one. A YouGov poll found that Prime Minister Johnson’s plan is supported by nearly 75%. The measures will be put to a vote in the Parliament tomorrow. The plan calls to revert back to the regional authority after December 2. Germany’s Merkel will hold a news conference shortly and the new social restrictions. Berlin is linking the lifting of the social restrictions to reduce the seven-day incidence rate to below 50 per 100k and effective tracking, which has broken down (it is around 114.6 for 100k now, according to reports).

The euro is poised to end a six-day slide that brought it about $1.1625 from $1.1880. It has bounced to almost $1.1700 today in Europe. The $1.1720 area roughly corresponds to the (38.2%) retracement of the decline, and a 585 mln euro option struck at $1.1725 rolls off today. Sterling fell to almost a one-month low near $1.2855 yesterday before recovering somewhat in North America. It is extending its recovery today to reach almost $1.30 in Europe on the back of the broadly heavier dollar tone. The $1.2980 area corresponds to the (38.2%) retracement objective of the last leg down, while $1.3015 is the (50%) retracement. Turkey’s headline include rose to 11.89% in October (year-over-year) from 11.75%. Economists expected it to come in slightly higher but below 12%. The core rate edged up to 11.48% from 11.32% and again was not as high as expected. Still, the lira drew little succor from it, and the dollar rose to a new record high (~TRY8.4870). Over the past month, the lira is off 8.3%, bringing the year-to-date loss to almost 30%.

America

As the US goes to the polls, investors will see September factory orders amid a string of economic reports that have mostly better than expected. Arguably, except for trade and inventory data, September reports have largely lost their oomph after Q3 GDP has been reported. October auto sales offer new information. The monthly average is 13.88 mln vehicles (saar) compared with 16.96 mln average for the same year-ago period through September. It puts the gap at18.2%, while in June, the year-to-date average was a little more than 17% lower than the H1 19.

While the partisans emphasize the difference between the two candidates and parties, our dollar outlook is influenced by the similarities. Specifically, we expect the dollar’s downtrend to continue exchange rates bear the burden of adjustment that will be increasing framed around the twin deficits. By definition, the balance of payments is balanced, and there are many equilibriums that can be achieved. Still, without higher rates or higher expected rates of return, a weaker dollar will be necessary. Regardless of today’s election results, we expect the US confrontation with China will continue. US frustration with Europe over the Nord Stream II pipeline, its NATO contributions, and its large trade surplus will persist. One area of difference is that the Democratic Party has been more critical of the UK’s decision to leave the EU than the Trump Administration.

US-Canadian relations would likely improve in a Biden government. The US dollar posted an outside down day against the Canadian dollar yesterday, and there is follow-through selling today. The greenback reached CAD1.3370 yesterday before reversing lower and settling on its lows (~CAD1.3215). It was sold a little through CAD1.3140 in Europe today. The CAD1.3100 area is the next target, which corresponds to the trendline drawn off the early September and late October lows. The Mexican peso is also bid today. Recall that last week, the greenback rose for the first time in five weeks and for only the third time since the end of July. It ran into a wall of offers near MXN21.50, repeatedly tested in recent days. It has been sold to about MXN21.02 today. Last month’s low was about MXN20.8320, and the September low was around MXN20.8450. Initial resistance in North America may be found in the MXN21.12-MXN21.15 area.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,Australia,COVID-19,Currency Movement,Featured,newsletter,Politics,Turkey