Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

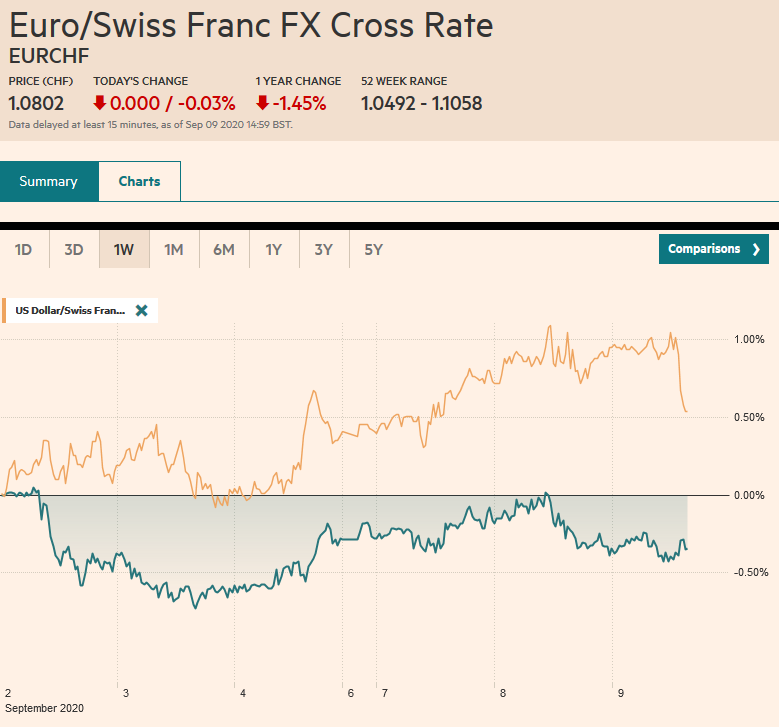

Swiss FrancThe Euro has fallen by 0.03% to 1.0802 |

EUR/CHF and USD/CHF, September 9(see more posts on EUR/CHF, USD/CHF, ) Source: investing.com - Click to enlarge |

FX RatesOverview: News that the AstraZeneca Phase 3 test had to be stopped to study the adverse reaction of one subject added to the uncertainty of investors amid one of the more significant reversals of risk appetites since March. Equities continued to slump in the Asia Pacific region, with many large markets off more than 1%, led by Australia’s more than 2% decline. However, European equities are moving higher, and the Dow Jones Stoxx 600 is up about 0.8% in late morning turnover that that seen nearly all the main industry groups advance. Energy, consumer staples, and communication service sectors are the strongest. US shares are firmer, and the early call is for the S&P 500 to open around 0.6% higher. Benchmark 10-year yields are mostly lower, with the US near 68 bp. The greenback is mixed. The dollar-bloc currencies are posting small gains, while sterling is the weakest, holding below $1.30 today. Emerging market currencies are mostly weaker, though the South African rand is recovering from yesterday’s disappointing-GDP induced slide and the Russian ruble is also a little stronger. Gold held above $1900 in yesterday’s slump but is consolidating today in nearly a $5 range on either side of $1930. Oil prices are also tentatively stabilizing after a four-day slide that took the October WTI contract from almost $43 to near $36. |

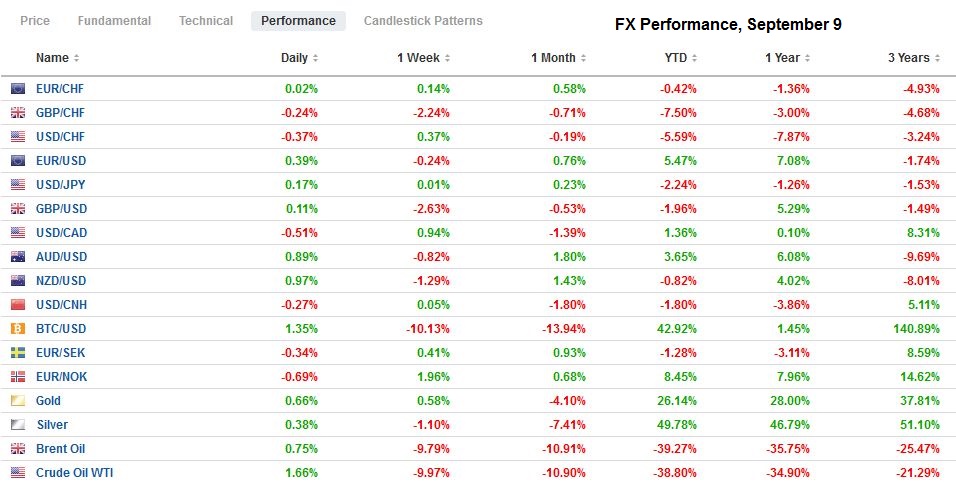

FX Performance, September 9 - Click to enlarge |

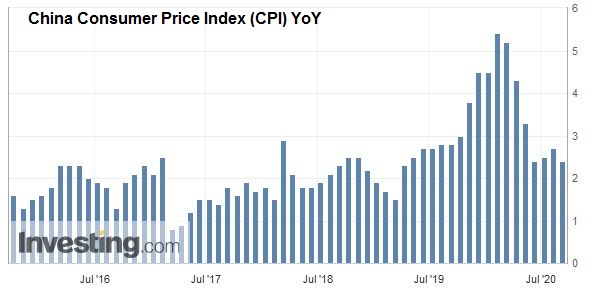

Asia PacificChina’s inflation challenge has been primarily about food prices, and these have begun easing. Headline August CPI eased to 2.4% from 2.7% in July. Pork prices slowed to 53% year-over-year, which is the smallest increase in a year. Overall, food price inflation slowed to 11.2%. Non-food prices rose a mere 0.1%. Core prices, excluding food and energy, rose 0.5% in August year-over-year, the same as in July. Further moderation in headline inflation is likely due to the base effect and the rebuilding of the Chinese pork industry after the swine flu forced a culling of herds. Meanwhile, producer deflation moderated to -2.0% from -2.4%. It does not seem that the high food prices were the main deterrent to more aggressive PBOC policy, so today’s CPI is unlikely to change the outlook. Gradual and targeting easing of policy is likely to continue. |

China Consumer Price Index (CPI) YoY, August 2020(see more posts on China Consumer Price Index, ) Source: investing.com - Click to enlarge |

No country that has a current account deficit has adopted negative policy rates. The UK curve is negative out through seven years as the BOE continues to keep this card in play. However, New Zealand appears to be readying the market for such a move, and today for the first time, swap rates have gone negative. The RBNZ meets on September 22.

Suga, the Chief Cabinet Secretary of the Abe Government, has emerged as the front-runner in the contest to be the next head of the LDP, which means the next Prime Minister. Speculation has mounted that he will quickly look for validation by voters and could call for a snap election as early as late October, though November is a possibility. Suga will represent a strong continuity with Abe, including a refusal to unwind the controversial sales tax increase.

The dollar is in a tight but lower range against the Japanese yen (~JPY105.80-JPY106.05). There is an option for almost $535 mln at JPY106.25 that expires today and about $1.4 bln in expiring options between JPY105.40-JPY105.50. The greenback has been mostly in a JPY105-JPY107 range for several weeks and in narrow ranges around the middle of the range. The Australian dollar traded on both sides of Monday’s range yesterday and closed below its low. The outside down day is bearish price action, but follow-through selling has been limited. It briefly dipped below $0.7200 for the first time in two weeks before recovering to the $0.7240 area. On the upside, a move above $0.7280 would lift the technical tone. The dollar traded at a seven-day high against the Chinese yuan after the PBOC fixing at CNY6.8423, a little lower than the models suggested. The overnight repo fell 42 bp to 1.6%, the biggest drop in eight weeks as the PBOC continues to pump liquidity into the banking system.

Europe

At the heart of the Brexit challenge is the contradiction between the Withdrawal Agreement and the commitment under the Good Friday Agreement. The latter requires no hard border between Northern Ireland and the Irish Republic. By leaving the EU, the UK has to do all kinds of gymnastics to ensure the Good Friday Agreement is maintained. Prime Minister Johnson negotiated the Withdrawal Agreement and ran an election campaign centered on it being the best for the UK. Now the government is proposing to abrogate it, which led to the resignation yesterday of two senior officials.

We have long argued that a trade agreement this year was unlikely, and the new actions by the UK government add nails to the coffin. With little progress in the past several months, an agreement by the EU Summit in the middle of next month, which would allow time for an agreement to be ratified by year-end, seemed a stretch. The UK’s actions can only be understood as a recognition that there will be no agreement and that the UK will exit from the standstill arrangement with only the WTO trade rules to government its most important trade relationship.

Tomorrow’s ECB meeting remains in focus. While no new actions are likely, there are two areas of keen interest. The first relates to the euro, which, as the ECB’s Chief Economist noted last week, is an input into the central bank’s forecasts. A stronger euro would add to the deflationary forces and slow the recovery. The second relates to how the ECB will respond to the downside risks, which appear to have increased. It would be another factor encouraging an extension of the Pandemic Emergency Purchase Program and could pave the ground for another TLTRO. It seems too early to expect the ECB to change its inflation target, which is close to but below 2%.

The euro, which poked above $1.20 on September 1, tested the late August low near $1.1755. A break of this area would signal a test on the $1.1700 area, the lower end of the last month’s range, and a (38.2%) retracement of the rally since the end of June. We anticipate that once the ECB meeting is out of the way, the market’s attention will shift to the FOMC meeting (September 15-16), and in the run-up to it, we expect the euro to recover. Both the euro and sterling are lower for the sixth consecutive session. Sterling has taken out the August lows and the (38.2%) retracement objective of the rally from the end of June. The next retracement objective (50%) is near $1.2870. Today’s low, recorded in Asia, was near $1.2920. Implied volatility is elevated, and a little above 11%, three-month implied volatility is the highest since early April.

America

A light economic calendar today for the US (JOLTS and mortgage applications), the main interest is the Bank of Canada’s meeting. There is little doubt that rates are on hold. Governor Macklem is expected to underscore the downside risks despite the recent data suggesting a recovery is underway. The policy focus is on fiscal matters and the start of the new parliament session (September 23) to see new initiatives by the government.

Mexico and Brazil both report August CPI figures. Pass through from the peso’s weakness earlier in the year will likely underpin inflation. The year-over-year pace of CPI bottomed in April, near 2.15%. It is expected to rise a little above 4% for the first time since April 2019. Banxico meets on September 24, and such a rise in CPI will reinforce ideas that the central bank is on hold. Separately, the draft of next year’s budget is tight and is looking for a primary balance (excludes debt servicing costs). We suspect an austere budget coupled with the peso’s recovery will allow the central bank to cut rates again. Brazil’s inflation (IPCA) bottomed in May a little below 1.9%. It is expected to have risen for the third consecutive month in August to a little above 2.4%. However, the central bank has slashed the Selic rate, which is now below CPI, limited what the central bank can do a week from now when it meets (September 16). Brazil is the worst-performing emerging market currency this year. It is off almost 25% after the 2% rise here in Q3.

The US dollar briefly extended yesterday’s sharp gains against the Canadian dollar to almost CAD1.3260. The (38.2%) retracement of the slump since the end of June is found near CAD1.3265. The next retracement (50%) is located near CAD1.3350. Initial support is seen near CAD1.3200, and a break could spur a move toward CAD1.3150. The dollar remains pinned between its 200-day moving average against the Mexican peso (~MXN21.55) and the 20-day moving average (~MXN21.91). It has not closed above the 20-day moving average in nearly a month.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,Bank of Canada,Brexit,China,Currency Movement,ECB,Featured,newsletter